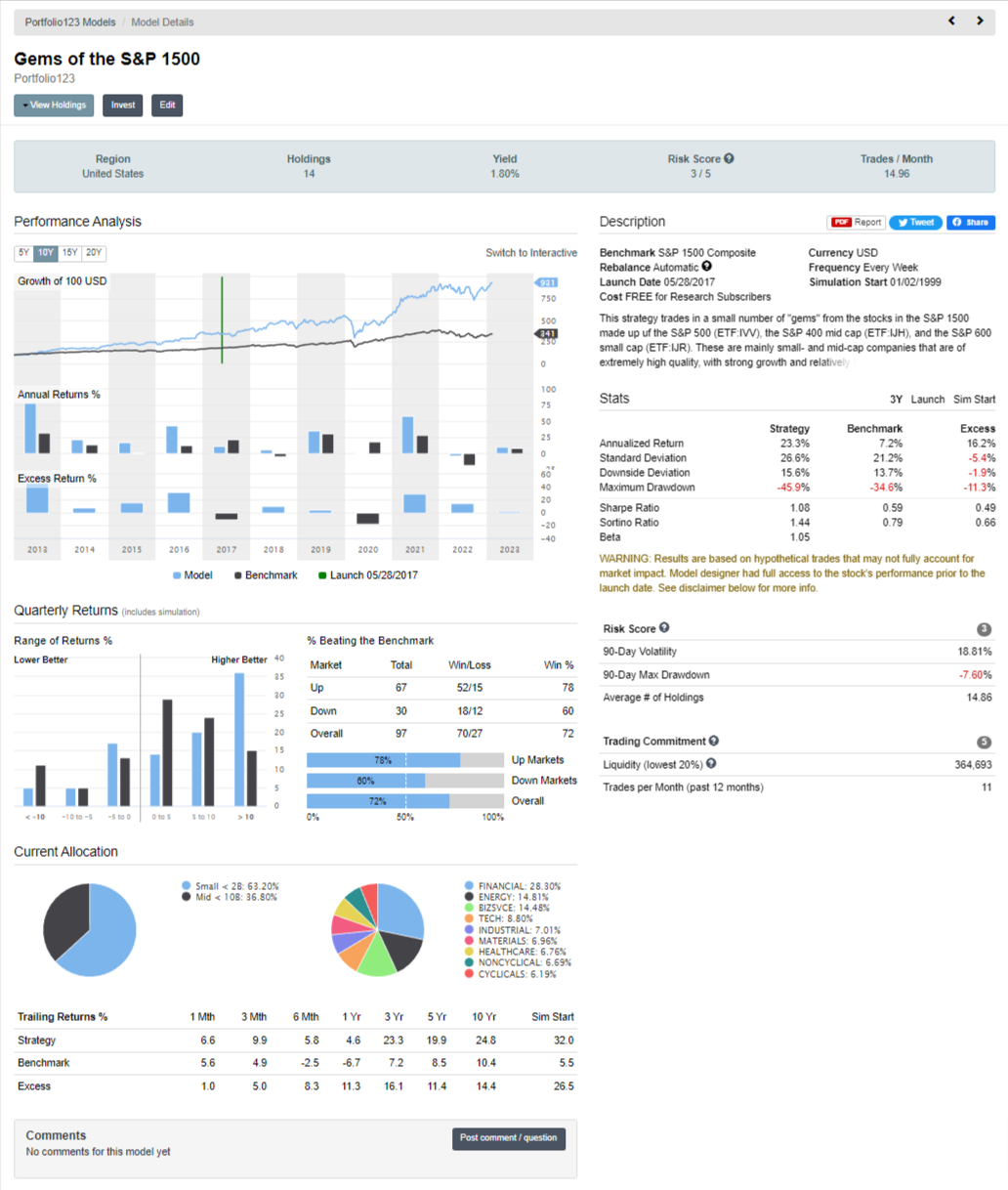

We launched the redesigned presentation of pre-built models that you can subscribe to and invest. We’re using the same presentation for Designer Models and our P123 models (which now require a subscription). See image below for an example.

A PDF report button has been added as well. User can download the report and share it for example. So you might want to add your own logo and info. Just go to your model and click the gear next to the PDF button.

We’ll be brainstorming more ideas to make this model marketplace popular. There’s appetite, users want models, but it has not taken off. We think that it still requires too much effort from the user. These are the top two planned upgrades we decided on:

Automatic investing via a linked broker (user can “set it and forget it”)

Discretionary rebalances

The second one will allow designer full control of the rebalance with new redesigned rebalance pages. These pages will show you a lot more information than existing one including for example stocks that were skipped and why. Dev work has begun, so should happen soon.

B/c as a designer, I regularly select through all my models to see how they’re performing since launch. There’s no easy way to look at that performance under the Research section. Perhaps P123 could update the live strategy presentation to include a marker of when the model was made live.

As a subscriber to designer models I rely heavily on being able to calculate the following for any time period:

Average profit per trade

Percent winners and losers.

Average days held

This is how I compare models to see if my trading style fits with the model. I use to use the 30 day lag of current holdings to do this but it’s gone and you don’t offer any other way of calculating these metrics. These in my opinion are the most important metrics. A system with 70% winners and an Average profit per trade of 0.5 % is much different than a system with 60% winners and an average profit per trade of 15%. I think you know which one I would choose with all else being equal. Even if you don’t show previous trades I just need the metrics. Is it possible to add these to the reports? Maybe in the future you can add them to the filters but that would be getting greedy.

Marco - quite an impressive interface, but you are starting to prominently display the back simulation period again which is irrelevant and misleading. The only results that constitute performance are post-launch.

No, no, it’s not like before. First of all the stats that you can search & rank DM’s are still based on since launch only. That was the biggest problem in version 1.

You only see the backtest performance once you click on the model. But now something new makes a very important characteristic obvious: how did the model do after launch vs simulation?

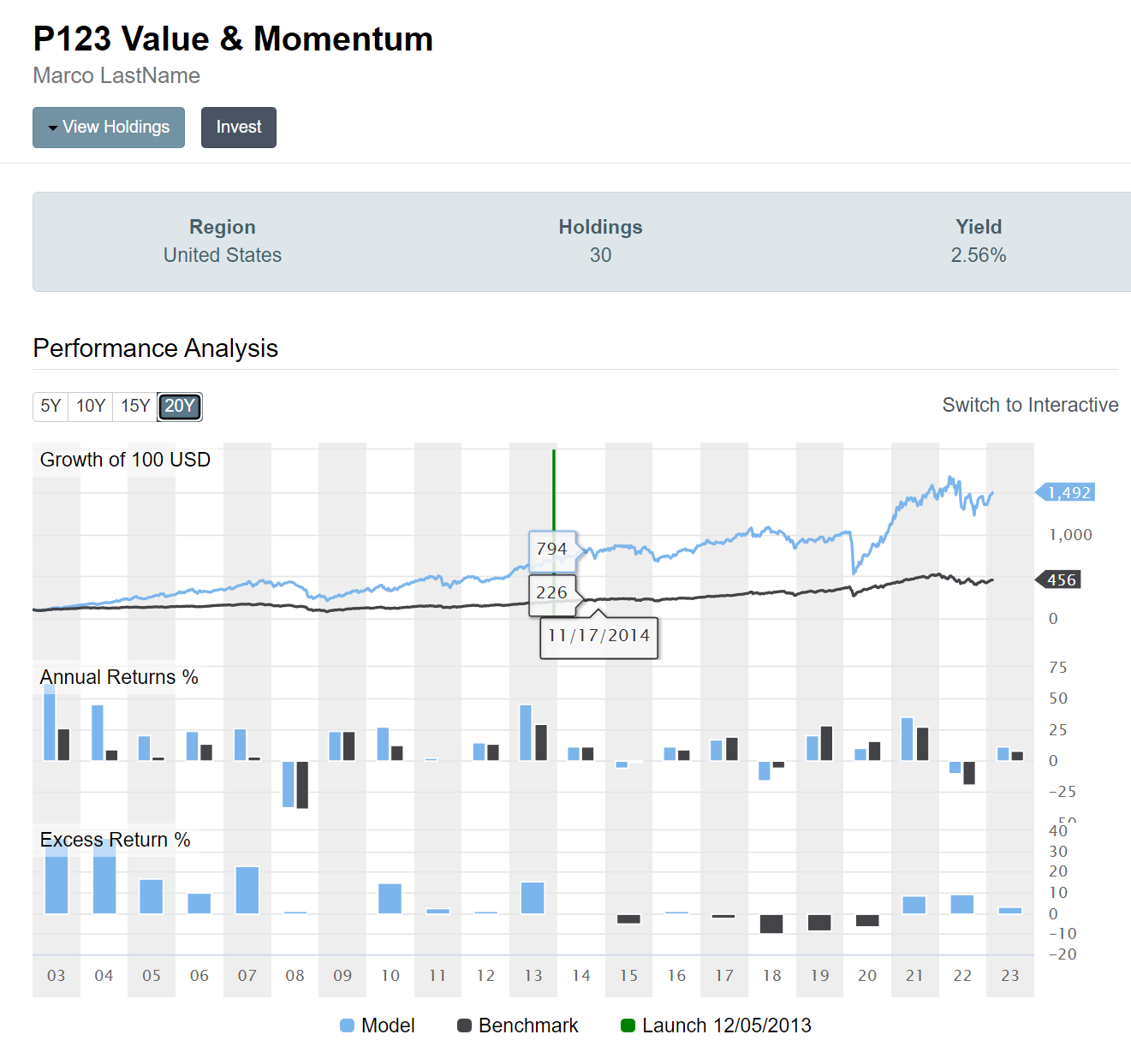

See my “crappy” model below. With the new “Excess Return %” it’s very clear the difference. All blue bars before launch; much, much different after launch. Mostly underperforming every year. Now, my model may not be total junk. Could be that the factors I chose were in favor in the past, but the next 7 years after launch they stopped working (things do tend to work in cycles of 7 years).

In any event, this was the design that won me over.

NOTE: It’s ok to have tremendous backtest and “ok” post launch. Backtests will always be great, like a big huge diamond. The post launch is ok that it’s a smaller diamond. What you really want to see is excess return, and the new design makes it very clear.

Marco - you are making an assumption that all strategies are developed in the same fashion. i.e. create a strategy that works for all time and market conditions and use a backtest to demonstrate its performance for posterity.

In reality, the developer may want to change his model based on market conditions and may simulate a particular time period that he believes is representative of the current market conditions. What value is there in providing a backtest given such a strategy? Or the developer may choose to employ a strategy of optimizing for the recent past. Yet, he is forced to provide a ten-year backtest as if there is some relevance in terms of “performance”.

I gather from reading your posts that there is going to be greater flexibility in modifying models, so the backtest becomes even less relevant. What is important, is how the model provider navigates markets, and that is not captured in backtests, only through performance post-launch. And it doesn’t matter how many times the model is revised. The performance is irrefutable.

How should a potential subscriber interpret the graphs below, without understanding the developer’s development strategy?

It is calculating the liquidity for each stock on the buy date of the stock’s transaction in the simulation. Then it takes the lowest 20% of those liquidity calculations and computes the average. That average must be > 150000 USD. So add a liquidity rule using either MedianDailyTot() or AvgDailyTot() to your universe or simulation Buy rules which is set high enough so that your simulation passes this liquidity rule when you try to create it to a Designer model. I dont want to give you the exact liquidity calculation because you would not be doing your potential subscribers a favor by creating a simulation that just barely squeaks past the liquidity rule.

Inspector,

Hm…I am wondering if you are making a valid point. 10-years back period is a good time frame to get a “feel” for a model (of course with no guarantee of anything, as usual).

In reality, the developer may want to change his model based on market conditions and may simulate a particular time period that he believes is representative of the current market conditions.

I can’t think of any market condidition that resembles a “particular time period representative of current market conditions”. All current market conditions are somewhat different from the past. No past situation is equally similar to a current one to base a strategy on, inmho. The stock market is a chaotic beast and has a tendency to surprise us all the time.

I agree that these are important stats to include. All else being equal, I’d rather not invest in a model that has an average return of 1% - 2% per trade. How about reporting the average return per trade and it’s distribution? A low average could indicate large (small) losses against large (small) gains. Having some measure of return distribution would be informative.

Hi Werner - Optimizing for specific time periods is a legitimate practice and has been discussed at P123 in the past. Just because you can’t find similar market conditions to today, that doesn’t mean it wasn’t possible 3 years ago when a model was released. Even with today’s market conditions, I may choose to follow a strategy that appears as an emerging trend. For example, “(Sales) Growth at all cost” is over, but “Max growth Sales + Earnings” is starting to emerge. Should I not release or update a model based on the new trend? The way the models are being presented now, I feel the developer needs to justify the last 10 year’s performance when it isn’t even relevant. And the potential for misleading performance is being re-introduced.

At the very least, it should be the developer’s choice whether backtest data is released to the public, and the choice should be made based on how the model was developed or modified.

Seeing the two years post launch I would not invest in this model without knowing who’s behind it intimately.

To avoid a repeat of the problems we had with version 1 of DMs, the quick fix for now is to just hide backtest performance until at least 2(?) years have gone by (but still let a user see it if they acknowledge some disclaimer). But again, this model would not show up anywhere in the ranked list, which only uses post launch data.

But there’s no quick fix to the main problem with DMs: the low participation from subscribers.

The most successful designers at the moment don’t need any of this fancy presentations or features. They have their own followers, and market themselves either in our community or somewhere else like seeking alpha.

For the rest, the simple truth is that without 5+ years of out of sample record it’s very hard to get anyone to subscribe. Even with 5+ years since launch is hard to gain subs. Take a look at the top ranked models right now. They look terrific, but have very little subscriber activity.

Why?

Hard to pinpoint. Obviously we are not a platform designed specifically for prebuilt models like a Collective2. So the user that comes to P123 is not initially interested in models. With some more effort I think it will pay off eventually for all involved. In any event the R&D we devote to DMs can be used elsewhere on the site. For example the fully automated integration with a broker is something that will be available for your own strategies.

Marco - maybe just allow the developer to decide whether the backtest is to be displayed. Backtest is a tool, and not meant to be a presentation of performance (which it isn’t in any case.)

One of the problems with DMs is that the market is for the public, not existing P123 subscribers.

There are plenty of people out there that want to follow strategies, but they do not want to put the effort into learning P123 tools. There are things that could be done to improve DM subscribership that have been mentioned before, such as streamlined signup and channels.

Streamlined signup for the public (non-P123 subscribers). A developer may want to advertise his models to the public (Google search, Facebook, etc.) but the signup process has to be focused. The viewer needs to stay on the model page while signing up, not taken somewhere else to subscribe to P123 and given the opportunity to forget about why he/she is there. With the present setup, there is no incentive for developers to spend money advertising outside of P123.

Channels (accessible by the public). This would give developers a voice to discuss their strategies, market conditions, essentially selling themselves without subjecting themselves to P123 members that don’t want that type of promotion.