As many hedge fund managers do, such an activist approach can accelerate the realisation of potential profits from their short positions, help others sell or short junk stonks, and help raise capital for their hedge funds.

After reading many shorting reports, I think quantitative models can identify junk stonks much better than they do. However, many junk stonks need some narrative as a catalyst to trigger a price crash. Considering Yuval is a writer, I think he can write better articles than the vast majority of obscure and hard to read shorting reports.

I don't think he would short any large cap stocks.

Also, I have read that article many times. The last time is to find if NVDA is a scam:

However, a shorting opinion on large and mid-cap stocks cannot have a similar effect if it is not matched by Hindenburg's influence, so I am talking about Yuval's shorting opinion on small and micro-cap stocks.

Thanks for the suggestion, ZGWZ. I'll definitely think it over because it really makes sense. But most of what I wrote about APLD in the forum has been written before: it's not original research. Furthermore, as I found out after the Tingo Group debacle a few years ago, Seeking Alpha does not allow me to accuse any company of fraud or cooking their books, no matter how obvious. In addition, my largest put positions are in RIVN, MARA, and UEC, none of which are small caps (yet; UEC will shortly be one . . .) I've always written about my process rather than my opinions about individual companies . . .

I'm pretty sure going public with short reports has opened short sellers to a lot of legal trouble, whether the reports are justified or not. If it's your business model, maybe it's worth it, but otherwise, maybe wise to tread carefully.

It's a shame, because you'd want fraudulent or otherwise shady business practices to be exposed, but given many of these sorts of companies are already bad actors, and short reports threaten their business further, it's safe to assume they'd not hesitate to try to take down threats.

I'm not trying to expose corporate misconduct, I'm just trying to learn and make money from shorting reports.

Edit:

BTW, one of the reasons I exposed NVIDIA is because too many people were bragging to me about NVIDIA being an super undervalued deep value stock and despising the p123 system's picks as so-called "overvalued momentum plays", and that really pissed me off.

I think almost all companies are (very) bad actors, it's just that some are particularly extreme in their approach, e.g. NVDA is much more extreme in US-listed megacap stocks than even LLY and TSLA, or Aramco is much more extreme in publicly listed integrated oil giants than Imperial Oil and Suncor Energy. The latter is one of the reasons why they can't list it in the US.

Edit:

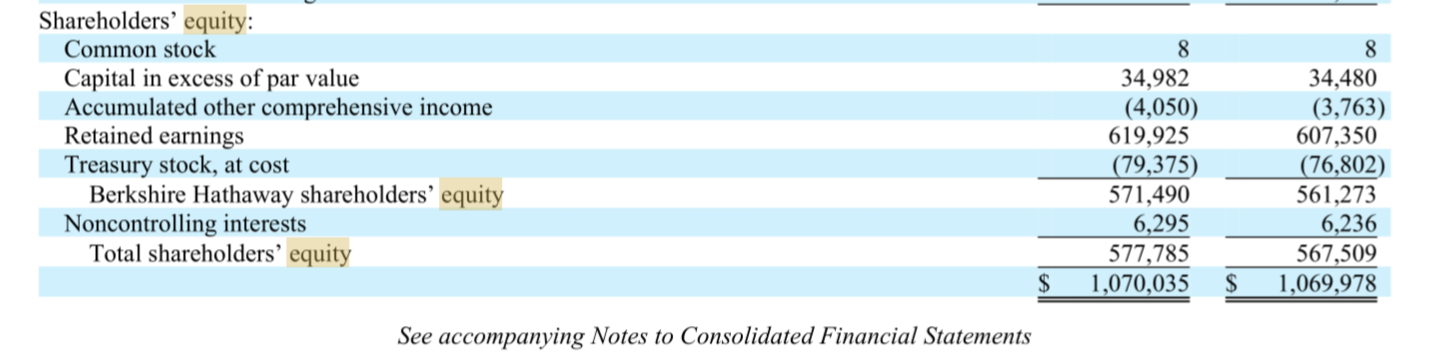

Even the almost financially most reliable mega-cap stock, BRK.A, has many potentially dubious elements. One only has to compare BRK.A with Mitsubishi Corporation, the largest of the Japanese trading company stocks that Buffett himself says has a similar business model, to see that the former has an extremely low D&A ratio of 3%+ compared to net PPE and intangible assets, whereas the latter's D&A ratio to net PPE and intangible assets is a whopping 15%+, which implies that BRK.A's assets/net incomes are somewhat inflated.

Edit2:

Buffett's company is also expensive even in the US. Its relative valuations are higher than 78% of its peers, and about 60% more expensive relative to the median valuation level, according to the discounted cash flow model and the industry relative valuation model. That's not even taking into account the fact that its structure is like IEP more than a typical peer company.

After his inevitable near-term death, BRK would need to fall by about 40% to reach its current level of relatively reasonable valuation due to the risk of his heirs selling off their BRK stakes in tax shelters called charities in order to buy broad indices as his recommendations) or other investable assets (such as Treasury bills, or may also include many foolish investments), to bear the cost of charitable activities (some of them are mandatory according to tax codes), to pay taxes for new tax codes which may come true in the future, to pay for their lavish lifestyle, and the risk of its long and deliberate image being dented. If the US market returns to its long-term average valuation or the global average, then BRK would need to fall by 60 per cent or more.

Maybe we can read a new Hindenburg report in the future like "Berkshire Hathaway: The Oracle of Omaha Preaching Value On His Own Bloated Throne" or "Berkshire Hathaway: How The World’s 6th Richest Man Is Pulling The Second Largest Con In Corporate History" (with an response to company "Our Reply To Buffett: Fraud Cannot Be Obfuscated By American Nationalism Or A Bloated Response That Ignores Every Key Allegation We Raised")

So is this an issue of different accounting standards of different countries? But even compared to scandal-ridden US-listed Brookfield Corporation/Infrastructure, BRK's depreciation rate is a bit too low. The former's parent and subsidiaries also have a 4%+ depreciation rate, while BRK only has a 3%+. And if we talk about conglomerates with many business units like MSFT and GE, their depreciation rates are even much higher at 10%+, even though I have questioned MSFT's cash holdings/flows before and many have questioned GE before.

Also, from the first link:

But Brookfield is hardly the only company with what is known as a dual-class share structure. The roster of companies with such a structure includes Google, Berkshire Hathaway and The New York Times Co. Whatever their merits, dual-class share structures are designed to keep the company’s operating assets in the hands of founders. When Berkshire Hathaway’s Warren Buffett likes another company, he does not use his publicly traded corporation as a springboard to build a string of downstream corporate investments via minority stakes; he generally buys all of it.

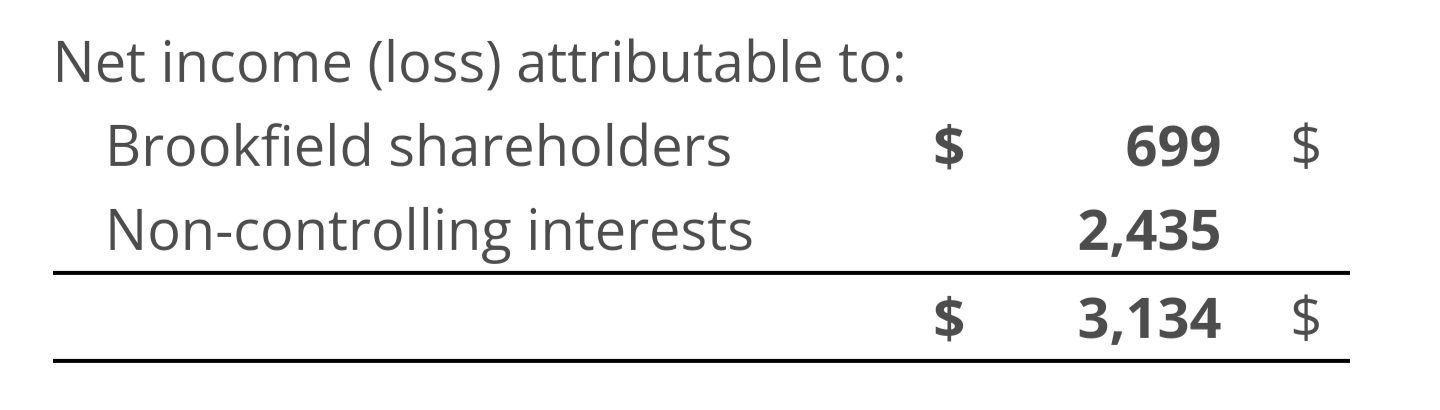

As a result, Brookfield is more likely to blame their low depreciation rate on non-controlling interests, while BRK not so much.

I do think Buffett has outstanding positive alpha generating ability and has correctly exposed the grossly fraudulent nature of the private equity industry (of which Brookfield is one of the participants). But buying his holding company at a premium of at least 60% when he was clearly dying and buys are at risk of becoming exit liquidity is another matter.

Buffett notes buybacks make sense only when a stock trades below its value. "All stock repurchases should be price-dependent," he wrote in his 2023 letter to shareholders. "What is sensible at a discount to business-value becomes stupid if done at a premium

After all, Buffett has literally told you he thought his stock is overpriced now by his speakings and his buyback plans.

BRK believers/HODLers are indeed less stupid than many of the GME apes now going for IEPs and calling GME a value stock, which is at least at a 100%+ premium and under threat of the extreme and severe dilution that is clearly happening at the moment. However, GME apes are even less stupid than NVDA/SMCI apes who think they are "value investors" instead of scam enjoyers now. After all, it is still not a good idea to assume the companies from which you buy their common stocks are not bad actors from the beginning. Trust models, not people (or companies).

I ended up writing an article about APLD and NVDA, as you suggested. Seeking Alpha wouldn't publish it because they shy away from suggesting that companies are engaging in fraud or financial manipulation, so I published it on my blog: https://backland.typepad.com/investigations/

Clearly, finding interesting shorting / put option opportunities are accessible to P123 users even without using (additional) external sources of information.