It tried but...

Trending versus Mean Reversion in Factor Returns: A Technical Analysis

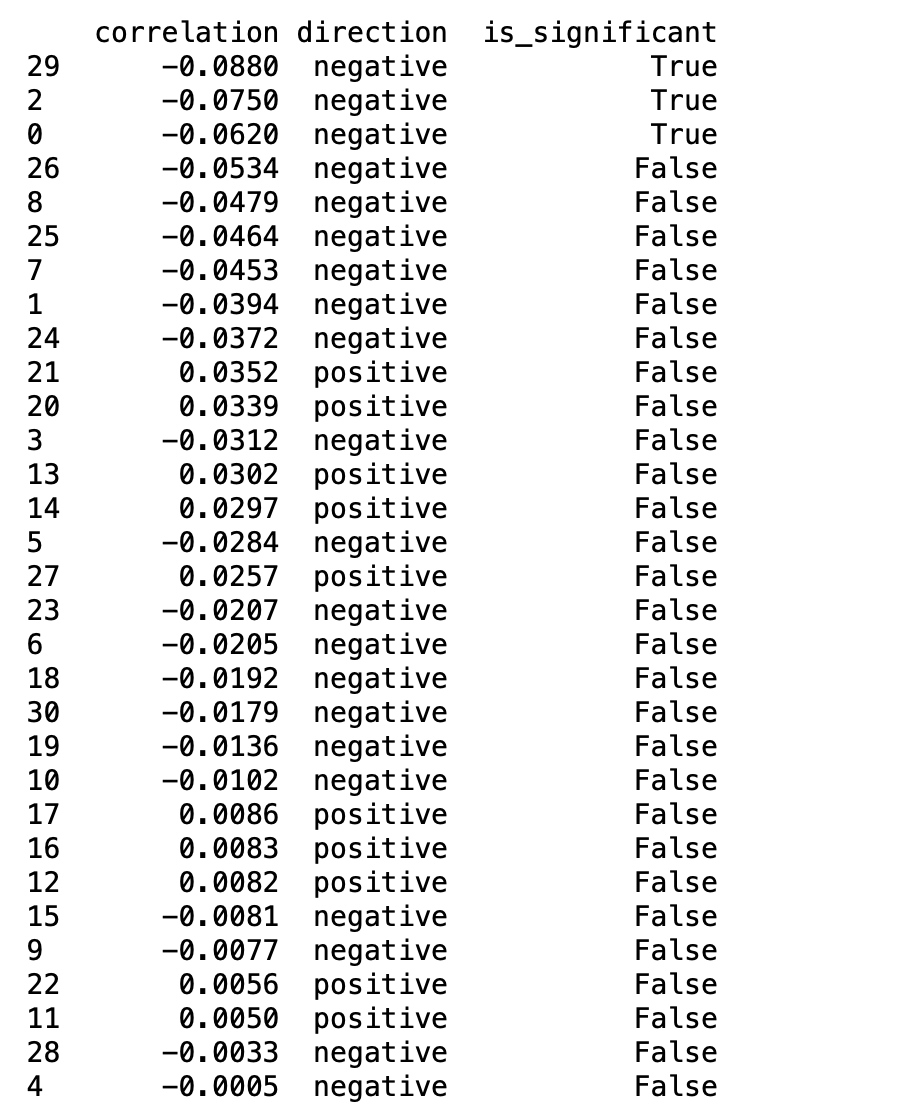

I analyzed the weekly returns of the top bucket for 31 different stock market factors to investigate their predictive properties. The key finding: weak predictive relationships (three statistically significant) with mean reversion dominating. NOTE: you would expect a few statistically positive tests of 31 factors, with multiple window sizes tested, by chance alone.

Methodology:

- Tested if the SMA over a period predicts average returns over the next 4 weeks

- Grid search for optimal SMA window sizes: [4, 8, 12, 16, 20, 24, 28, 32 weeks]

- Used linear regression to test predictive power

- Analyzed correlations, p-values, and statistical significance

Key Findings:

-

Evidence of weak predictive relationships:

- Correlations range from -0.0880 to +0.0339

- Three factors show statistical significance (p < 0.05)

- 21 of 31 factors show negative correlations (mean-reverting tendency)

- All best performing windows were 4 weeks

-

Window Size Analysis:

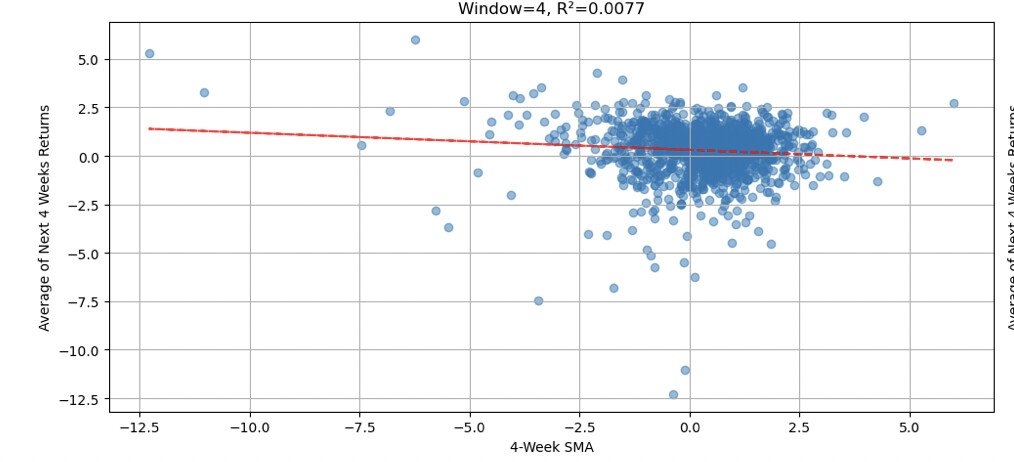

- 4-week window emerged as optimal for all factors

- R-squared values all below 1%

- Predominantly negative correlations suggesting mean reversion

Results table (name of factors removed):

Most significant regression results:

Code included for transparency and replication.

import pandas as pd

import numpy as np

from scipy import stats

import statsmodels.api as sm

import matplotlib.pyplot as plt

import seaborn as sns

def analyze_predictive_power(data_series, window):

"""

Analyze predictive power of SMA for average of next 4 weeks' returns

"""

# Calculate SMA

sma = data_series.rolling(window=window).mean()

# Calculate average return over next 4 weeks

forward_returns = pd.concat([data_series.shift(-i) for i in range(1, 5)], axis=1).mean(axis=1)

# Remove NAs from both series

sma = sma[window:-4] # Remove first window periods and last 4 periods

forward_returns = forward_returns[window:-4] # Align with SMA

# Run regression of forward returns on SMA

slope, intercept, r_value, p_value, std_err = stats.linregress(sma, forward_returns)

# Calculate correlation

correlation = sma.corr(forward_returns)

return {

'window': window,

'slope': slope,

'p_value': p_value,

'r_squared': r_value**2,

'correlation': correlation,

'std_err': std_err,

'direction': 'positive' if slope > 0 else 'negative',

'is_significant': p_value < 0.05

}

def analyze_all_metrics(data, windows=[4, 8, 12, 16, 20, 24, 28, 32]):

"""

Analyze predictive power for all metrics

"""

all_results = {}

significant_predictions = []

# Analyze each column

for column in data.columns:

if column != 'date':

print(f"\nAnalyzing {column}...")

# Test each window size

window_results = []

for window in windows:

result = analyze_predictive_power(data[column], window)

window_results.append(result)

# Convert results to DataFrame

results_df = pd.DataFrame(window_results)

all_results[column] = results_df

# Track significant predictions

best_window = results_df.loc[results_df['r_squared'].idxmax()]

if best_window['is_significant']:

significant_predictions.append({

'metric': column,

'window': int(best_window['window']),

'r_squared': best_window['r_squared'],

'direction': best_window['direction'],

'p_value': best_window['p_value'],

'correlation': best_window['correlation']

})

return all_results, significant_predictions

# Read and prepare data

file_path = "insert_your_path" # Replace with your file path

data = pd.read_csv(file_path)

data['date'] = pd.to_datetime(data['date'], format='%m/%d/%y')

data = data.set_index('date')

# Perform analysis

all_results, significant_predictions = analyze_all_metrics(data)

# Create summary of best windows for each metric

summary_data = []

for metric, results in all_results.items():

best_result = results.loc[results_df['r_squared'].idxmax()]

summary_data.append({

'metric': metric,

'best_window': int(best_result['window']),

'r_squared': best_result['r_squared'],

'p_value': best_result['p_value'],

'correlation': best_result['correlation'],

'direction': best_result['direction'],

'is_significant': best_result['is_significant']

})

summary_df = pd.DataFrame(summary_data)

summary_df = summary_df.sort_values('r_squared', ascending=False)

# Print summary results

print("\n=== Summary of Predictive Power Analysis ===")

pd.set_option('display.max_rows', None)

pd.set_option('display.float_format', lambda x: '%.4f' % x)

print(summary_df)

# Create visualization of top metrics

plt.figure(figsize=(20, 15))

# Select top 6 metrics by R-squared for visualization

top_metrics = list(summary_df.head(6)['metric'])

for i, metric in enumerate(top_metrics, 1):

plt.subplot(3, 2, i)

# Get best window for this metric

best_window = int(summary_df[summary_df['metric'] == metric]['best_window'].values[0])

# Calculate SMA and forward returns

sma = data[metric].rolling(window=best_window).mean()

forward_returns = pd.concat([data[metric].shift(-i) for i in range(1, 5)], axis=1).mean(axis=1)

# Remove NAs

sma = sma[best_window:-4]

forward_returns = forward_returns[best_window:-4]

# Create scatter plot

plt.scatter(sma, forward_returns, alpha=0.5)

# Add regression line

z = np.polyfit(sma, forward_returns, 1)

p = np.poly1d(z)

plt.plot(sma, p(sma), "r--", alpha=0.8)

plt.title(f'{metric}\nWindow={best_window}, R²={summary_df[summary_df["metric"]==metric]["r_squared"].values[0]:.4f}')

plt.xlabel(f'{best_window}-Week SMA')

plt.ylabel('Average of Next 4 Weeks Returns')

plt.grid(True)

plt.tight_layout()

plt.show()

# Print key insights

print("\n=== Key Insights ===")

print(f"1. Total metrics analyzed: {len(summary_df)}")

print(f"2. Metrics with significant predictive power: {len(significant_predictions)}")

print("\n3. Top 5 most predictive metrics:")

print(summary_df.head().to_string())

# Additional analysis of significant predictors

if significant_predictions:

print("\n4. Metrics with significant predictive power:")

sig_df = pd.DataFrame(significant_predictions).sort_values('r_squared', ascending=False)

print(sig_df.to_string())

else:

print("\n4. No metrics showed significant predictive power")

# Create correlation heatmap for top metrics

top_10_metrics = summary_df.head(10)['metric'].tolist()

corr_matrix = data[top_10_metrics].corr()

plt.figure(figsize=(12, 10))

sns.heatmap(corr_matrix, annot=True, cmap='coolwarm', center=0)

plt.title('Correlation Matrix of Top 10 Predictive Metrics')

plt.tight_layout()

plt.show()

# Save results

summary_df.to_csv('predictive_power_analysis.csv')

if significant_predictions:

pd.DataFrame(significant_predictions).to_csv('significant_predictors.csv')