[quote]

They pick stocks which are likely winners and give them more weight than in the index. If this is successfully done they can make much better returns than the index. This would enable the fund manager to pocket the excess returns for themselves and then simply value SPY to follow the index.

[/quote]You can figure this by downloading SPY holdings and comparing it with the S&P500 Index downloaded from P123.

[quote]

BTW As of 1/10/2018, the stock weight differences between the ETF SPY and the S&P500 Index range from -49% to +97%, with only 37 of the 500 stocks being within a weight difference range of -2% and +2%.

[/quote]When you compare the SPY weights with those of the Index you will see that they do not match at all. For example, they are under-exposed to GOOGL by $4.57-Billion, and over-exposed to AAPL by $0.80-Billion relative to the Index. They obviously are taking a view on the future performance of GOOGL and APPL, expecting GOOGL to perform worse than APPL. If they are correct, then they can siphon off the excess returns and still have SPY matching the Index.

Assume that over the next month GOOGL loses 1% and all the other stocks prices remain the same. Then the fund managers can withdraw $45.7-Million without changing the relationship between SPY and the Index. (We should be in a business like this!!!)

[quote]

…the S&P500 Index downloaded from P123.

[/quote]I have not found this data on P123. Do you have a link?

[/quote]Create a new universe with the Starting Universe S&P 500 Index. Run Screen and download. All the info is there.

[/quote]I suspect that most differences are because the S&P 500 index is not strictly weighted by market capitalization. To quote S&P: [quote]

The majority of S&P Dow Jones Indices’ market capitalization-weighted indices are float-adjusted.

[/quote]So, comparing market caps of S&P 500 stocks to SPY weights, is like comparing apples and oranges. Instead, you need to compare float adjusted weights, which can be obtained by making a custom screen. See attached spreadsheet.

However, P123 does not have accurate float numbers for stocks with multiple share classes (such as Google). So many of the remaining differences are most likely caused by data errors on P123.

There is an emerging area of quant finance referred to as “stochastic portfolio theory” which begins to address the questions of optimal position weighting. One of its precepts says that the arithmetic mean return underestimates the long-term CAGR by one-half its variance. I.e., legacy estimates of small cap outperformance may be over-estimating the long-term rate of return due to the phenomenon which has become known as “volatility drag”.

Of course there is no such actual thing as volatility drag, but the risk of ruin is indeed much higher for under-diversified small cap holdings.

While SPY can “rebalance” for any number of corporate actions (buybacks, share issuance, treasury actions) which can affect the public “float” in addition to a number of adjustments due to additions and removals of constituents, it is definitely not actively managed as per George’s suggestion.

Volatility drag is just a definition: “The difference between arithmetic returns and geometric returns is the ‘volatility drag.’” Just as real as anything we can calculate in a spreadsheet.

And I agree: Geometric Return= Arithmetic Return -.5*Variance. I am not sure if this assumes a normal distribution or not, however.

It is “volatility harvesting” that seems like it cannot be real. But that too is real.

I did not say that the ETF is actively managed, but the weights of the stocks in the fund seem to be.

BTW, I made a mistake with the GOOGL weight. The under-exposure is $576 Million.

[quote]

I think they are actively managing the weights of the S&P500 stocks in the SPY portfolio

[/quote]Geov, given the fact that SPY claims to track the index, and given the fact that they are regulated by the SEC, how could they get away with different weightings?

Furthermore, why is SPY tracking error so low if they own different weights?

Furthermore, since the P123 market cap data is not always accurate (as you can see for yourself if you dig through the SEC filings for the individual stocks), why do you trust the P123 weightings?

Chipper, I don’t know what is going on with the weights. Also the weights in the float-adjusted Index differ substantially from the weights in SPY.

BTW where does one find the float numbers?

Here are the top 5 under-weighted and top 5 over-weighted stocks. Put them into a screen and you will see how they out-perform SPY. In fact one would do quite well checking the weights monthly and running a port with them. The 1-year return of these 10 stocks was 39% versus 25% for SPY.

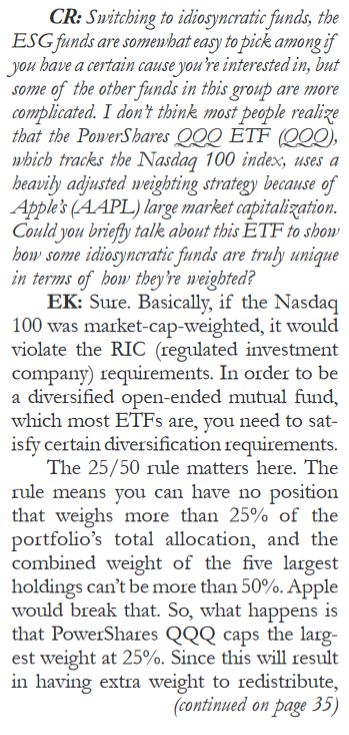

I do not know if this is directly relevant to the SPY mystery here but there was an article in Aug 2017 in AAII “The Four Groups of ETFs - An Interview With Elisabeth Kashner”

I assume I can’t post the whole article (copyright) but the screenshot is the relevant bit. Maybe a similar issue here?

Jerome, thanks for posting this. There is obviously no requirement for the fund manager of SPY to match the index’s weights. So all they have to do is to match the daily returns of the index with dividends. How they do this is their business, and my assertion could be correct that the mis-balance is actively managed to provide additional profits for the manager.

Here is a scenario how the fund manager can earn additional income by managing the weightings.

Currently SPY has Total Net Assets= $281,049.38-M and an Expense Ratio =0.0945%. So all expenses are covered by this including a fee for managing.

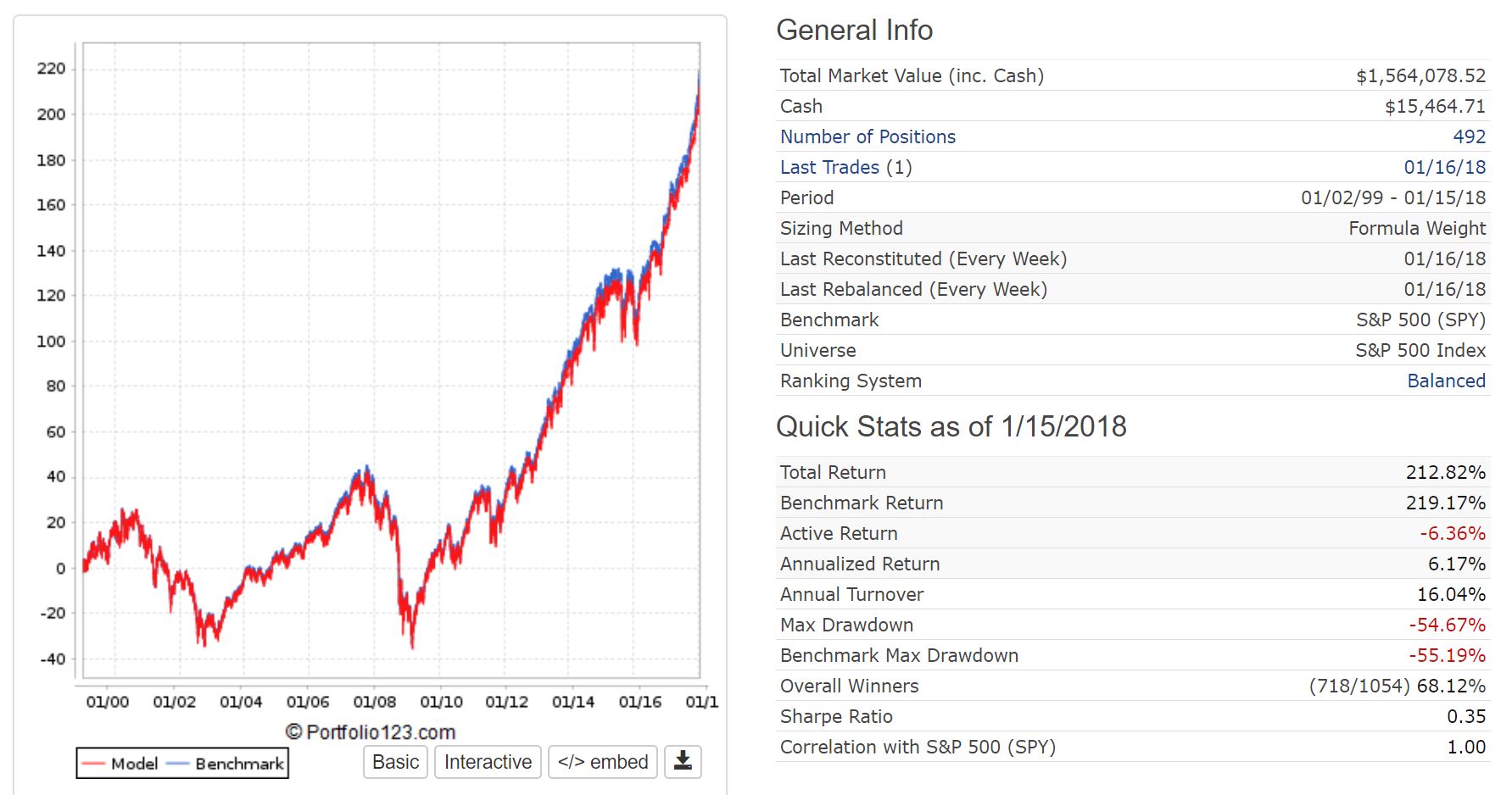

If one uses a position weight formula: pow((mktcap),0.9), reconstitute and rebalance every week, you can outperform SPY every year except in 2006, but you would have plenty of money to cover this small under-performance from the previous excess performance.

So far this year (15 days) you would have an excess return of 0.10% = $281-M.

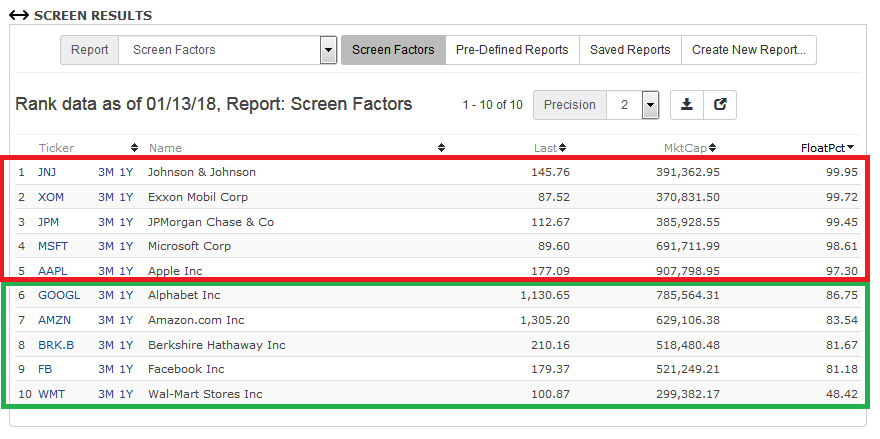

over-weighted:

XOM

JPM

JNJ

MSFT

AAPL

[/quote]Check out the attached screenshot. You should see a correlation between FloatPct and under/over weighing. That makes sense. FloatPct measures the percentage of shares outstanding that are publicly traded. Companies with a smaller FloatPct are smaller weightings in the index compared to their market cap and vice versa.

Here is a screen to calculate mktcap and float for S&P 500 stocks.

There are issues with accuracy. For example, GOOGL is showing a float of 602.70M shares according to P123 but only 297.20M according to morningstar.com. Some other stocks probably also have different float numbers for different data sources, which would explain why SPY weights don’t perfectly match P123’s version of float adjusted market cap.

Chipper,

Thank you for the screen.

Logic dictates that the under-weighted stocks should perform better than the over-weighted ones, which is indeed the case.

The 1-year return for the 5 under-weighted is 44.7%.

The 1-year return for the 5 over-weighted is 33.7%.

The 1-year return for SPY is 24.8%.

On prima facie, it would appear as though the index is purely a float-weighted passive vehicle. On deeper inspection, regulatory distortions may compel some limitations only on very large issuers (e.g., AAPL).

Despite the discrepancies, the SPY does not qualify as actively managed.