There’s been a lot of discussion about market timing and hedging to reduce risk. I won’t rehash all of the points, but generally agree with Marc Gerstein’s views, as I am skeptical that market timing rules will be effective out-of-sample.

It seems that the average retail investor is looking for performance similar to a hedge fund, or at least what most hedge funds are attempting to achieve, which is equity-like returns with bond-like risk. Many of the better models that I have developed (and seen in P123) can achieve high returns, but with either higher risk or similar risk to equity indexes. While market timing works well in backtests, in my opinion, the best tool for reducing risk is good ol’ fashioned diversification, namely using a healthy dose of fixed income.

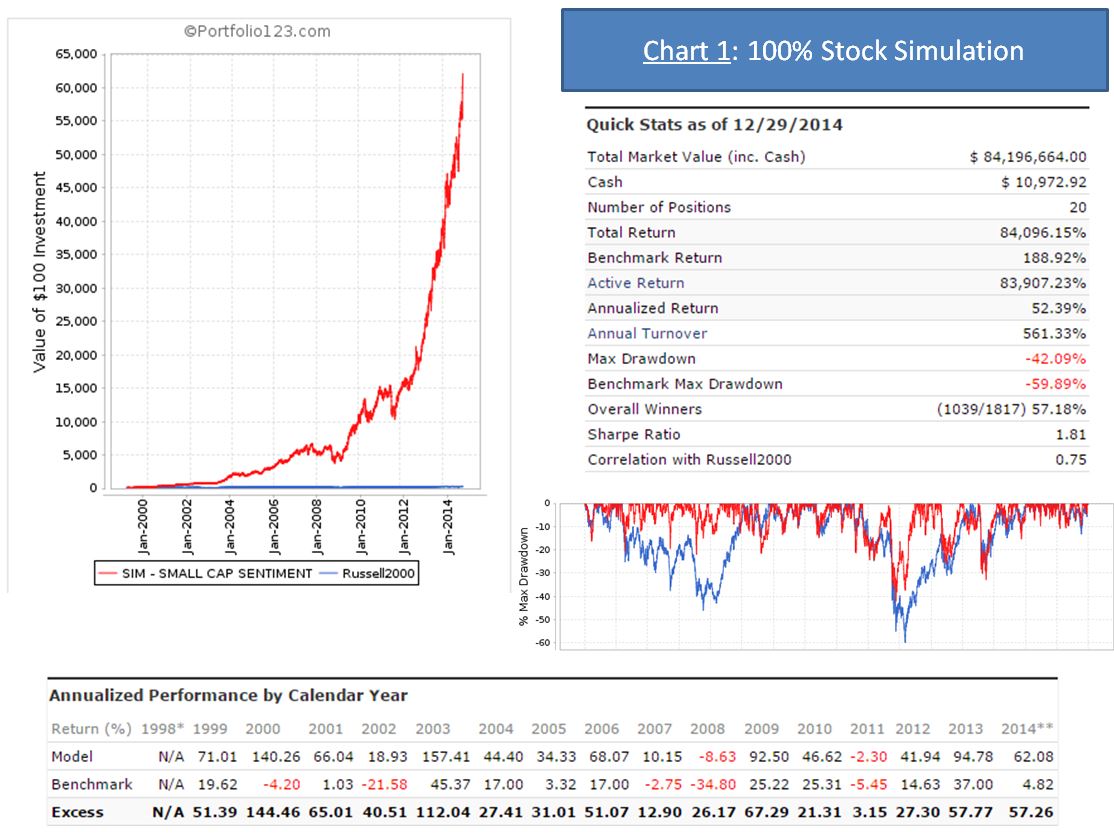

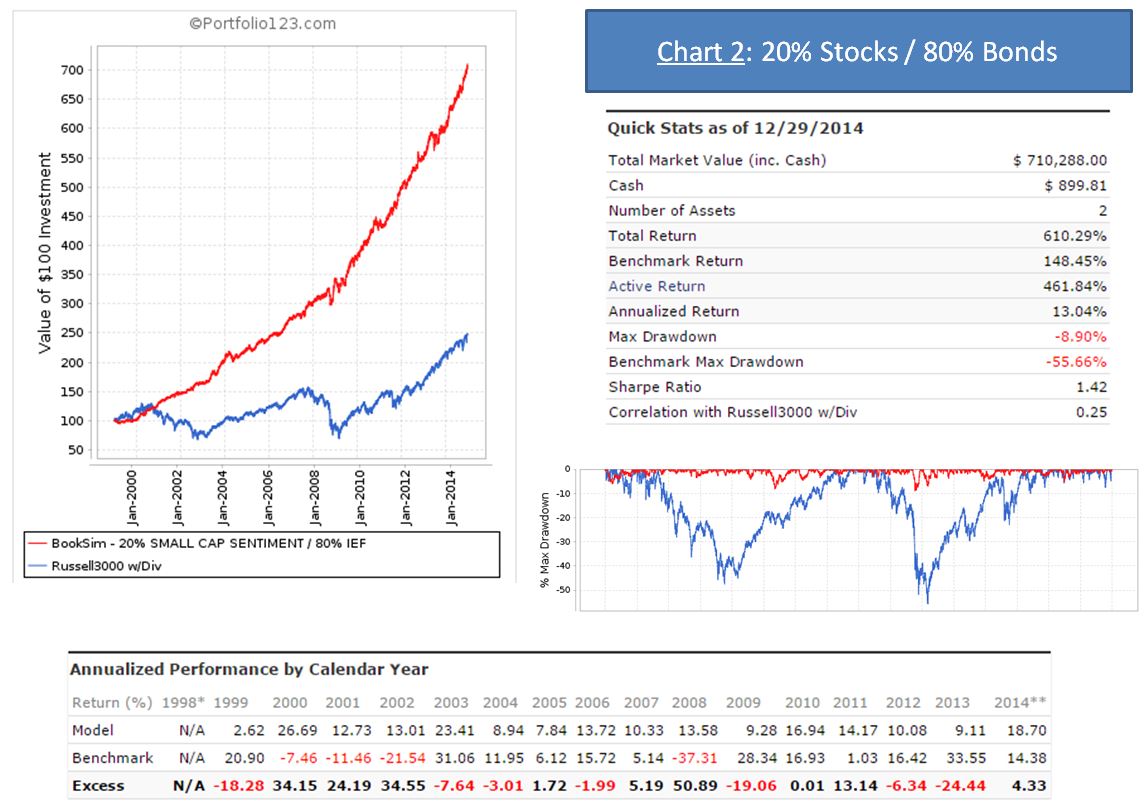

As you can see in Chart 1 below, a model with high returns may also have unacceptable risk for most retail investors. But, if an investor wanted to target <10% maximum draw downs, they could simply hold 80% in a bond ETF, and still achieve much higher returns than an equity index (at least for this simulation), as shown in the book simulation in Chart 2.

Holding a fixed allocation in bonds to reduce risk is: (1) transparent; (2) based on sound financial theory, as bonds have relatively low correlations with equities; and (3) very straightforward to implement and understand with no leverage, shorting or derivatives.

It may be helpful to allow book simulations for R2G models that hold a fixed allocation to bonds or other asset classes to reduce risk. It may also be useful to allow for spliced benchmarks, to reflect a multi-asset class benchmark that may include both equity and fixed income.

Any thoughts?