Momentum is often cited as one of the most consistent and pervasive investing factors along with value. I all my time with P123, I have never come up with any reasonable momentum metric that didn’t make results WORSE. Often times negative momentum seemed to be a more reliable factor. Any momentum systems I have seem that claim to work, seem to very sensitive to any “tweaks”, and are easily broken down with a few changes in parameters. Any thoughts?

It doesn’t seem to work great in the P123 sims from what I tested. I think it’s mostly caused by alpha erosion over the last decade. I remember back in 2005 when O’Shaughnessy promoted that factor style with his quote “A winner will continue to be a winner” and the ROC 12 months. Market participants began trading based on that metric at the end of the month, then as too many market participants looked into it, people started to find ways to front run the other funds by looking at the ROC 11 months to have a faster signal and glimpse at what the ROC 12 months might print a month later. And so on until the alpha got eroded away. It was probably easy money back in the days but lately it’s not all what it used to be.

This guy wrote a piece on using 200d MA for timing but also talks about its use for individual stocks and why it works on markets but not individual securities. (I think his ideas are related to the concept of price momentum.)

http://www.philosophicaleconomics.com/2016/01/movingaverage/

As a side note, I think we use the idea of momentum (that is, something will continue in its direction based upon its speed and mass) for fundamental analysis. We think that if a company has had good ROE in the last 12, 24 or 60 months, that whatever luck/good management gave rise to this will (probably) continue and therefore we look more favorably on the stock to do well in the near future, based upon its recent past. So ‘momentum’ in that context sounds right to me. But like you, I have had little luck with incorporating price momentum in my strategies. But if people use it successfully, more power to them.

I find that momentum in one form or another helps my models avoid “value trap” stocks.

Of my 3 best models with over 4 years real money history, 1 has a ranking system that gives 35% weight to price momentum. The other two models don’t have price momentum in their ranking systems, but they do have a buy rule that checks to make sure there is no “negative” momentum over the recent past (3 months).

In all three models, I’m using momentum in one way or another to avoid “value trap” stocks, ie, stocks that temporarily appear to have great value ratios because the price has fallen (in the denominator of the ratio) but the fundamental factor (in the numerator of the ratio) has yet to be updated to a lower number. The falling price action of the market is a signal to me that the fundamental value is “suspect” if not “wrong”.

Brian

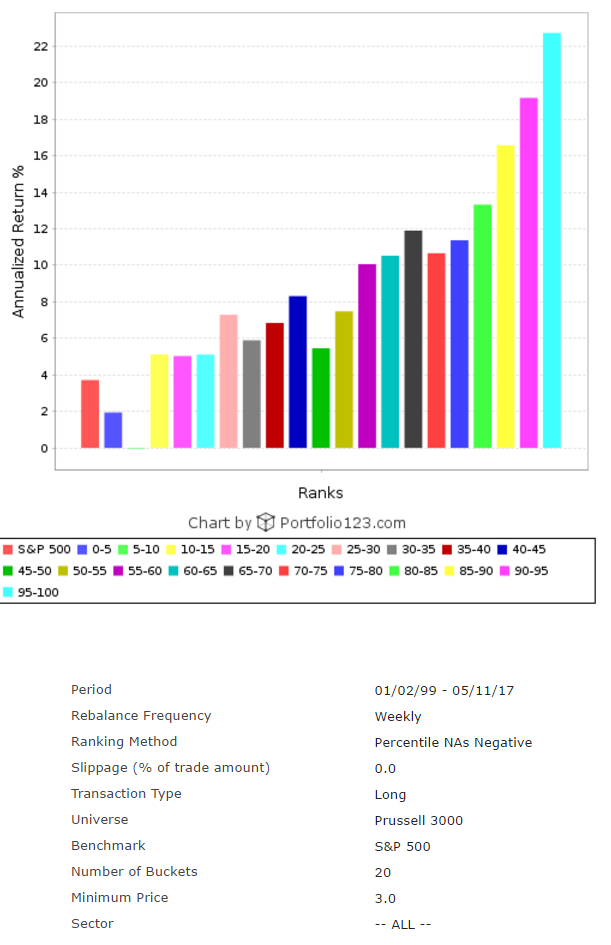

https://www.portfolio123.com/port_summary.jsp?portid=1290029 is a pure momentum play.

It works since 2003 in realtime (on another Plattform), over 20% p.a. on big cap stocks.

Also I combine momentum with value on my small caps and that (as posted by Brian) indeed makes sure, that

the value factor does not buy “dead value”…

though momentum stocks get usually destoryed on market turndowns…

add this to your ranking and try if it works

vma(150)/vma(300) ema(50)/ema(100) avgdailytot(20)/avgdailytot(120) Sharpe(120,1)Personally, I have found low SI%float and low volatility to be much better factors combined with value to avoid “value traps”

In my opinion, momentum is probably here to stay, though I think it will look differently in the future than in the past due to the proliferation of rational, risk-neutral, edge-seeking algorithms. Herein, momentum refers only to price momentum. It is the same thing as a trend. Fundamental momentum is arguably fundamentally different since it it relies on the inertia of good managerial execution.

Anyhow…

Momentum is the “greatest embarrassment” to the theory of efficient markets, according to Eugene Fama. It’s mere existence implies a free lunch, i.e., excess return which is not related to cost and/or risk. A weak form of EMH can allow the existence of excess returns when a thing is “under-valued” and/or “under-loved”. However, no one, in my opinion, has given a rational explanation for momentum to exist. Dr. Wesley Gray of Alpha Architects believes that it is “under-reaction to good news”. Behavioralists such Dick Thaler, Dan Kahnemann, and Amos Tversky have given possible “irrational” reasons for the human tendency to “buy higher”.

Momentum was added to the Fama-French framework as a result of Carhart’s 1994 paper. It has been canon until 2016. In the recent iteration of the Fama-French Model, momentum was dropped in favor of metrics for beta, size, value, profitability, and investing style. When all these factors were considered together, the predictive value of both value and momentum fell by the way-side. Eugene Fama and Kenneth French had to pick one of those things top drop: the obvious choice momentum – that thing which was the thorn in their sides.

AQR’s Cliff Asness went the other direct and instead posits that a six factor model saves both value and momentum from redundancy.

Does momentum exist? It has… in most markets, anyway. But – because it has been predicated on discontinuous and non-linear behavior – I do not think it is a steady-state phenomenon such as a physical constant. Moreover, the growing use of automated investment decision tools which recognize momentum will likely change its behavior going forward. Hypothetically, machines which jump on and off trends more quickly suggests that future price trends will tend to look less like “momentum” and more like “jumps”.

Although the “jump” hypothesis is pure speculation, I am curious as to how one would recognize an unannounced jump before it happens. Ideas?

I guess my point is, I know there are lot of studies pointing to the validity of momentum, but I have not been able to come up with, or even seen any, robust momentum based strategies demonstrated with P123. As others point out adding a momentum factor with a meaningful weighting to a ranking system often reduces return.

@Charles123. The opposite of momentum is mean-reversion. How can they co-exist? What information regarding one drowns out the information contained within the other? As a general rule: momentum happens over longer periods, while reversion takes place over shorter periods.

Are you looking for specific rules?

It would be interesting to see a non-market-timed sim of 50 stocks based price momentum only that looks decent.

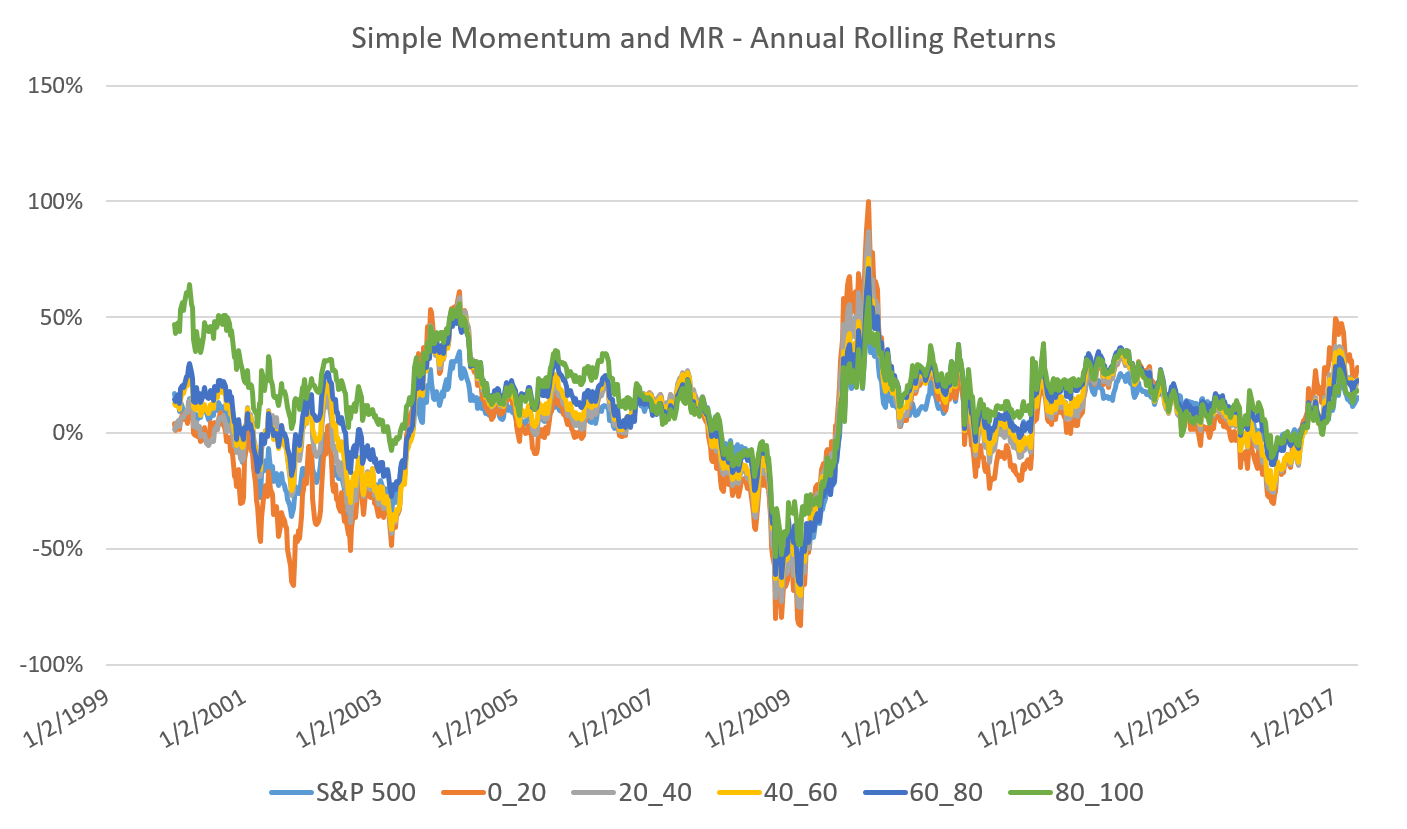

These are some results of a simple 2 factor momentum - mean-reversion model. I am reluctant to share too much of my sauce. Interestingly, the results look good over the period (1991-present), but bad recently. Momentum gained wide acceptance in 1994 through Carhart’s factor model… notice how in the rolling returns chart, the performance spread becomes increasingly narrow.

So, I could design a seemingly good system which performs well since 1991, but I shouldn’t necessarily expect to do so well going forward.

In my experience, momentum works better as a screener rule than as a part of a ranking system. My guess is that in a screen, you’re saying “of these stocks that are going up, which have the best fundamentals”. In a ranker, the momentum component pulls weight from the fundamental component, which must be more important. But that’s just a guess.

A few quick comments.

-

Momentum works, as Marc pointed out a while ago, because companies that have done well over the last few quarters are more likely to do well in the next quarter than those that have done badly. To use an analogy, a high school student who has gotten several A’s in the last few semesters is more likely to get an A next semester than a high school student who has gotten C’s.

-

Momentum coexists with mean reversion. There’s not really a contradiction between them if you think of things this way. Break up time into units of varying lengths. Let’s say, for example, we break time up into the following units: 1 hour, 1 day, 1 week, 1 month, 1 year, 1 decade. Then perform a test on each unit as follows. If the price rises during the unit, is it more likely to continue to rise the next unit, or more likely to fall? Because the averages will be pretty close to 50%, most units are going to exhibit averages between 45% and 55% in one direction or another. But they will ALL be slightly off from 50%. For each unit of time, then, we can characterize the average as either momentum or mean-reversion. In my limited experimentation, 10 months definitely leans toward momentum and 3 weeks definitely leans toward mean reversion. And there are good reasons for this, reasons that aren’t arbitrary, that make a lot of sense. The reason for momentum I gave above; the reason for short-term mean reversion is that investors have a tendency to overreact to news.

-

Try VMA(15)/VMA(210) with a weekly rebalance. I think you’ll find that it works pretty well as a single-factor momentum strategy.

-

The S&P 500 is a momentum index. Think about it. If a stock’s price falls too much, it leaves the index. If a stock isn’t in the index and its price rises, it enters the index.

-

I know some people here use momentum along with value in a single ranking system to great effect. I have not been able to myself. Every time I throw momentum into the mix, value goes out the window. To me, they’re two opposite strategies, and shouldn’t be mixed. Devote part of your portfolio to each if you want. But a good value investor tries to buy at the lowest possible price, and that’s not going to happen if you have a momentum factor in your ranking system.

I like this A LOT. Simply put and it has to be right: a theorem.

-Jim

The word “momentum” is actually less informative than we realize. You can experience big differences depending on whether you measure it over longer or shorter time frames. Also relevant is how much time you give your “buy” stories to work. Don’t assume daily or weekly re-balancing is best.

Also, we have to remember that no stock ever does anything in a straight-line fashion. Others in this thread used the phrase mean reversion. Regardless of label, any tend you see is really built with lots of zigfs and zags, and many momentum investors have found it fruitful to capture this by investing in momentum but times to match a recent pullback. So it’s entirely possible that capturing peak momentum might be the worst thing to do.

Also in this thread you’ve seen comments about incorporating additional factors. That’s part of the logic that lies underneath momentum. In truth, pure momentum (a stock moves up in the future because it moved up in the past) is pure fiction. In truth, the stock moved up in the past for reason A, or reasons A, B, C, etc. and moves up in the future because A or A, B, C remain valid. Fundamental analysis goes after A, B and c. Momentum rides piggyback atop those who do but without necessarily looking into A, B and C. Those who’ve written here about combining momentum with other factors are, in essence, doing both of the above; they’re looking at momentum, but verifying what they see by also looking at the reasons behind the momentum, which, I think, is a pretty good way to go. (It’s a way to try to increase the probability that past momentum will carry into the future.)

Isn’t that pretty much the secret sauce as to why the SP500 Index is so hard to beat for stock pickers? The cap weighting creates a covert systematic momentum strategy.

“Isn’t that pretty much the secret sauce as to why the SP500 Index is so hard to beat for stock pickers? The cap weighting creates a covert systematic momentum strategy.”

Yes, I have wondered about that too. Is this being amplified with so many people piling into SP500 index funds?

This discussion raises an interesting question: if you could change the methodology for the S&P 500 (i.e., market-cap weighted), would you, and what would it look like? In other words, is there a “better” index available, one that is either, A) scalable enough to reflect the aggregate income stream for a modern global economy, or B) optimal for creating wealth for the owners of that index?

To my mind this question is not just theoretical but practical in nature, as the answer may suggest the long-term upper performance limits for any alternative approach - assuming the market-cap index isn’t the answer, which it may be.

Duplicate

Duplicate.