Hi all, I just saw this thread, so I’m coming in here late. I just ran a couple of my main screens/rankers on beta and production site and results are mostly comparable, and companies selected are mostly similar with some jumbling of the order.

One thing I wanted to mention is is I have a line in my Universe

IssueChange(8) = 0

and in the original site I get about 10% more passing companies for this rule (2214 pass) than in the beta site (2003 pass)

I mentioned the encouraging news that simulation results on the Beta site using prelim CompuStat data were were finally approximating “as is” results on the existing site after the WeeksIntoQ correction was made on the Beta site.

Unfortunately, rerunning simulations on the Beta site this morning, it seems that results have fallen off the map again. In fact, I’m now seeing even more extreme differences between CompuStat with preliminary data “as is” results vs. Beta site CompuStat data with preliminary data results than before the WeeksIntoQ correction was made.

It’s hard to pinpoint what the new issue might be without more access to a log that would show, for example, exactly what changes were made on the Beta site between the WeeksIntoQ correction and this morning’s results.

I don’t know how any subscriber can make a serious evaluation of the differences between CompuStat and FactSet data until we can sort out the differences between CompuStat “as is” and CompuStat Beta data.

Is there any way to tell on our end how many months are in a “quarter”? For those who like to use quarterly numbers this is very important information.

I have the same issue and agree with this post 100%. I see so many discrepancies that I don’t know the best method (or have the time) to isolate and report them all.

Doug

Phil,

Marco has been working on estimates and will move on to actuals and ownership, then any other data set that will need to be implemented. After squaring away any outstanding differences with Compustat data and ensuring FactSet data is working as expected, I will be working on integrating RBICS further and will continue to address bugs that come up. A version supporting FactSet data may be rolled out to production if we come to a good milestone along the way, but the beta will be active as long as features are being introduced. We don’t have a set timeframe on this but hope to introduce features to the beta as they’re finished in the coming weeks.

Edward,

It looks like my recent changes should have corrected EV. Can you review the current behavior? Thanks.

Chaim,

This is an issue that we’ll have to review to pick the best solution for the platform. We’ll track updates on this Trello card.

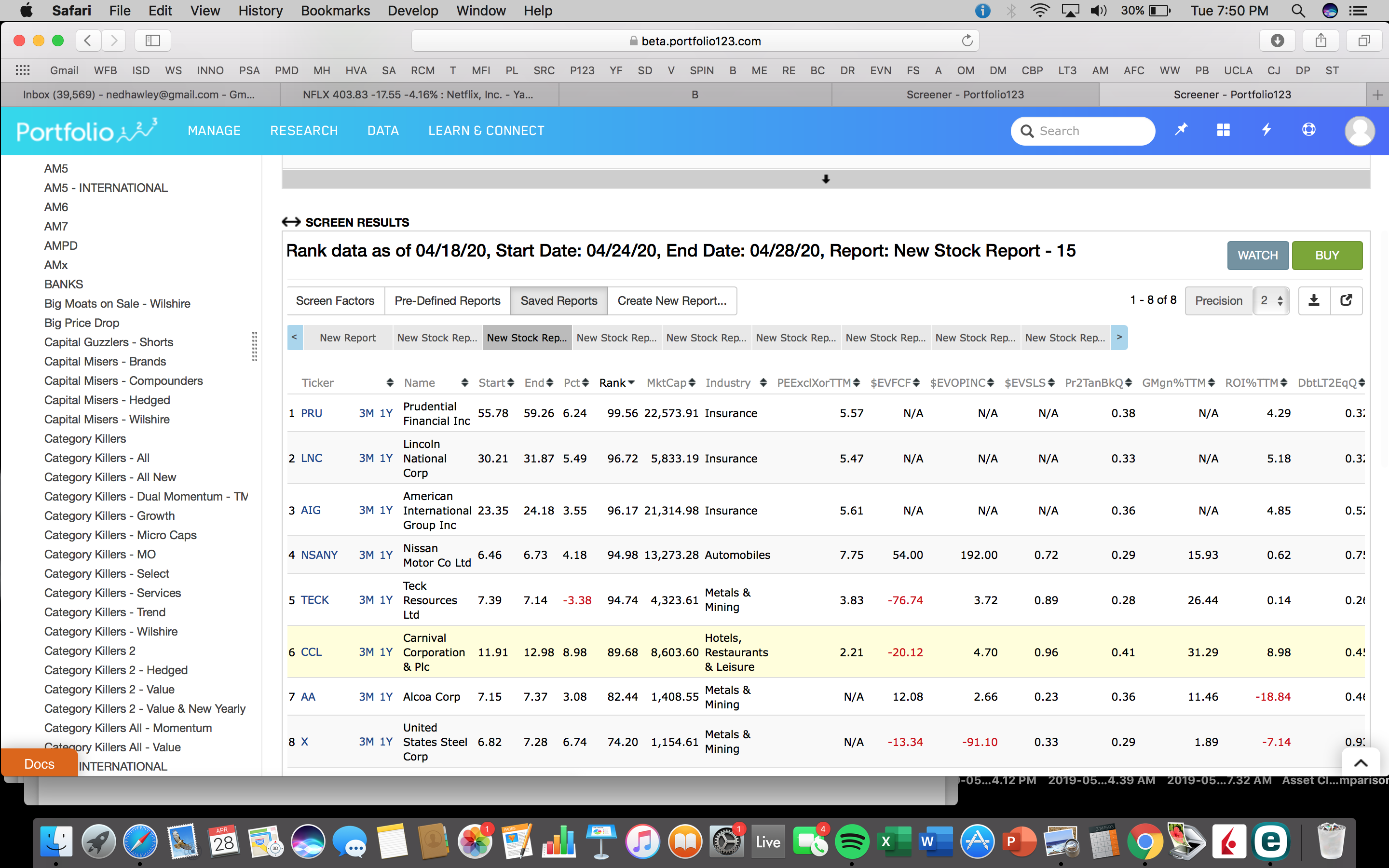

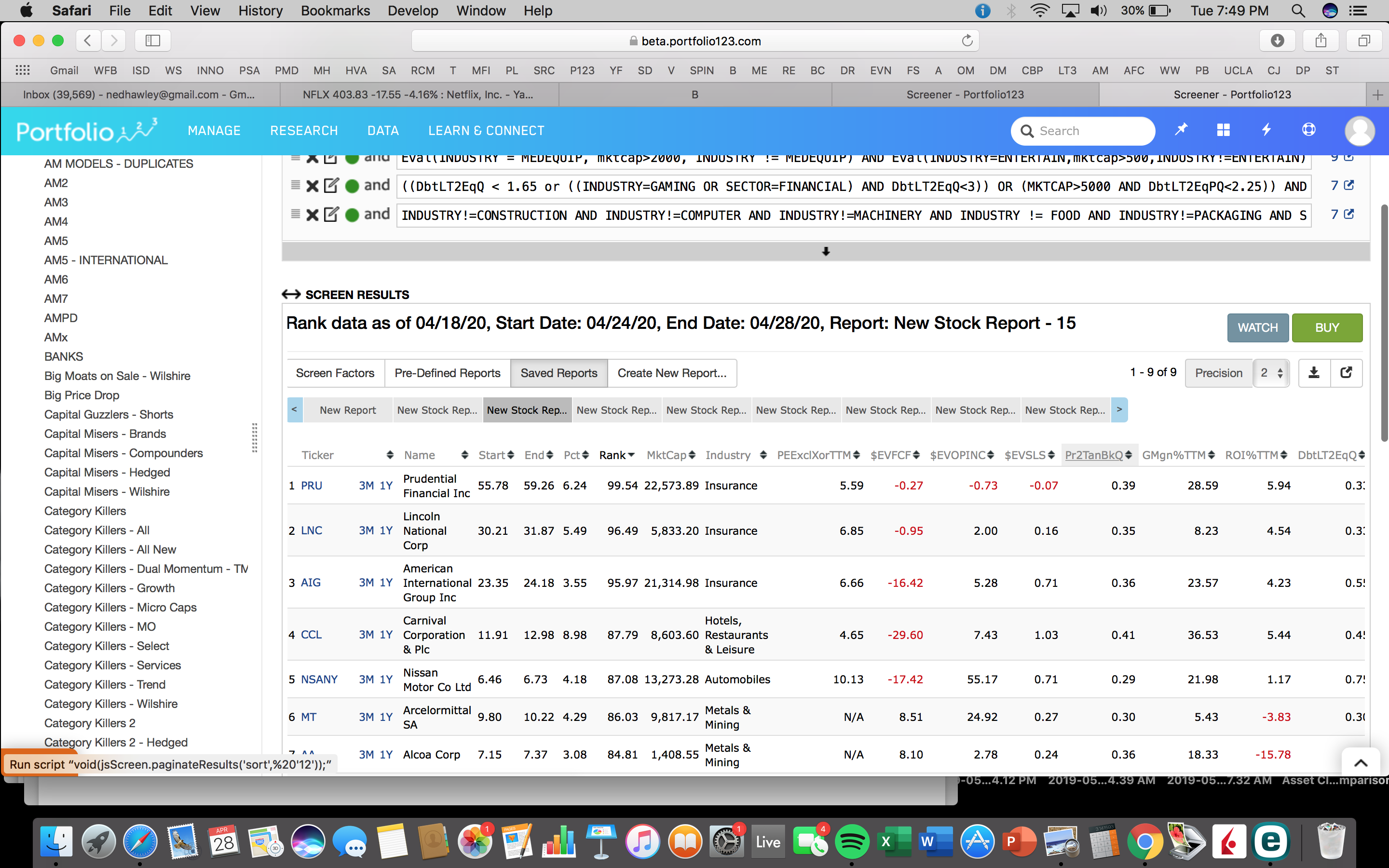

I am using it inside of Ranking System (if that helps). It works just fine if I use the Compustat database, but breaks if I set the database to Factset.

Those ratios and factors still aren’t working. I’ve included two screenshots, one with using the existing data and the other with Factset. Note the empty values - particularly for financials (definitely for insurance, maybe other industries too).

These include:

Enterprise Value/Free Cash Flow

Enterprise Value/Operating Income After Depreciation

Enterprise Value/Sales

Gross Margin

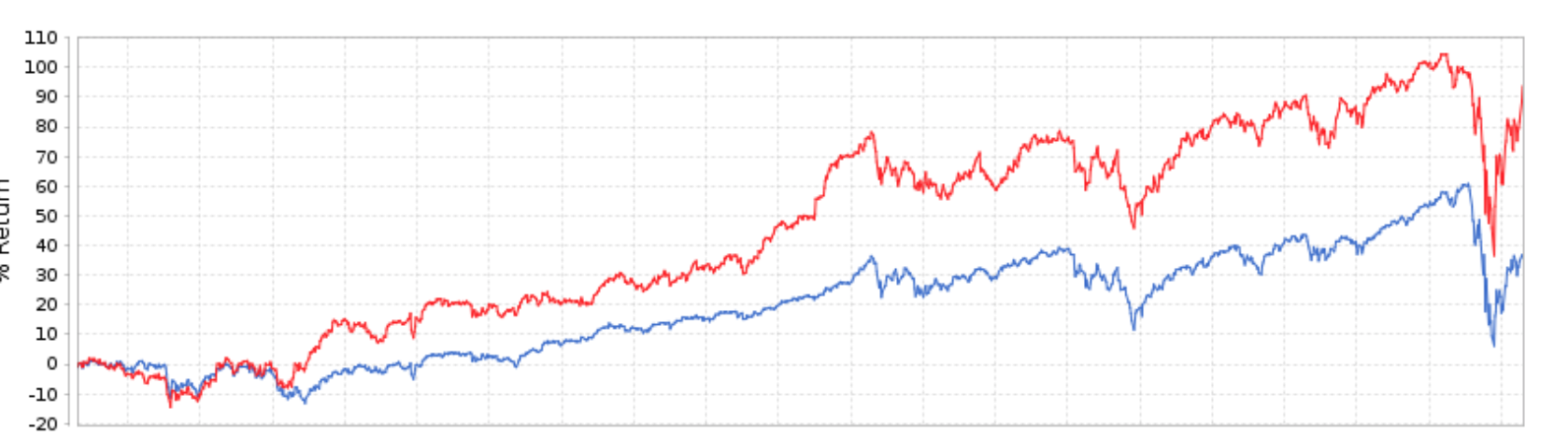

I have a conservative SP500 universe sim with a quality ranking system and buy rules based on dividends and payout ratio that has been chugging along. I finally decided today to put money into it: see first image (5 years).

Of course, best to check FactSet first. But surely some simple factors for the SP500 will not change. Not for the SP500, anyway.

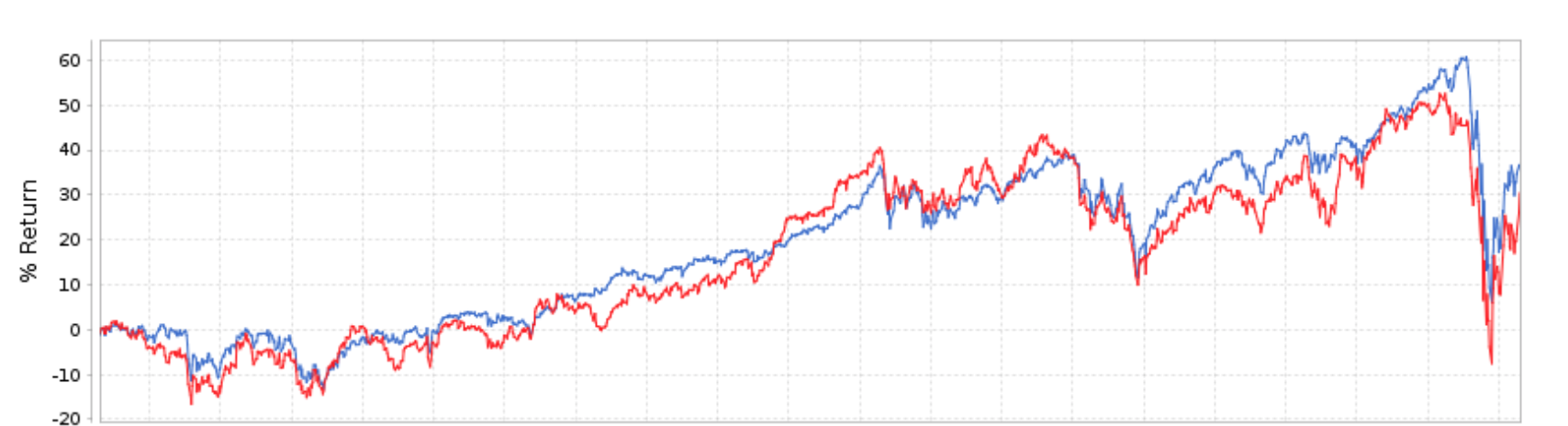

Would investing in this have been an illusion for the last 5 years? Which is right? Second image (5 years).

Still do not know what to say for now. Except possibly good to know that something is not right. And I guess I will hold off on funding this.

Are dividends included in FactSet now? Looking at the transactions looks like they are.

Indeed there are a lot of things that are “not right.” We’re still seeing some differences between Compustat numbers on beta and on the production site, which we’re trying to resolve, some of them having to do with dividends. In addition there are a number of FactSet items that we may need to remap to different FactSet items. There’s a lot in flux at the moment, and we REALLY appreciate your help. We’re especially interested in systematic differences. For example, we discovered that with the current FactSet mapping OpIncBDepr is greater than GrossProfit 20% of the time, while with Compustat that’s a real rarity. It’s possible that the mapping needs to be redone a bit, it’s possible that FactSet is calculating things entirely differently when it comes to the income statement, and it’s possible that both are happening at once.

We’re working hard on fixing every issue that we come across, and your collective help, dear users, has been invaluable.

As for whether to hold off putting money in models because of discrepancies on the beta site, the beta site is not yet fully trustworthy. The intention behind the beta site was to provide a testing ground for what we’re doing, not as a check on whether your strategy is working or not. Once all the bugs have been fixed, that’s when you can use it for that purpose.

Thanks for the update Aaron. When additional changes to the Beta site are made (ie. more variables are moved over to the FactSet database), where will the updates be announced?

I’m worried about missing something if they’re done in this thread.

Thanks for the hard work guys. Just wanted to note that recent changes (changes made since this weekend) to the Factset database have really hammered the performance on some of my simulations. Haven’t had the chance to dig in yet and figure out why, but as of this weekend my Factset performance was comparable with my Compustat performance. That has changed significantly.

One of the tickers for which I am seeing significant differences in its rank between the two servers is SCVL. I have listed a few of the factors with significant differences below