I can't find 17% and 13% in the chart

The "fake foreign cash" problem may also exist:

"Lower tax rates abroad" may mean non-existent cash income, non-existent tax payments and non-existent cash balances. Instead, share buybacks may be mostly backed by debt financing from affiliated entities including CoreWeave.

The worse part is not CoreWeave itself. It is about the AI Infrastructure Server Solutions For Enterprise.

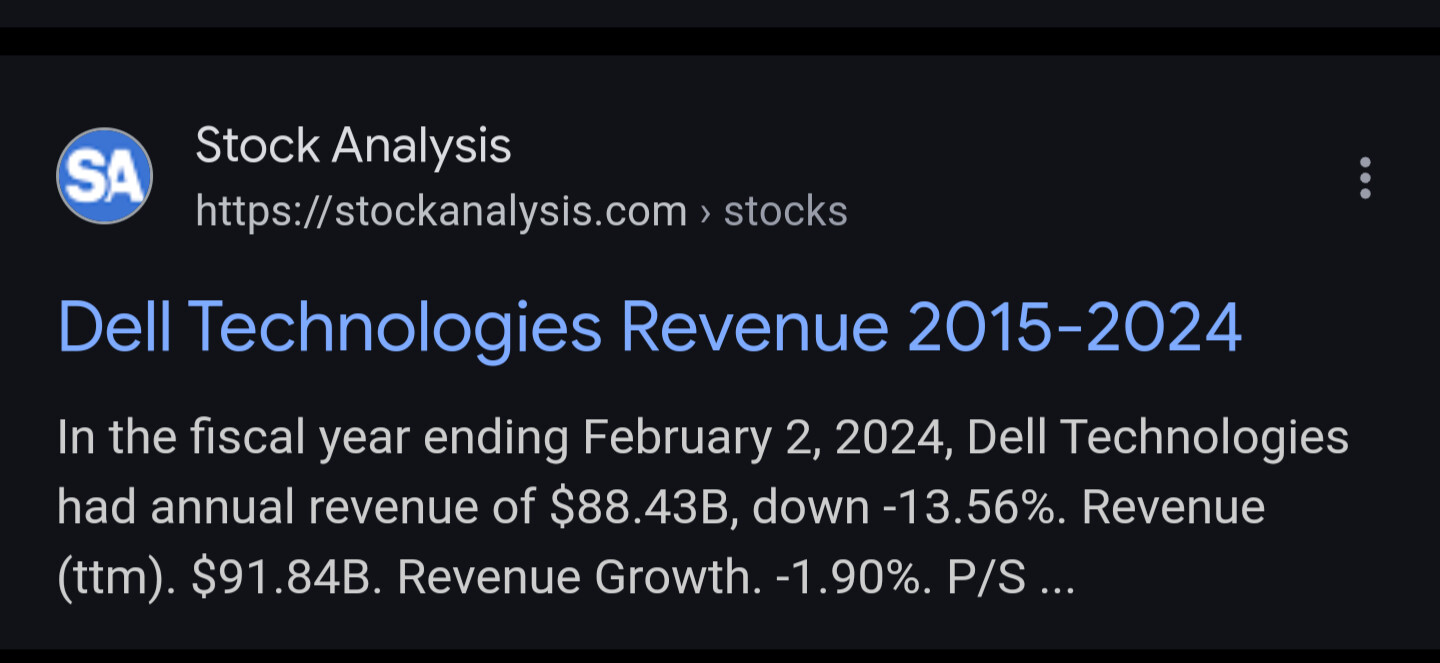

In fact, despite Jensen's praise, Dell, a strong competitor to SMCI n the server solution industry, had negative TTM sales growth, as has HPE, which offers similar solutions.

"It seems that AI has become so powerful that they can even assemble themselves to form their own servers without the incompetent Dell, HP and SMCI, and we are one big step closer to ASI and everyone enjoying UBI without having to work!" /s

Super Micro crashes after company says it will not file 10-K on time

Coupled with the fact that SMCI is suspected by short sellers of fakery and has an M-score even higher than 0, a plausible explanation is that since the "AI data centre investment mania" doesn't actually exist, so does the sales mania for AI server solutions if we don't include SMCI's cooked books.

Background: $80 Billion Global Data Center REIT With 260 Facilities Globally

Despite growth CapEx at all-time highs, billed cabinet growth slowed to 1.7% in 2023.

Equinix is another red flag because its real sales growth was only 1%+ in 2023. Even if the biggest users tend to build AI data centres on their own. The smaller players still need data centre providers like Equinix for their AI servers. The tiny real sales growth of Equinix means the general AI mania narrative may be a scam at all.

The worse part is Equinix's competitors have even worse sales. For example, Lumen is exposed by many short-sellers and has a two-digit negative sales growth.

Digital Realty is just not so bad but still has a negative growth.

Maybe people are just moving to clouds?

However, even CoreWeave still needs those traditional data center providers like Equinix to storage their servers.

So if the so-called "AI investment mania" does exist, why would data center industry enjoy such a minus sales growth as a whole?

Of course, I'm sure AI and our tech god aka Wonder Uncle Jensen's accelerator cards have evolved to the point where they don't need any real places to store at all, right? Right? /s

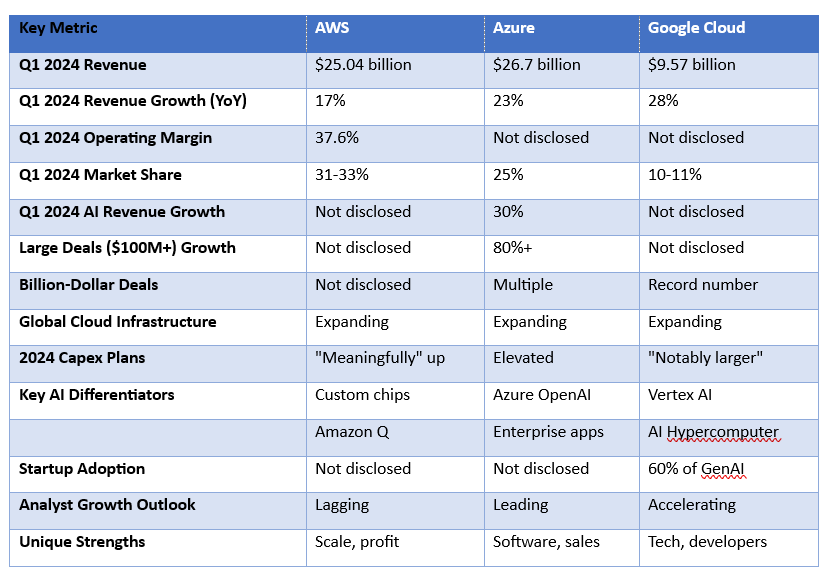

Regarding cloud services, the three cloud service giants didn't do so well in terms of revenue growth either.

Azure, the only one to have posted AI-related cloud service revenue growth, didn't grow much higher than its overall growth in AI-related cloud services (23% vs 30%). This doesn't support the narrative that the big three cloud service providers are rapidly investing in AI infrastructure to serve surging demand.

The problem isn't whether there is a real gold mine, as many say, or even the absurdity of thinking that "NVIDIA is a good company, but the stock price is a bit high and will need to be pulled back later", but rather the fact that there isn't even a real gold rush going on, or maybe the real gold rush is the stonks we pump and dump along the way /s

While all the companies up and down the chain of the alleged AI investment mania are enjoying negative, single-digit or at best slightly over 10% TTM sales growth, only NVDA and its friend SMCI, also from Taiwan, are enjoying staggering triple-digit growth rates, and the latter has had its financial reporting delayed and its share price plummeted by short-sellers on suspicion of fakery. But NVDA's nearly 200% TTM sales growth must be real. /s

If Nvidia reverts to its 2022 earnings of 0.17 per share, coupled with a valuation of about 10x-20x due to a lack of real growth prospects and involved in scam like PDD & BABA, it could fall to much less than $5, assuming it doesn't fall into the red under the pressure of bagholders' lawsuits.