There have been lots of rumblings about potential fraudulent practices in their partnership with Coreweave and other datacenter builders. They issue huge amounts of debt to these datacenter buildrs, and they all put in orders for NVDA gpus that NVDA reports as revenue. These datacenter builders use GPUs as collateral on the debt. There's hedge funds like Magnetar Capital, who were neck deep in the CDO issuances in 2008, involved and getting their beak wet in these deals too. To me this sounds like the kind of thing that works as long as there is unlimited demand, but as soon as that stops the whole house of cards could fall and semis have historically always cyclical in nature.

Personally, I would be bearish on the thesis that the most well capitalized and staffed companies in the world like Meta/Google/Microsoft are going to be fine with paying tens of billions of dollars every year to their largest vendor (and biggest bottleneck) without finding their own workarounds and internal solutions. I know Google in parituclar is pretty far along in implementing their own specialized chips for LLMs and internal uses

Yes, I also think it was the burning capital of private market investors, who are consistently accustomed to very low returns on capital aka value destruction, that injected money into NVIDIA to keep it from being too phony on its cash flow statements.

Edit:

Also, I think this kind of cash injection benefits the financial statements of other public-listed companies especially MSFT, GOOG and AMZN.

The "CUDA is the moat" argument is kind of funny to me, because the AI Maximalists will say that AI is so revolutionary because it completely democratizes knowledge and puts all the established powers in the crosshairs and any average person can just log into an LLM and start pumping out workable code witha few prompts... EXCEPT for AI engineers, who will only learn or use this one specific piece of established software and there can be no other viable imitators or disruptors. I dunno, sounds like motivated reasoning to me that AI is going to be a revolutionary and disruptive technology for everyone else, but not for my sacred cows.

"AI will disrupt everything, creating AGI or even ASI so immensely powerful that one has to even worry about it destroying the human race, so that people will enjoy UBI without doing any job, thanks to our AI gods Altman and Jensen"

"So that would disrupt Microsoft, Nvidia, Tesla, Meta, Google, Apple and Amazon as well, right? Right?"

"No, not like that"

The NVIDIA graphics card I'm using doesn't support CUDA, but that didn't very much bother me in my machine learning attempts.

I think people just haven't tried machine learning on their own, or their graphics cards are so good that they all support CUDA. Or more likely, wishful thinking and blind trust are at work.

We are on the same page. If this is truly going to be a disruptive technology, the last place you want to be is in the established players with existing cashcow business models that are begging to be dirsupted.

It's kind of amazing to me the things people claim AI bots and script writers will be able to do in the next 5-7, but somehow they won't let you to easily move your data out of your cloud walled garden mega public-provider, administer it on a private cloud and get around the current lock-in of AWS and Azure.

Wall Street loves to sell a story. What better story than there is this new revolutionary disruptive technology that could potentially bring unlimited growth and the only thing that is required of you as an investor is just double down on all the current proven Mag 7 companies that you already hold and trust. Talk about a free lunch !!!

I also have a bit of speculation that I think the amount of overseas cash many companies have is suspect.

Since people are now relying on cash flow to detect accounting fraud, I think some smart people have come up with some ways to fake cash balances to keep company financial reports healthy. And one interesting way to falsify them revealed in shorting reports is to falsify overseas cash balances in the name of "not paying such a lot of taxes", as in the case of Wirecard.

And

December 2019 The FT reports that Wirecard appears to have counted cash held in escrow accounts managed by trustees within the cash balances declared on its financial statements.

And

KPMG also queries €1bn of cash balances, on the basis that the only evidence for the sum were documents provided by a Singapore trustee that cut ties with Wirecard around the time the special audit began.

The unfairness felt by Germans on Wirecard might be "why is it that only you Americans are allowed to fake things and not us?"

But I think they are wrong (if they really think so), and that the Chinese and Africans also enjoy equal opportunities for financial fakery on the NASDAQ!!! Regardless of their race, every person has the freedom and opportunity to succeed and attain a better life ... via securities fraud. I think it must represent the American dream. /s

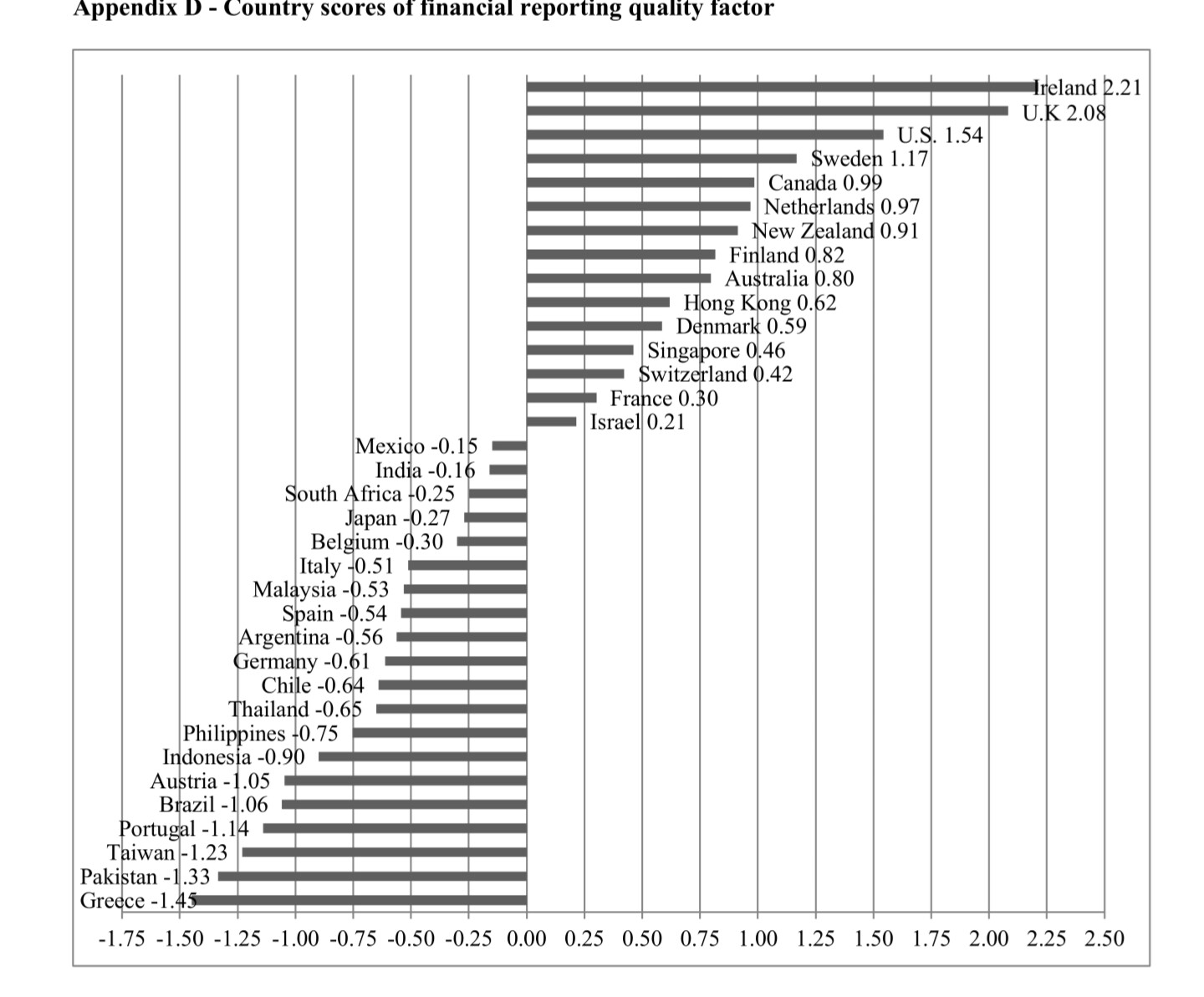

Considering that the U.S. market is already at the top of the accounting credibility rankings of markets around the world, accounting fraud in other markets is even more alarming.

The interesting part is that Taiwan is nearly the worst in accounting quality. And the founders of SMCI and NVDA are both from Taiwan. It must just be a coincidence!!! Right? Right??!! /s

One of these, I believe, is APLD. They're ranked #1 on my list of stocks to buy puts on. They recently raised $160M from a Nvidia private placement, which made their stock go up over $6: a perfect opportunity for me to buy some $4 and $4.50 puts because the price of those puts went way down. This is a company with negative gross margins, huge net losses, depleted cash reserves, asset sales, equipment issues, and questions about the true demand for their services. This quarter's interest expense: $18M, revenue: $46M, operating income: -$34M. Net loss: -$65M. This is obviously unsustainable, so they just issued $53M in convertible preferreds, convertible at $7, so that places a pretty firm cap on the stock price there. Then they're going to issue 49M more shares at $3.24. The current price is about 6X tangible book value. This is a company that used to be called Applied Blockchain and only switched from Bitcoin mining to HPC two years ago. I'm not sure whether APLD uses only Nvidia GPUs, but I suspect it does. And then there's all this: https://www.wolfpackresearch.com/items/apld%3A-an-embarrassing-and-predictable-stock-promotion and this: Problems at Applied Digital (APLD) - by Edwin Dorsey . . .

If this is typical of the kind of investments Nvidia is making, that doesn't speak well of them. If they're so successful at selling GPUs, why are they trying to shore up customers like these?

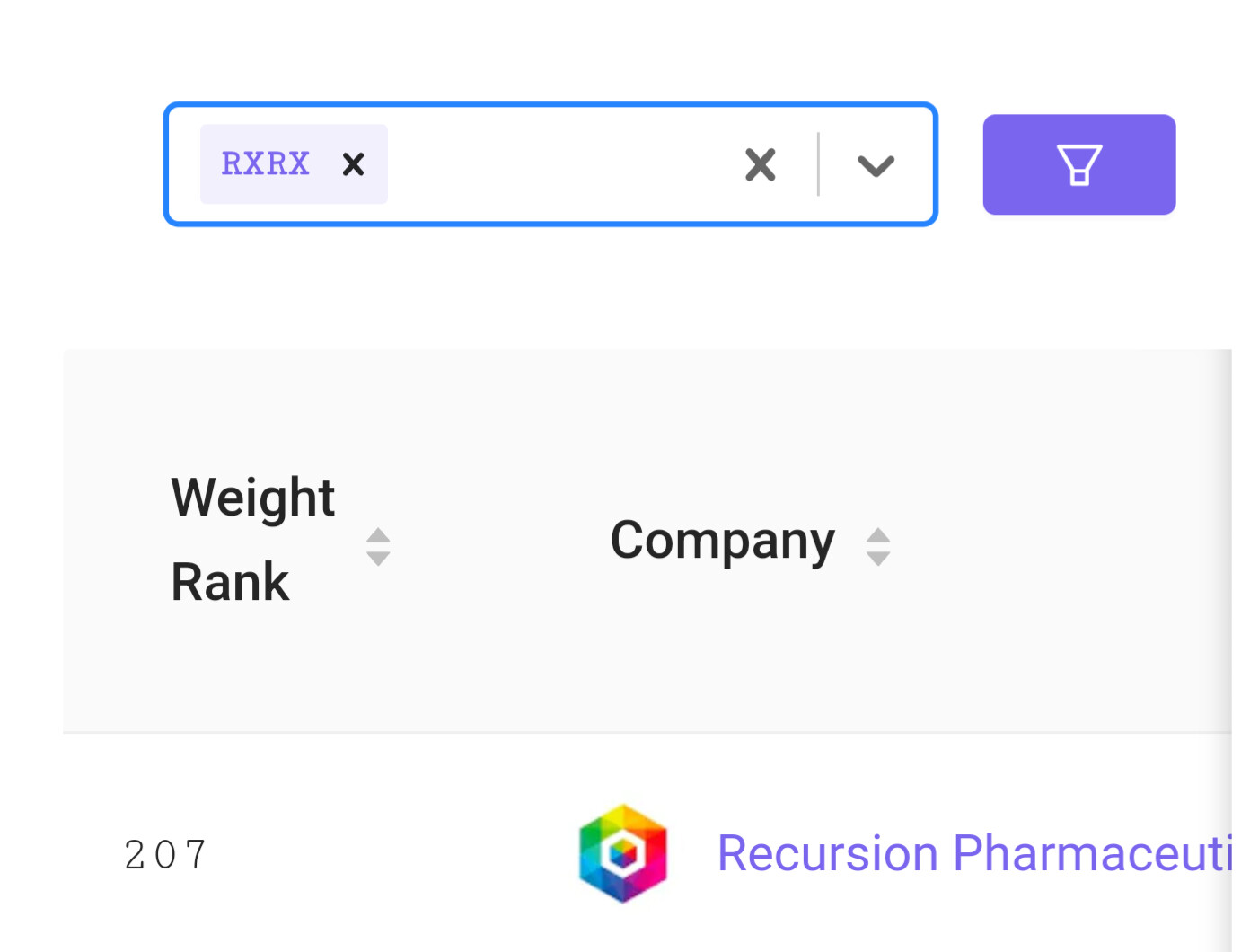

In a 13F filing earlier this year, Nvidia disclosed its investments in five companies as of Dec. 31, 2023: SoundHound AI (NASDAQ: SOUN), Arm Holdings (NASDAQ: ARM), Recursion Pharmaceuticals (NASDAQ: RXRX), Nano-X Imaging (NASDAQ: NNOX), and TuSimple Holdings

Four of them are losing money and the other one aka ARM has a PE ratio of 300+. The most shocking one is TuSimple Holdings because it is a stock listed in OTC and even has a "Delinquent SEC Reporting" status.

I think NVIDIA deserves a better partner than such a totally failed traditional China Hustle with a lot of fake overseas cash because Nvidia is a grossly undervalued super quality ultra growth deep value chad sigma AI AGI ASI company, right? Right? /s

"Even though five of the seven US-listed companies NVIDIA invests in have short-selling reports, that in no way means there's anything wrong with NVIDIA, right? Right?" /s

"When you're deemed less worthy to buy than the meme stonk king GME by the Core Combination system..."

GME

Maybe Uncle Jensen should compete with Aunt Cathie for the winner of the contest about buying the most value destroying stonks and fabricating daydreaming numbers & absurd narratives to deceive investors...

Oh no, Cathie acutally HAD bought one of those stonks too!!!

If this is typical of the kind of investments Nvidia is making, that doesn't speak well of them. If they're so successful at selling GPUs, why are they trying to shore up customers like these?

"This must be because Jensen is charitably helping these struggling companies, not because they are all used to financial fraud and stock fraud like SMCI and NVDA. "/s

This was the first article I read that turned my attention to some of the concerns, and I've seen other since. I don't think they're doing anything illegal, per se. And I would never short such a high flyer. I just think some of this is sketchy accounting practices, and high risk of impairment losses, for one of the highest market cap and well known companies in the world.

I think it's far more than just being illegal. There are basically no companies that don't always cook their books (very) illegally. For example, I said many large/mega US-listed companies may falsify their cash flow figures in the name of overseas cash and stabilize & inflate their FCF yields. My suspicion is that there are extremely serious falsifications and misstatements about NVDA so I said it may be a scam.

For example, there may be fraudulent round-tripping "sales" like SenseTime (a typical China Hustle) and NVDA is only backed by borrowed cash from private market investors to keep their shit from showing up on the cash flow statement.

provides funds to customers that in turn are used to purchase goods from SenseTime that might never have been delivered.

And

Our research uncovered numerous potential undisclosed related parties with SenseTime. Many instances were majority-owned by senior-titled officers of SenseTime or related to one another through publicly available sources. SenseTime’s conscious choice to keep these entities off the balance sheet is deeply worrying, especially in light of the revenue round-tripping described above.

I suspect that what appears to be free cash flow of NVDA is actually financing cash flow of its affiliated entities (such as CoreWeave but much more), backed up by money from private debt funds that have been booming lately.

I think as in Microsoft's relationship with OpenAI there may be this same problem, i.e., because of the importance western investors place on free cash flow, many US-listed/Europe-listed companies use a similar approach to falsify their own free cash flows from financing cash flows from related parties (and much of the cash is from private market so it inflates the FCF yield of the public market), but NVDA may have taken this to the extreme.

Great article. This entire discussion has been truly eye-opening.

And thanks to ZGWZ for the info on the Nvidia-backed companies. It stands to reason that several of them are companies I'm actively betting against with put options.

I've even seen many people (apes or shills) at WSB advocating that NVIDIA wisely invests in promising AI companies with their GPUs and therefore NVIDIA has a very promising future. This is wonderfully ironic considering how rubbish the public companies it invests in are.

"Lower tax rates abroad" may mean non-existent cash income, non-existent tax payments and non-existent cash balances. Instead, share buybacks may be mostly backed by debt financing from affiliated entities including CoreWeave.

The worse part is not CoreWeave itself. It is about the AI Infrastructure Server Solutions For Enterprise.

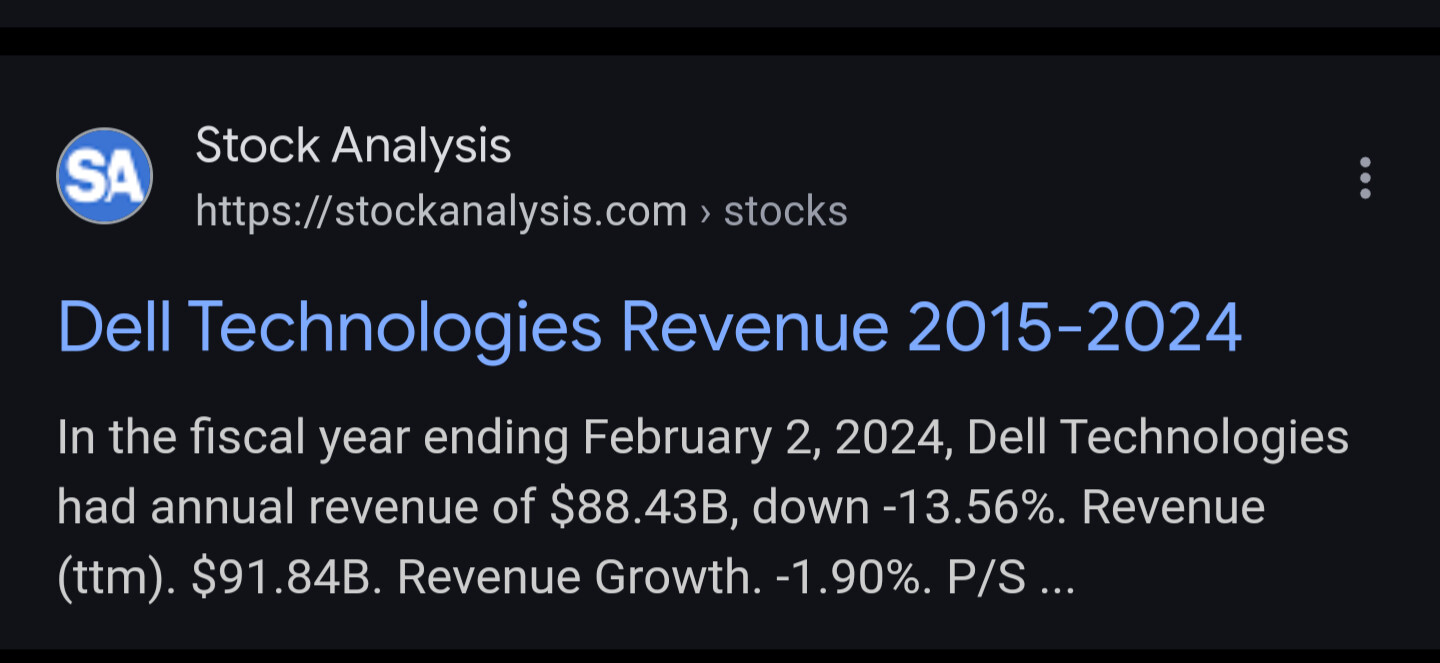

In fact, despite Jensen's praise, Dell, a strong competitor to SMCI n the server solution industry, had negative TTM sales growth, as has HPE, which offers similar solutions.

"It seems that AI has become so powerful that they can even assemble themselves to form their own servers without the incompetent Dell, HP and SMCI, and we are one big step closer to ASI and everyone enjoying UBI without having to work!" /s

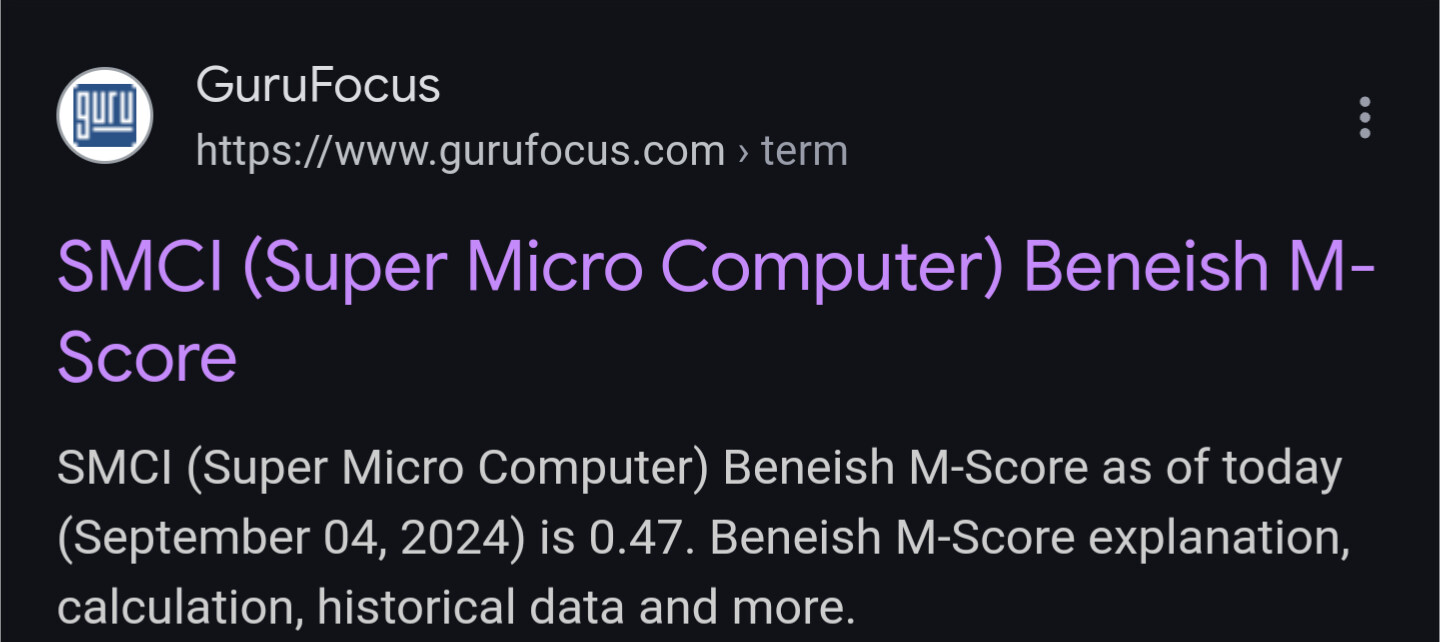

Coupled with the fact that SMCI is suspected by short sellers of fakery and has an M-score even higher than 0, a plausible explanation is that since the "AI data centre investment mania" doesn't actually exist, so does the sales mania for AI server solutions if we don't include SMCI's cooked books.

Background: $80 Billion Global Data Center REIT With 260 Facilities Globally

Despite growth CapEx at all-time highs, billed cabinet growth slowed to 1.7% in 2023.

Equinix is another red flag because its real sales growth was only 1%+ in 2023. Even if the biggest users tend to build AI data centres on their own. The smaller players still need data centre providers like Equinix for their AI servers. The tiny real sales growth of Equinix means the general AI mania narrative may be a scam at all.

The worse part is Equinix's competitors have even worse sales. For example, Lumen is exposed by many short-sellers and has a two-digit negative sales growth.

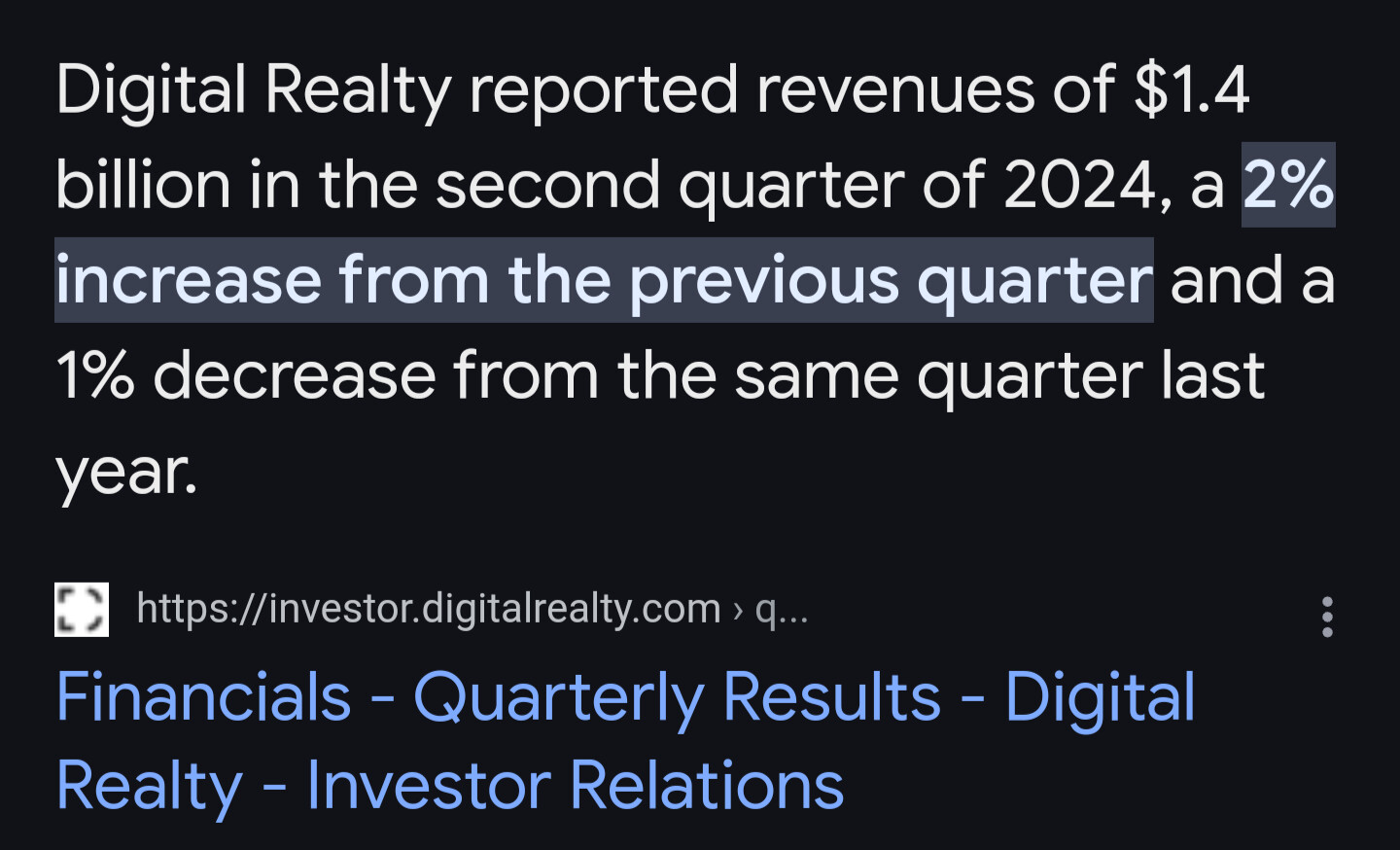

Digital Realty is just not so bad but still has a negative growth.

So if the so-called "AI investment mania" does exist, why would data center industry enjoy such a minus sales growth as a whole?

Of course, I'm sure AI and our tech god aka Wonder Uncle Jensen's accelerator cards have evolved to the point where they don't need any real places to store at all, right? Right? /s

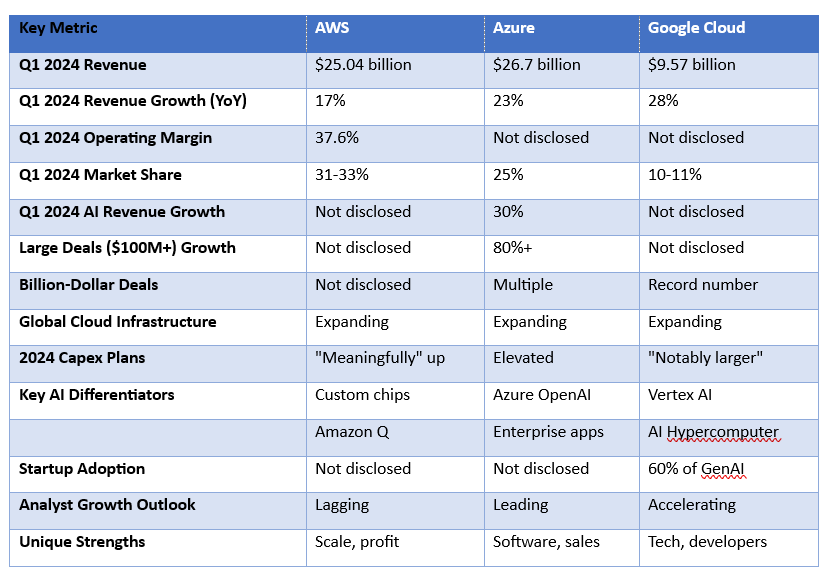

Regarding cloud services, the three cloud service giants didn't do so well in terms of revenue growth either.

Azure, the only one to have posted AI-related cloud service revenue growth, didn't grow much higher than its overall growth in AI-related cloud services (23% vs 30%). This doesn't support the narrative that the big three cloud service providers are rapidly investing in AI infrastructure to serve surging demand.

The problem isn't whether there is a real gold mine, as many say, or even the absurdity of thinking that "NVIDIA is a good company, but the stock price is a bit high and will need to be pulled back later", but rather the fact that there isn't even a real gold rush going on, or maybe the real gold rush is the stonks we pump and dump along the way /s

While all the companies up and down the chain of the alleged AI investment mania are enjoying negative, single-digit or at best slightly over 10% TTM sales growth, only NVDA and its friend SMCI, also from Taiwan, are enjoying staggering triple-digit growth rates, and the latter has had its financial reporting delayed and its share price plummeted by short-sellers on suspicion of fakery. But NVDA's nearly 200% TTM sales growth must be real. /s

If Nvidia reverts to its 2022 earnings of 0.17 per share, coupled with a valuation of about 10x-20x due to a lack of real growth prospects and involved in scam like PDD & BABA, it could fall to much less than $5, assuming it doesn't fall into the red under the pressure of bagholders' lawsuits.

I think the AI narrative is basically just a rebranding of the COVID-era "growth" hype linked to infamous figures like Aunt Wood, in order to revive the stock prices of semiconductor- and cloud-related "high-growth" story-tellers and unprofitable crapw in 2022 after the bubble slightly bursts. And other stakeholders have led, participated or acquiesced in these speculations for their own interests.

For example, the "Mag7" wants to boost its share price, regulators want a soft landing along with interest rate hikes, billionaires want people to be content with investing in tax-free savings accounts without having to rely on taxes on the rich to pay for their pension shortfalls, financial institutions want more trading volume in the stock market, private equity and hedge funds want to have more more assets under management, and quantitative traders want more stupid money. Concerns about this unprecedentedly ridiculous bubble may be exactly why Warren Buffett chose to sell off some of his largest holdings, despite attempts by the financial media to assuage the associated fears on a variety of now seemingly untenable grounds.

However, this doesn't mean anything new, it just means that people need to rely more on factor premiums than equity premiums at the moment, but this has held true since the rate hike.

The US leagues of stock exchanges are the most pumped and dumped in the world, after all in a system of growth based upon the flow of capital, the pressure for positive qtr numbers is intense and most if not all do whatever it takes to keep that growth momentum.

without what some term creative accounting your portfolios would hardly grow even long term with compounding,

The US has actually been one of the best, with the quality of its accounting second only to the UK and Ireland. Internationally, Aramco's financial statements are just incredible in the extreme, and LVMH, NOVO-B and ASML are also very bad.

However, I do think the UK has a very good stock market at the moment and I am currently heavily invested in UK equities.

The emergence of DeepSeek means that if its allegedly extremely low training costs are true, then the number of hardware purchases claimed by large tech companies is likely to be extremely bogus, and is simply being used to hide losses/inflate profits and hype Nvidia's stock and their stocks.

My point here is that the big tech companies are very likely to dominate the hype this time around. And I think the stock market is centered not on growth, but on profit-making

In fact, it's almost impossible to spot Coca-Cola ahead of time, which relies heavily on luck, as Buffett himself has long admitted. Machine learning algorithms with 5+ or even 10 year horizons are almost exclusively low value ratios + low volatility + high gross margins and poorly predictive. As a result, you can't just "buy Coca-Cola" and "long-term" is always too long to maximize reward-risk ratios.

There is also no intrinsic value: it's just a convenient construct that fits people's needs, but very unsuitable for talking seriously about stock selection. In fact the best we can do is to rely on relative valuations (that is, relative rankings within the industry on the value factor) to make predictions about future relative returns. I agree with the rest of your formulation though.