Hi Andreas,

I used regression to answer this question here: I really wish factor momentum would work - help me show that it actually does - #4 by Jrinne. Using linear regression, I found that over a month's period, value ratios and earnings estimate revisions were more likely to tend than other factors I looked at. Most factors mean-reverted over that period.

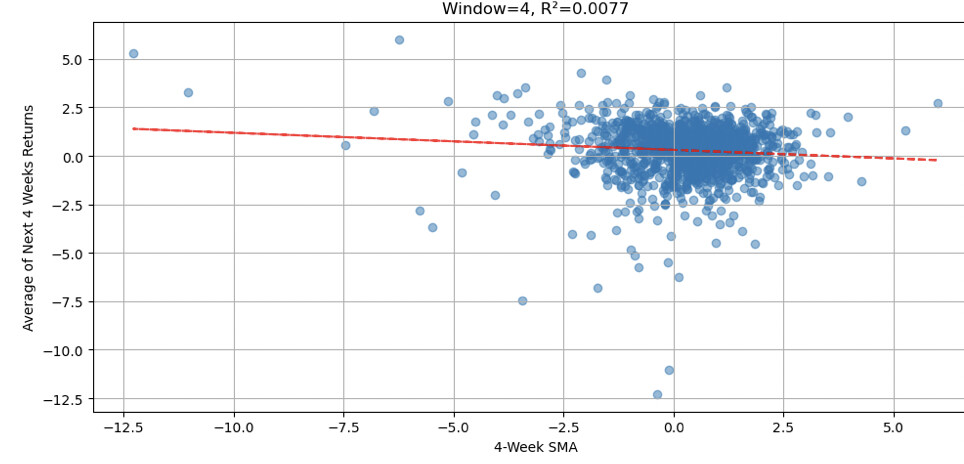

Specifically, I used 4 weeks of returns to predict the next 4 weeks of returns. Here is an example of a factor that mean-reverted. Here the regression line had a negative slope. At the far left of the graph, the 5 data points with the worst 4 weeks (on the x-axis) went on to have some of the best months going forward (the y-axis). None of those 5 data points showed negative returns.

But one could argue for a U-shaped curve with this data which would be one reason to use KNN as it does not assume linearity. Looking at the scatter plot, extreme negative returns (left side) AND extreme positive returns (right side) both tend to be followed by positive returns, suggesting a U-shaped relationship. However, it gets more difficult to classify a factor as just trending or mean-reverting when encountering U-shaped curves. While less descriptive, KNN methods may have more predictive power when data is not always linear.

The data I presented in this post supports a significant improvement in predictive power using KNN compared to linear methods: I really wish factor momentum would work - help me show that it actually does - #10 by Jrinne

Jim