Thanks for all of the good points Denny and Don -

This is becoming more involved than I had anticipated and I probably should have explained my original thinking.

I started with the IVY portfolio. There are several references here:

http://dshort.com/articles/2009/ivy-portfolio-update.html

My thinking was that I would start with this portfolio and then see what improvements I could make. BTW - the 1Month moving average > 10Month moving average has been backtested over the various asset classes for several decades. Starting in 2006 is “out of sample”.

So I created the 5 ETF portfolio using the same ETFs as the IVY portfolio with one exception. VEU only has a history back to March 8, 2007. I substituted EFA which goes back to August 27, 2001. Whether it is the best substitution is the subject for another debate. The simulation with weekly rebalance is here:

http://www.portfolio123.com/port_summary.jsp?portid=879356

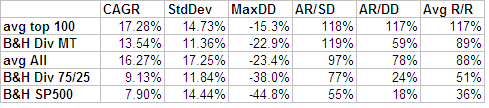

Annual Return: 4.95%

% Drawdown: 13.30%

This is with 0.25% slippage. So this sim is not pretty… Yes it has fairly sizeable drawdowns… BUT the moving average filter SMA(21) > SMA(210) did its job. Taking out the moving average filter I got this simulation:

http://www.portfolio123.com/port_summary.jsp?portid=879357

Annual Return: 3.9%

% Drawdown: 47.01%

The drawdown was significantly reduced using the MA filter (from 47% to 13.3%) with less capital deployed. This result is absolutely consistent with the decades worth of backtest results.

My thought was to try to increase profitability by using a ranking system to select the best ETFs.

Now new variables have been introduced… changes to the moving averages and adding another ETF. These are all interesting changes and I appreciate these mod’s. My only concern is not having the decades worth of backtest to support the changes to the moving average filter.

More considerations:

The start dates for the five ETFs are:

VTI June 16 2001

VNQ Oct 1, 2006

IEF July 31, 2002

EFA Aug 27, 2001

DBC Feb 6, 2007

Asuming that one year of data is used in the ranking system or buy/sell rules then by rights the sim shouldn’t start before Feb 6, 2008. So I am cheating by using a five year sim - DBC is not included for the first year. (But let’s ignore that ![]()

Now if I add 0.25% slippage into Denny’s sim and add TLT into mine I get the following results:

Dennys weekly rebalance: 57.38% Total Return

Mine with 4 week rebalance:

#1 91.28% Total Return (5 yr)

#2 79.44% Total Return (5 yr shifted one week)

#3 49.66% Total Return (5 yr shifted two weeks)

#4 55.53% Total Return (5 yr shifted three weeks)

With regards to Don’s simulation - it does provide better results but I would have to go back to square 1 and test all assumptions over again. Things like using SHY instead of IEF, etc…

Again - thanks for the suggestions!

Steve