This website has some interesting information on this topic; also below is a strategy that could be implemented in P123 provided it can retrieve VIX and VXV info:

A heads up about risk control: While the VIX only goes back to the early 2000’s there is another index (Yahoo ticker: ^VXO) that measures the S&P 100 Volatility and goes back to the early 1980’s. On Black Monday ^VXO spiked up from ~36 to a high of ~152 overnight. Such a spike would probably easily result in a total loss for ETN holders. See Fred Piard’s good article on SA.

Etn ticker, vqt, allows the less skilled to have a long position in a VIX like instrument when it is trending upward. It’s maximum backtested drawdown was 18% in 2008. It has credit risk via Barclays Bank but is tax efficient due to its structure. However this etn has a small return relative to the potential return that one could achieve if they have the tools and guts (trading the VIX is like chasing a jackrabbit on crack) to successfully trade the VIX.

Did any of you consider just buying the mutual fund mentioned earlier in this thread (I am always suspicious when a hedge like fund converts to a mutual fund format after several years of good performance followed by a suboptimal year as retail investors just buy funds based on past performance and institutional/ qualified investors usually do more due diligence into the funds methods/system)?

In my own modelling, I have come to the conclusion that systems that go long/short VXX (or long XIV) can complement other systems. I would suggest that the most successful models use both contango / backwardization along with some type of trend following of the VIX to determine the switch (or going to cash at certain points). Most of the profit comes from the short side because of people’s propensity to overbuy insurance, but those times when you switch long volatility and everything is falling apart, it can really help smooth the equity curve. (Although there are lots of false starts and whipsaws on the long side which make it mentally tough to trade).

If the risk of ruin in a product like XIV is too much to handle (and if it is, I would suggest you have too much devoted to the strategy), you can use option spreads on VXX in order to help dial in your risk. (VXX has puts and calls traded on it with relatively good liquidity)

I find this interesting. I wouldn’t want any trade secrets but the VIX is a very interesting patten. It spikes up quickly and then follows an exponential decay. The decay seems to be the only predicable portion of the curve to me (very predictable). Although there is some discussion of auto-correlation of volatility in the literature (Mandelbrot).

I am not very worried about what institutional investors are doing. They chase recent performance like everyone else.

I have a proprietary method to evaluate talent that has worked for me. It does not overweigh recent performance. In fact, I often find that if the manager is talented then recent performance is mean reverting. For example after Fairholme’s famous dip in 2011 they have been in the top 15% in their category for three years in a row. So too after Weitz Partners Value had a difficult time during the financial crisis they were in the top 15% of their category for four years in a row.

Joel Greenblatt ran one of the most successful hedge funds in history (50%/year for his first ten years). In one of his books he described how it was when he was first starting out. After a few months he got a call from one of his institutional investors: “You were up only 1% last month while the market was up 1.5%. To what do you attribute this underperformance?”. That’s not an exact quote but it sums up the unhealthy fixation on recent performance. If you can have confidence in a strategy to stick with it through thick and thin and have no one looking over your shoulder then you have a huge advantage over almost everyone else.

From reading that description on the website it is tempting to invest with the Catalyst Fund but without knowing more about their strategy it is difficult to really know if they are good or if they were simply lucky.

Chaim I wish I were that smart. What I will do is more simple and basically just takes advantage of the roll yield. I will probably wait until there is a huge spike in the VIX and wait until the futures go from backwardation to contango to buy the XIV. I’ll get out when the VIX goes to backwardation again or just when the VIX spikes. A 50% increase per year for XIV is good but I have a port that is doing that well and it has a little less risk for now.

This morning I woke up thinking I would put $5,000 into XIV with $5,000 in reserve, hoping to get out of XIV then back in with the additional $5,000 if the VIX spiked but I probably won’t do it. If I don’t, however, I will regret it in 10 years when my 5,000 could have been $288,000 at 50% per year compounded.

@Jim, I agree with you in general…that is the most predictable portion of the curve – that is, just going short volatility, does really well right after the expansion – that’s where the outsized gains are. That said…in terms of gains, there is not much there in going long volatility…but the value comes in when you are long when everything else is going to hell (look at 2nd half of 2008,2011). It’s not that you are making money on that part of the model, it’s just that it’s SUCH a good hedge against your other models that you can’t ignore it. That may be every bit as important as the outsized gains in the other part of these models.

I agree with your general points. ‘Good’ managers are mean reverting often. Evaluation of manager skill is very hard. And…often best entry time is in a multi-year dip (like managed futures now, to me).

However…out of curiosity, I looked at the Weitz Partners Value fund. Have to say…I see no evidence of manager skill. All of their ‘outperformance’ can be explained by two simple factors - a) equal weighting and/or b) weighting on simple value factors.

Buying the 900 or so, P3000 stocks with MktCap>$100MM and Avg DailyTot(60)>$5MM and close>$2 and rebalancing annually…Equal weighted, would have returned around 16% / yr since 1999. That significantly outpaces Weitz over 14 years or so. Randomly sampling stocks with some sector controls from this universe would have beaten them by 4% or more per year on average.

Buying the top 50 ranked value stocks in a screen from same universe, using the prebuilt single PE value factor would have also outperformed Weitz…albeit with more volatility and a bigger DD in 2008 period. Would be way ahead since 2009.

Making an annual rebal. sim with P123’s prebuilt value rank and buying 50 stocks from this uni, with annual rebal and no sector greater than 20%, would have also beaten the Weitz fund handily.

My opinion is that…many managers are charging for ‘performance’ based on simple EW and value factor loadings. And luck.

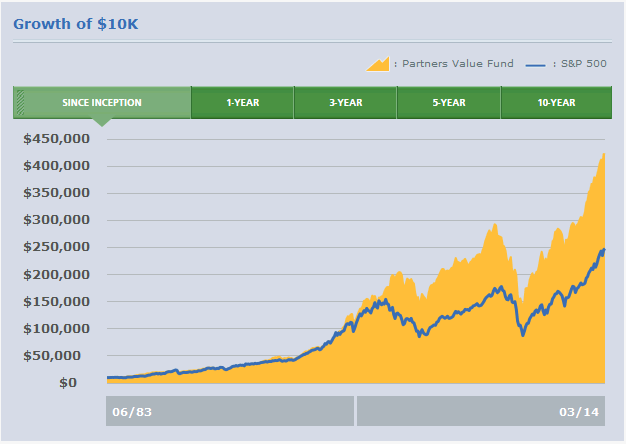

Tom, you are correct: there are almost no managers who can beat a half decent P123 strategy. Man is no match for machines. It’s just not a fair fight. Just ask the person who runs Google’s self driving cars. But there are a handful of managers who can beat their index. While Weitz is not Buffett by any stretch of the imagination, he has outperformed the S & P 500 and Russell 3000 by 1.7%/year since inception in mid 1983. This is while holding ~20% in cash as a hedge. (You can also argue that the first few years don’t count as he improved since then after learning some lessons, but I am not figuring that into my calculations). He also puts in about 5%/stock which means that he is limited to the Russell 1000 or so at best.

And that’s the rub, according to Warren Buffett 2%/year over the market is huge. There are a very small handful of mutual funds who can do that through skill. And yet, you could argue that with a 2% edge over the market he doesn’t beat the market after taxes, and you may be right. But again, I chose Weitz not as someone with whom to invest with but as someone who has skill and to illustrate this point of mean reversion.

P.S. His stats tell me that there is a 75% probability that he is skilled if you look at yearly returns.

After some more research, the VXX ETN (and it’s inverse; the XIV ETN) are supposed to track a blend of 1 month and 2 month futures for a weighted maturity of up to 60 days. The ^VIX index is supposed to track 30 day volatility, while the ^VXV index is supposed to track 90 day volatility. That means that the ^VIX/^VXV ratio is an imprecise way of measuring the contango for the ETNs.

Fred, P123 does not need to reinvent the wheel themselves. Accurate backfilled data on the ETNs and the indexes are available on the web for a price that is reasonable for P123.

Aurélien, you are correct, that’s what Barclay’s claims. However, since VXX actually blends the volatility futures of Month 1 and Month 2, the maturity of VXX is the market is willing to pay for what volatility will be in 60 days. That’s why it doesn’t match the VIX precisely. See Barclays’ VXX—Not as Short Term as You Think.

To quote from that article:

The author of that article (Vance Harwood) has actually reconstructed the VXX using this criteria and has claimed that his data is accurate to within ~0.05% or so (I don’t remember his exact figure).

I subscribe to “The Option Strategist” by Larry McMillan http://www.optionstrategist.com/ and trade a number of his option strategies including volatility term structure.

Here is a video where Larry walks through the various CBOE and ETN products, how they’re calculated, trading pitfalls and hedging tips that really matter when trading volatility. I learn a lot from his newsletter about trading volatility and this video shows he knows his stuff… http://www.youtube.com/watch?v=p_jlUOqjGXg