With SP500 up 50% in the past 2 years and 100% in past 5 years it sure feels over-extended. But that is not the case. I will prove it using our newest relative functions that show that there are still many stocks trading at historically low valuations. If the market was over-extended I'd expect to find a more pronounced skew.

Below are histograms of the relative valuation ranks for Price-to-Sales and Earning-Yield. A flat percentile rank indicates an even distribution of relative valuations.

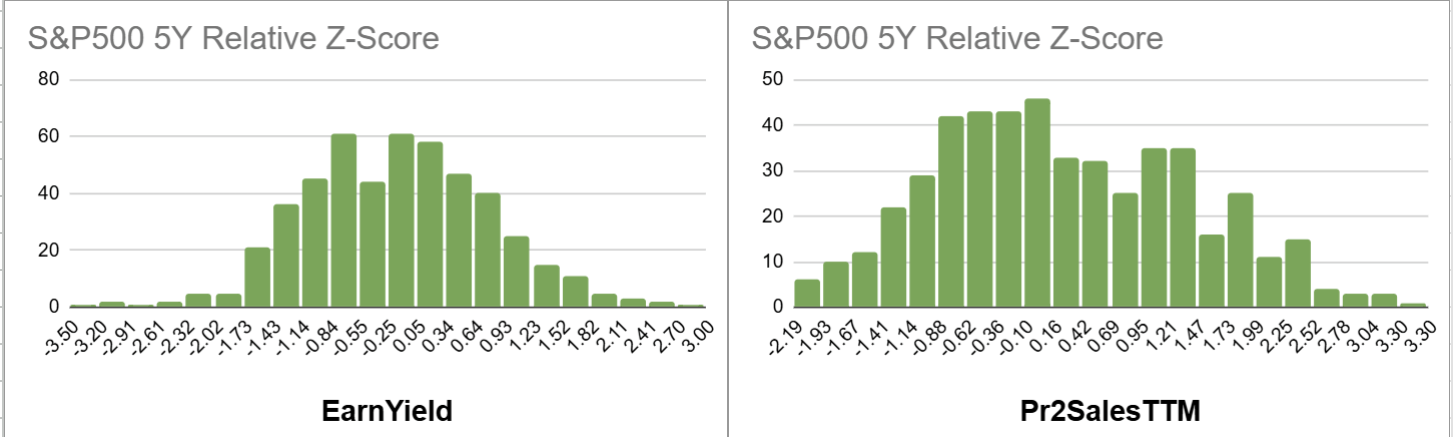

Yes, for Pr2Sales the 95-100 bucket is about twice as large, representing stocks trading in the top 5% of their 5Y historical valuations. But all other buckets are fairly uniform.

For Earnings Yields the lowest bucket is the largest, but otherwise the distribution is pretty uniform.

Below are histograms of the relative 5Y valuation z-scores for Price-to-Sales and Earning-Yield. Both means are close to 0 indicating that there's a balance between stocks trading at historically high vs. low valuations.

The Shiller CAPE ratio for Nov-2024 is at 37.5. Only twice since 1880 has this ratio been that high, in Dec-1998 and Jul-2021, indicating an overvalued market then as it does now.

From Dec-1998 to Aug-2000 the market gained another 25% and then by Oct-2002 it lost 43% from the Aug-2000 high, as measured by the monthly average of the S&P 500..

From Jul-2021 to Dec-2021 the market gained another 7% and then by Oct-2022 it had declined 20% from the Dec-2021 high.

As per the historic precedence the market could possibly gain another 20%, but caution is certainly advisable. The forward 10-year real annualized return is now estimated at only 4.7%.

"But every hero has a fatal flaw. America’s is its sharply increasing addiction to government debt. My calculations suggest it now takes nearly $2 of new government debt to generate an additional $1 of US GDP growth — a 50 per cent increase on just five years ago. If any other country were spending this way, investors would be fleeing, but for now, they think America can get away with anything, as the world’s leading economy and issuer of the reserve currency."

I'm not so sure – the party can usually last much longer than expected.

Looks interesting, but I’m unsure how to monetize it. Could you share a few examples of the new release and highlight the value it adds?

Your cautious stance on many user feature requests makes it seem like you see this new feature as particularly significant, or at least a top priority. I value your opinion so it seems there must be good approach here.

Could you provide a sample showing how this improves results in the AI factor? I remember you sharing the theory of uncorrelated signals. Since we’re now paying for tests in addition to platform fees, guidance on how to use this efficiently would be greatly appreciated.

We have not released these relative functions in AI Factor. It's coming later tonight, or tomorrow at the latest, together with several other AI factor upgrades.

As far as how best to use them, that is T.B.D. We have not used them extensively either. So we're in the same boat, but the boat is still missing some key components.

Relative valuation is one of those components that we realized was missing. We now believe that telling the AI model that a stock is overvalued/undervalued relative to it's own history is as important as comparing the stock to other stocks.

Another component still missing is feature engineering tools. Right now the best you can do is add lots of features and hope the AI algorithm uses the best ones, which is not ideal. We have something planned for this soon.

Rest assured we're not just building tools for the sake of building them, we want to use them too. But often the only way to build anything properly is an iterative process.

In case I want to test this as a factor in a ranking system, what would the best way to do this? For example, ideally I would use rankzscore("opercashfl(ctr,ttm)/max(EV(ctr,ttm), 5)",8) to compare the latest number against the last two years of quarters, but that syntax is not functional.

One thing that I've been pondering lates is how to make apples to apples comparisons between market eras on a macro level when we have a new variable to account for: crypto. One can reasonably say equity valuations are nowhere near where they were during the 90s dot com mania, but a lot of traditional speculative risk seeking behavior that was funneled into things like high risk biotech stocks has now forked off into crypto. Should crypto be taken into account now when judging how frothy markets are getting? Could a collapse in crypto bleed into equity markets given how levered, financialized and institutionalized they've become? Or on the other side of the coin, perhaps crypto is a great release valve for high risk seeking behavior because they're generally walled off from equity markets.

The Shiller CAPE ratio for Nov-2024 is at 37.5. Only twice since 1880 has this ratio been that high, in Dec-1998 and Jul-2021, indicating an overvalued market then as it does now.

Actually, both can be true:

A. 90% of stocks are selling at reasonable valuations.

B. The market cap weighted S&P 500 is near all time high valuations.

That's because the biggest stocks (typically momentum ones) have gone up a ton, while the average stock is still reasonably priced.

I rarely make market calls, but with G-D's help when I have made a prediction I so far have a pretty good track record.

I am calling it now: over the next seven years, the average stock will very likely do better than the Nasdaq 100.