Let’s bring this back to the topic of this thread; Ghost Models (why so many DMs have no subscribers).

As soon as I saw George’s initial post, I had assumed it was some sort of spoof. It was presented as a stock model (I inferred that from his use of the SPY benchmark) and as a stock model, all I could envision from an equity curve like that was Bernie Madoff. Hence I sat back quietly and watched for responses. This is a pretty good example of why DM has not been succeeding, after the initial days and when subscribers learned the hard way that carefully constructed backtests are not really investable for them.

George’s disclosure of the method (the tickers, the goal) completely changes the inquiry. Had the test initially been presented with a proper fixed income benchmark and a discussion of why he chose those fixed-income characteristics (had it been a real designer model, he could not have been expected to reveal specific tickers), I, as a prospective subscriber, would have been able to think rationally about it and whether or not it is consistent with what I expect going forward from this asset class. While the world doesn’t need and can’t expect the secret sauce, the world is going to need an understanding of what the designer is trying to accomplish. George’s first presentation delivered the message “hold on to your wallet, run far and run fast.” The information he added (even without the exact ticker) changed the game and provoked the sort of rational thought process a DM subscriber should be expected to pursue.

I think we’re now seeing why there are so many “ghost models.”

Mark and Yuval,

Thank you for your comments. The reason I chose SPY as the benchmark was to ask the question: which of those two performance curves do you prefer to but your money in? The obvious answer is the red one. Obviously one should use a fixed income ETF as the benchmark with similar duration as the model’s, like IEI.

But Yuval is correct, a straight line indicates diminishing returns over time. That is what has happened to savers in fixed income funds, they have all seen poor performance for the last 10 years. You need to have increasing returns per unit time. A log-plot of the performance curve should be a straight line with a positive slope.

Hi Jim, If you’re willing to share, I’d love to understand how quickly you adjust your buy and sell bids and offers? How quickly are you able to move into and out of positions? I think that I’m probably slower than I should be in just “paying up” for a buy or “accepting” a lower price on a sell. I have had a few run away from me recently.

I place a VWAP or Percent of Volume order for the total number of stocks recommended by the port in the morning. Market orders for small orders.

Any strategy I MIGHT develop would be the opposite of what Nisser outlines. If a stock is moving (eg a stock is increasing in price after a favorable announcement) I would speed up my purchases. I would want to finish my order before the stock moves higher. Maybe convert from 5%POV to 10%POV.

The opposite situation is when a stock is going lower. Do I want to put on a limit order and buy all of it when it hits the limit? Maybe. But maybe I want to slow the purchases and let it continue to go lower—getting an even lower price.

This is the strategy outlined in the books IF YOU BELIEVE THE PRICE TRENDS. I am inclined to think stock price moment is generally random over shorter periods BUT who can deny that stocks will move in one direction after an announcement: for the whole day or even a week or two. A few stocks never come back at all. Admittedly, a few. Those few “tail-events” seem to have a large impact on my returns.

If the movement is truly random it does not matter what I do anyway. I think trading reversion to the mean will work for some ports but there is a lot of work needed for that timing. And probably requires more smarts/patience than I have.

Even if I rebalanced every quarter, I would look at a new set of stocks a week later—in another port or something. I would not be chasing week-old information. But I don’t watch yesterday’s news on TV either—could be just me.

That is what I would consider as a strategy. In truth, I put the order in in the morning and watch. Never changing it—not really a strategy.

But at the end of the day when the accounting is done, I do beat the sim (or port on auto) and the more trades I make the more I beat it.

Then I guess we’re trading on entirely different planets, because that doesn’t work 100%.

I keep track of all my attempted sell/buy orders. In 2018 I made 65 attempts with about 10% of them running away from me (Following about 3-4 systems with low turnover). Some tank and are losers, others are winners but I have no reliable way of predicting which is a loser and which is a winner. Some initial tankers make a U-turn and become winners and vice versa.

I do not have time to watch and adjust orders throughout the day. In fact, I can’t even wait to see what happens at the open as I’m a west-Coaster and I need to…go to work!

I set my orders on Sunday based on previous close.

Close to minus 0.5% for sell orders

Close to Plus 0.5% for buy orders

I make them for the entire week and I do not adjust. About 70% of them go through on Day 1. Others are filled throughout the week, or not at all

I cringe at the thought of my transactions quadrupling or more. There’s no reason to believe that the ratio of run-away orders would decrease.

If owners of DMs are intending followers to monitor open prices, adjust, watch, calculate VWAPs, etc…then it’s absolutely no mystery to me that there’s so little interest in current DMs. You have to understand your target audience.

Lot’s of great points mentioned but the most important reason is the probability of selecting a DM that will perform well Out of sample. This is a very difficult choice and knowing what is under the hood is important but there is one more thing that greatly influences the decision. The reputation of the designer. My numbers are not exact but since the first 2 years of DM launched there are only 30 models that have positive excess return over the last 2 years out of 120 total. I’m sure the numbers are not much different since inception. If you were to include the grave yard the numbers would be magnified 2 or 3 times. Let’s say a designer has launched 10 models since 2013 and has retired 8 with bad performance and 2 are left from 2014. In 2014 there is no way for me to decide which of the 10 DM to invest in since I have no way of knowing which ones work. Fast forward during that time period the designer launches another 5 models that have great back tests but very little OS performance. Would you invest in any of the new five models if you knew the same designer has retired 8 that don’t work? The point is as a Designer you hurt your credibility by retiring models that don’t work. I’m not sure how to fix this since no model is perfect but since the vast majority of models fail it is really hard to pick a DM with a high probability of future success. I think the Designers who are successful will have 50% of there models beating the market over the long term and this will be combined in a book explaining the strategy of how these DM will beat the market over the long term. If the strategy does not work deleting it is not the solution since your credibility is gone just like the deleted model.

“In 2014 there is no way for me to decide which of the 10 DM to invest in since I have no way of knowing which ones work. it is hard to pick a model with high probability of future success”

Well, it is not only 2014, it is ALWAYS. What you are looking for is a nice wish but an illusion.

NO model and no parameter will give you a guarantee, not even a “high probability” that a model (or any model) will result in future financial success.

Otherwise the whole game would be easy.

That’s not at all obvious, and is an example of the flaw of using historical testing for unsuitable purposes.

The seemingly better long-term record owes nothing to the merits of the strategy and everything to the fortuitous date as of which test data on our platform first became available, which just so happened to have approximately coincided with the peak of an epoch bubble. Suppose, on the other hand, the oldest possible start date on p123 was 6/1/02, or 09 9/30/08. In that case, it would be equally “obvious” the the blue line would represent the preferable outcome. Or, if the earliest start date was 1/2/08, we’d be back to the red line as the “obvious” choice. Actually, though, none of these answers, nor any other, is ever obvious becasue we could game the start and end dates in countless ways.

Once again, I’m going to try to bring this thread back to the original topic, ghost models (the failure of many DM models to attract users). There is no way around the reality that DMs cannot hope to succeed on the basis of backtest data. Given that the future is unknown, however, there still needs to be a way to match potential providers with potential subscribers. The only thing that is going to make this happen is for potential subscribers to be clear to themselves what they are looking for interms of risk-reward and for providers to present their offerings in an understandable and authloritative way (non-statisticl reasons why your strategy can be expected to satisfy certain risk-reward goals in the future), and by now, it should be well understood that backtest results are not the answer (and if you doubt this, then check with the many early subscribers who walked away).

thanks for your valuable feedback. I agree that most (~99%) of algorithms cannot reproduce the simulated performance. Hence when I look at DMs I can only make choices based on out-of-sample performance.

Here are my selection criteria for investing in a DM:

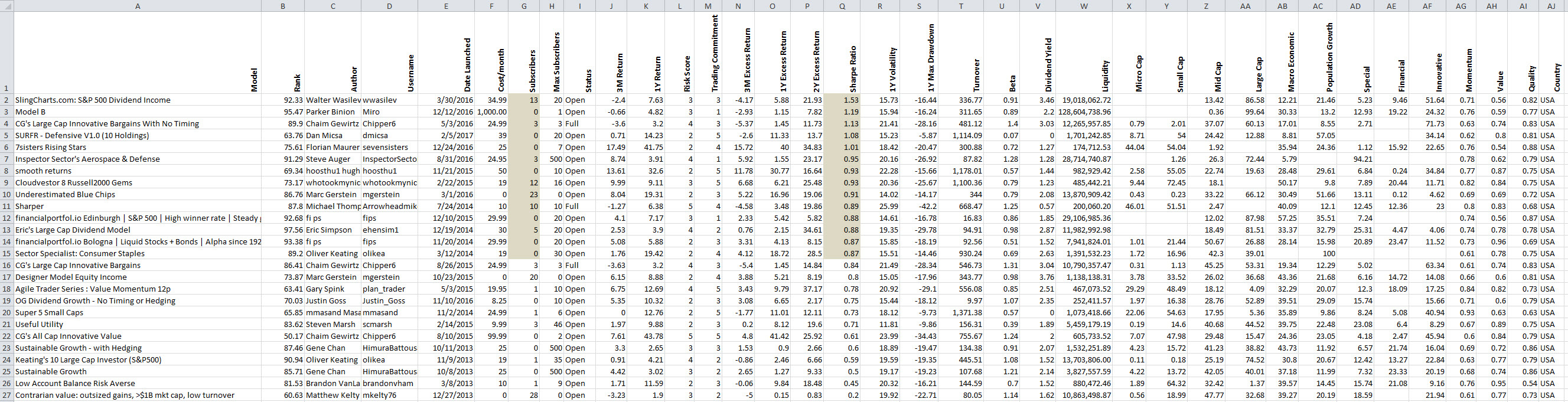

from all DMs (currently 287) I choose those who have both 1Y and 2Y positive excess returns: there are only 40 models which qualify as of today. All others don’t live up to their simulated performance (or hopefully will in the future if they are launched less than 24 month ago).

from these 40 models I eliminate those with > 1500 annual turnover because such high turnover is likely to have a large proportion of the profit consumed by trading fees: this leaves us with 32 models.

from these 32 models I eliminate those which are ‘coming soon’, hence cannot have any subscribers: this leaves me with 26 models to put my money in.

aiming at lower risk, I can sort these DMs by Sharpe ratio (see attached), and sure enough the DM with highest Sharpe ratio has a decent number of subscribers. At the same time there are 7 other DMs with acceptable Sharpe ratio > 0.85 which don’t have any subscribers.

Hence most subscribers probably use different criteria such as cost, reputation or perhaps P123 Top designer model rankings, all of which are not prominent in my final selection.

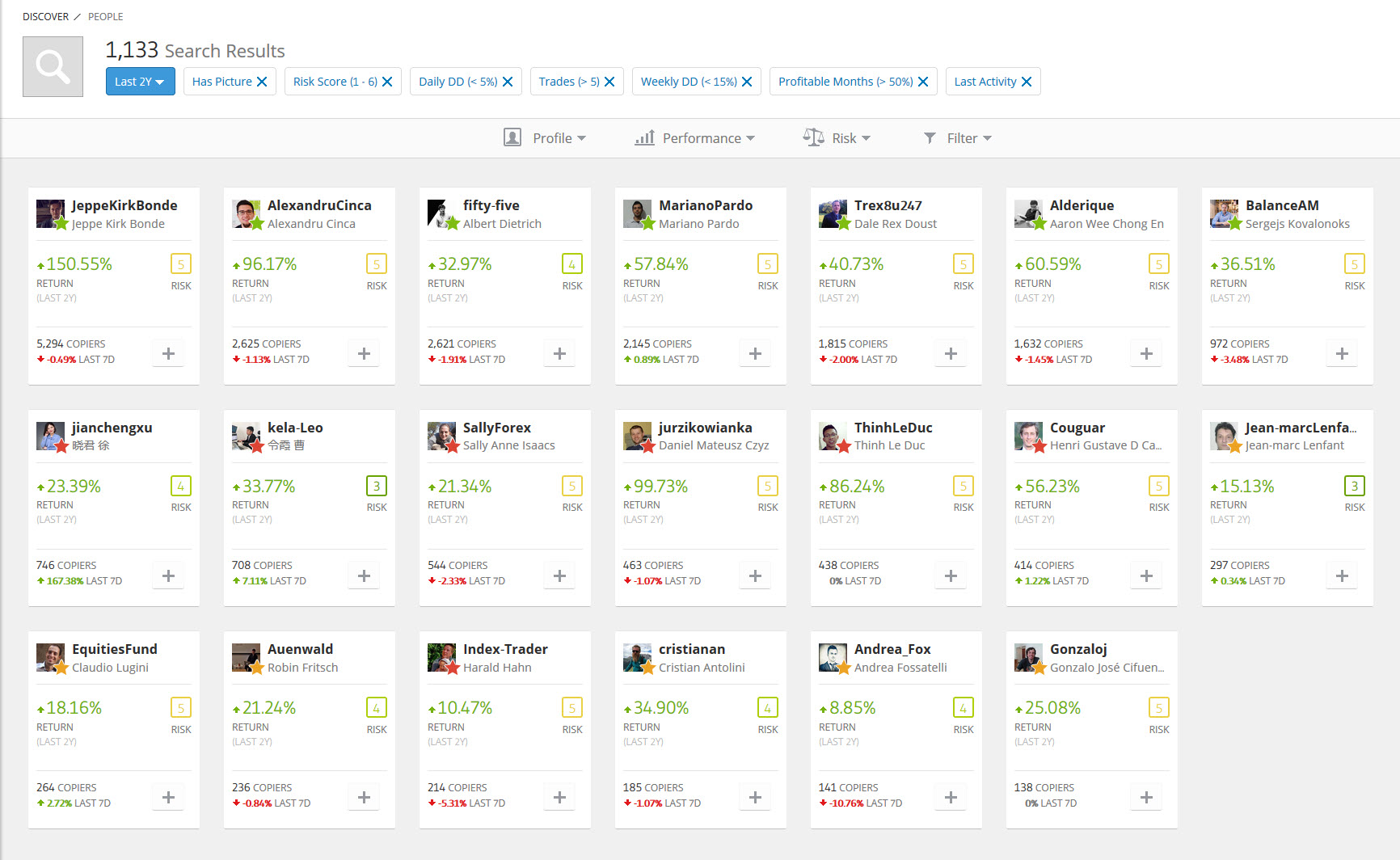

What bothers me most is that we have such a good platform here at P123 yet the community is very small. For comparison I post a screen shot from e-Toro with models having excess returns over 2 years. Look how many followers there are per model compared to P123!

Well, eToro looks very interesting. Does anyone have actual experience with the site? I do like the UI and that it’s geared toward the consumers of recommendations - i.e. portfolio owners. Of course, P123 co-mingles consumers and producers. It that setup a barrier to potential subscribers? How do eToro producers generate their portfolios?

Looks like this means you are informed about what the person you are “copying” has already done—at least in many cases. And in at least some cases copying a “Professional.” Discretionary trader?

Front running may not be the word, but it is different. Apples to uhhh…. pork butts, I’d say.