First, we found some bugs that were making the beta site using Compustat somewhat different from the production site and we’ve fixed those. They are:

-

The beta site was adjusting non-currency line items for Canadian stocks by the exchange rate. No longer.

-

Industry factors like Pr52W%ChgInd were quite different between the beta server and the production server. This was because the beta server was using the All Stocks universe rather than the All Fundamentals universe. This has been fixed. There may still be a few minor differences, but those are due to an improvement in how those numbers are calculated on the beta server.

-

Div%ChgA was outputting N/A numbers as 0 on the beta site, which meant that a stock with no dividends was ranked higher than a stock whose dividends had decreased. We fixed this behavior. Now, on the beta site, a stock which has not paid any dividends gets N/A, a stock whose dividends have not changed gets 0, a stock that has stopped paying dividends gets -100, and a stock that has changed its dividend gets the percent change.

Now on to the FactSet database.

First, thanks to Daniel for bringing up the differences.

There’s yet another TTM bug here. The four quarters aren’t always adding up for FactSet TTM. I’m hoping that will be fixed tomorrow or the next day.

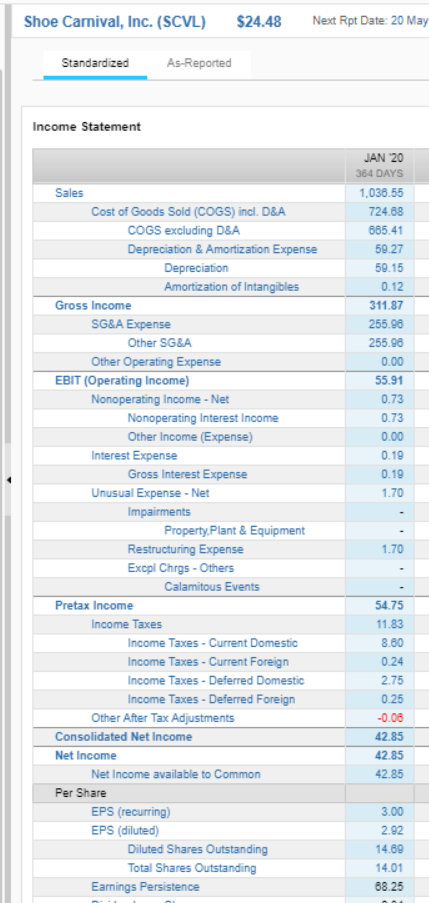

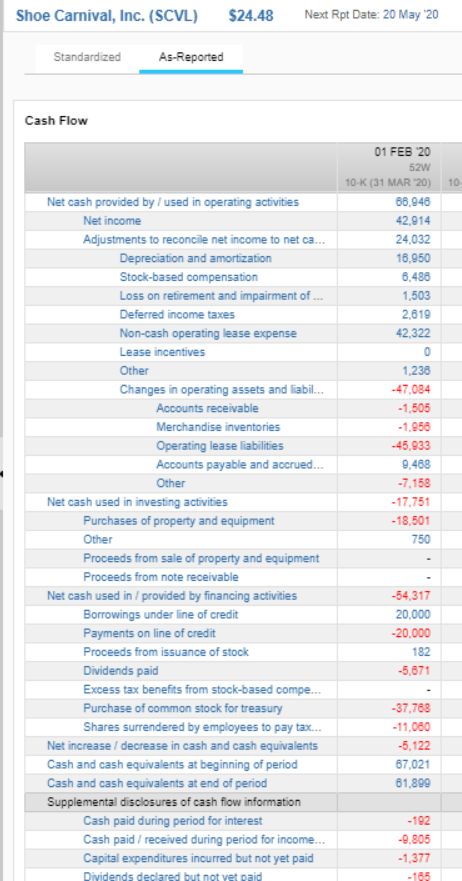

SCVL is a good example of how FactSet handles financial statements differently from Compustat.

Basically, every data provider digs into the numbers and alters them according to their research. They standardize most items depending on the nature of the business the company is in. So, for example, FactSet treats health-care providers like insurance companies, and even if a health-care provider lists its cost of goods in its filing, FactSet will not provide that in their standardized income statement because they don’t believe that cost of goods is a meaningful figure for insurance companies.

I’m attaching some screen shots to show you the difference between the as-reported statements and FactSet’s standardized statements. You’ll notice large differences between them. And these are not accidents.

We are still working on how best to handle the differences between the way FactSet and Compustat handle reported data. We will let you know when we’ve made some final decisions. Right now, as you can see, the differences are quite big for a lot of items.