I've never cared much for NVIDIA because it's a mega-cap stock and completely out of my league.

But I recently read an article claiming that NVIDIA is a scam. I thought "how is this possible". After all, Enron and Wirecard were not among the largest companies in the world. I can't imagine even one of the world's largest companies being a scam.

However, I did do a research. One of the centrepieces of the NVIDIA narrative is that AI demand drove demand for graphics cards, allowing them to grow sales and profits extremely quickly without a significant increase in the number of cards they made. I've also heard that China is figuring out how to import graphics cards and that US officials are restricting NVIDIA's graphics card exports. smci has even been questioned about evading sanctions because of this.

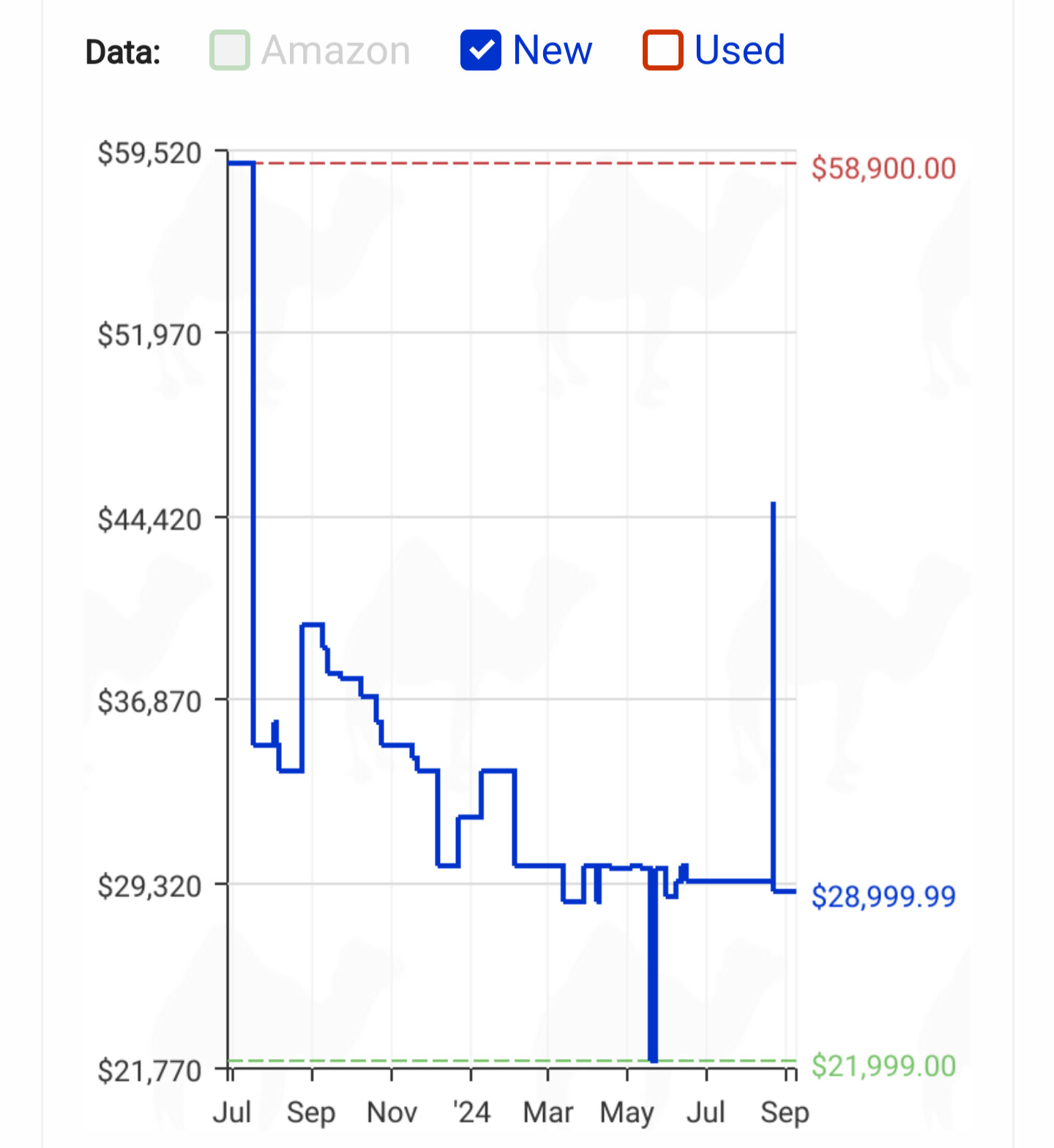

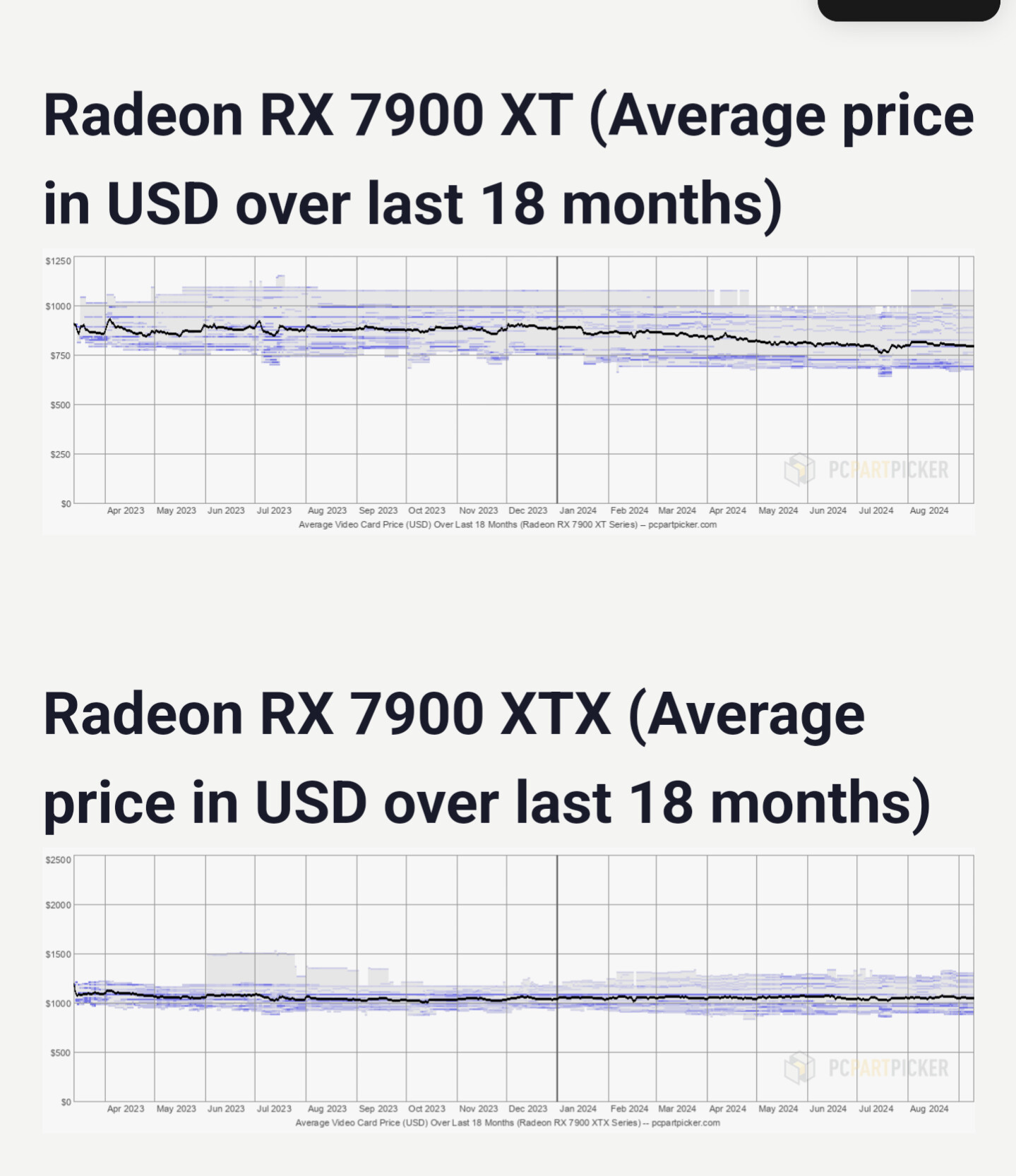

So I expect graphics card prices to rise similarly to what they did in 2020. However, I was surprised to find that the price of Series 4 graphics cards, which are known as ones of the best NVIDIA graphics cards for training AI, not only didn't go up in the last 18 months, but instead went down by about 20 per cent. OK, this is not what you would expect an AI frenzy to look like.

Of course, it's not as if the NVIDIA narrative doesn't take this into account. Its saying that they're shifting capacity to AI-specific compute cards (not graphics cards) with much higher margins. However, given that Ethernet's shift to PoS in October 2022 increased the supply of graphics cards at the start of the charts (early 2023), this further reduction in supply should result in a significant increase in current graphics card prices compared to early 2023, not a decrease. Not to mention, the purportedly extremely high pricing of its AI-specific compute cards should lead to increased demand for gaming graphics cards that 1 can partially replace their functions, further leading to an increase in their prices.

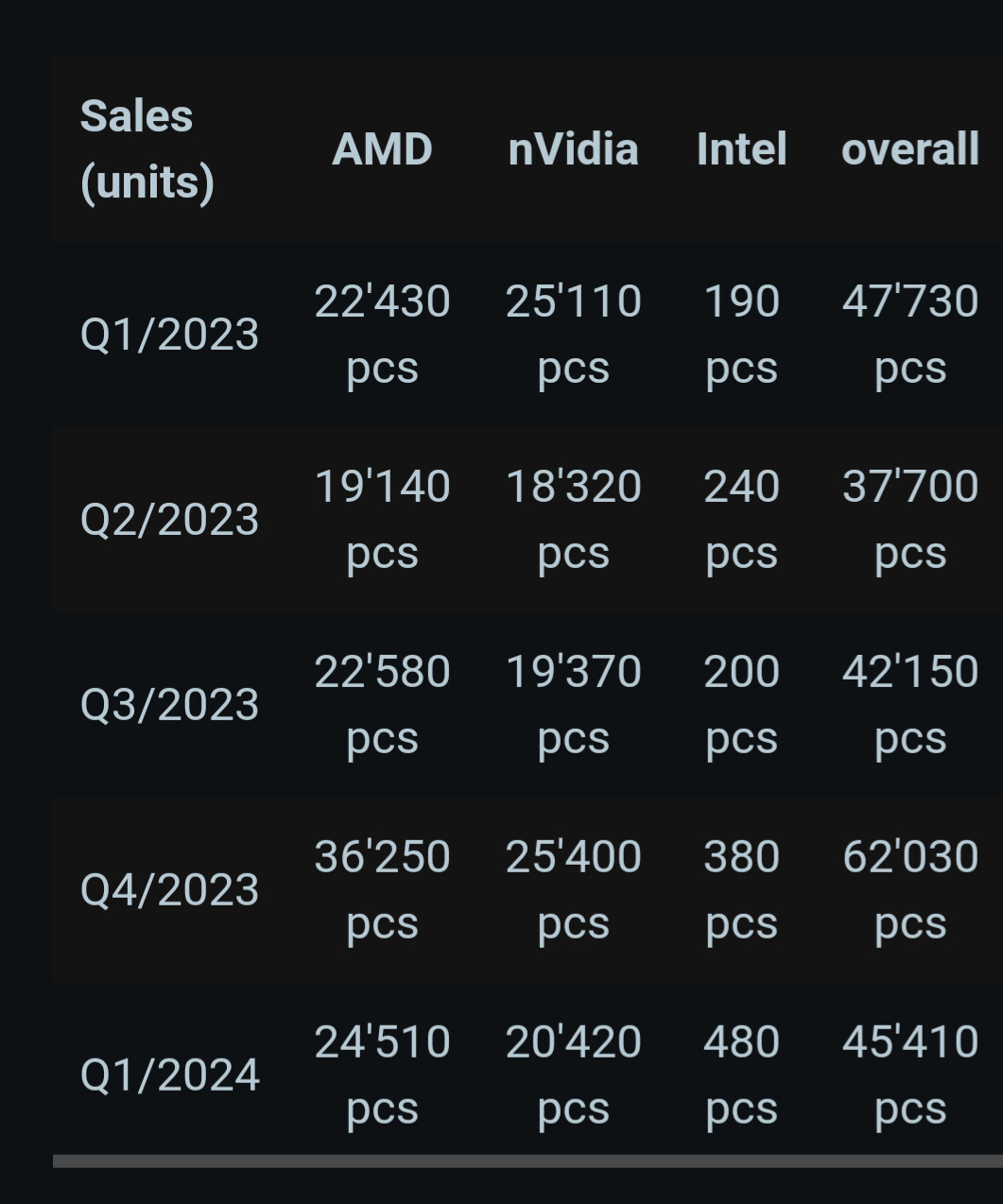

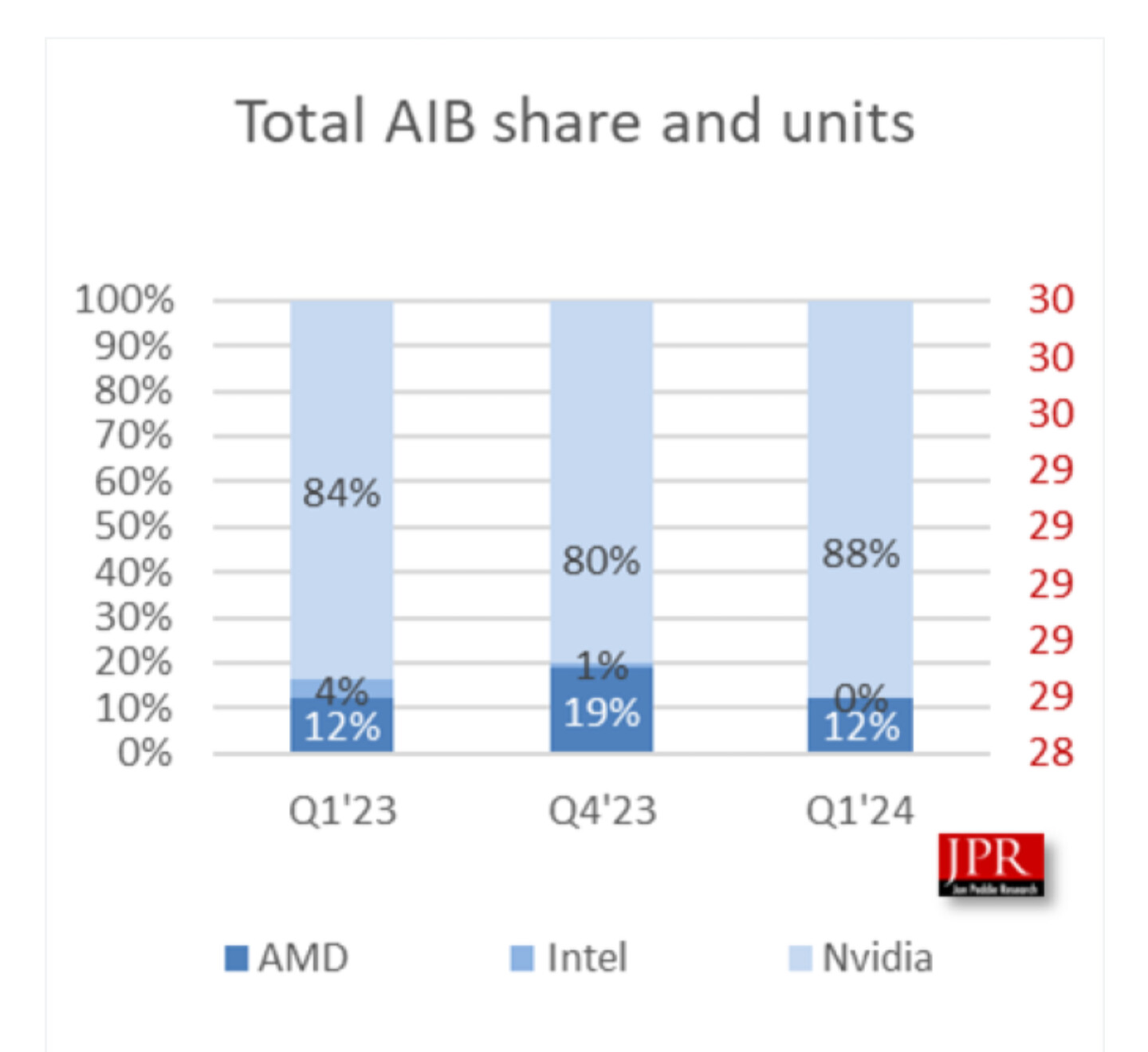

And oddly enough, AMD's graphics cards actually had less of a price drop than NVIDIA's. But their TTM sales revenue growth is only in single digits. And SMCI, which was recently shorted by Hindenburg, had "only" 100% sales growth after possible accounting fraud, so how could NVIDIA have 200% sales growth? The numbers don't add up.

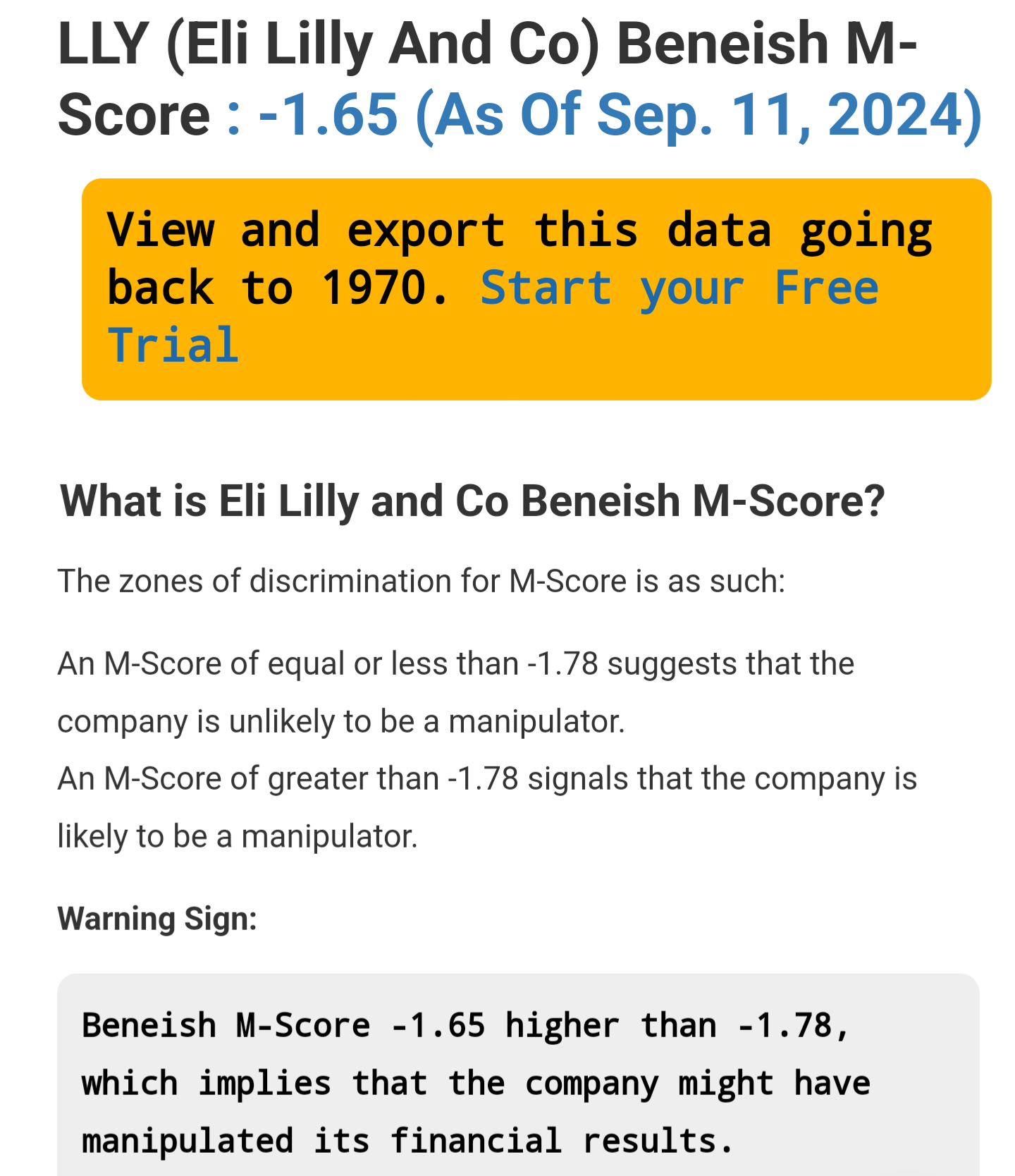

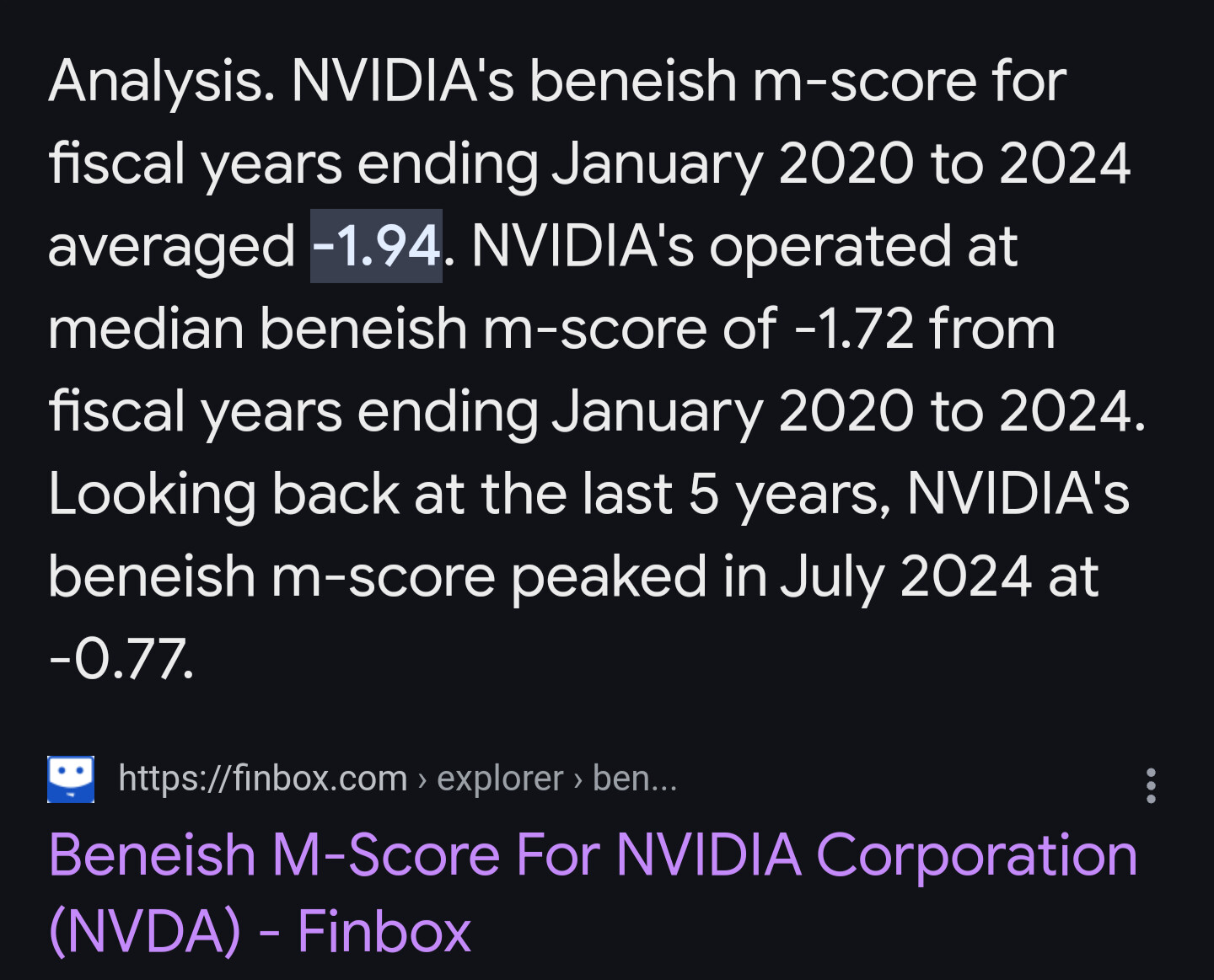

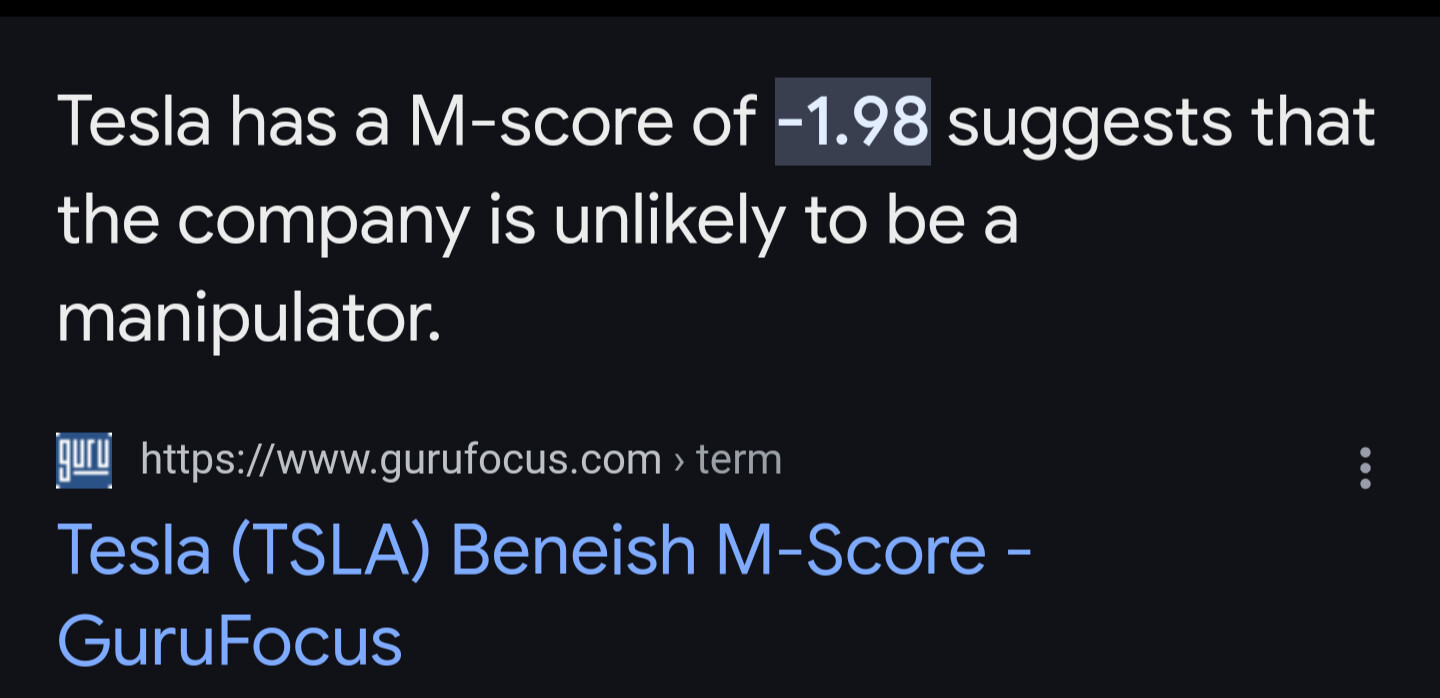

What's even stranger is that despite a great graphics card price increase in 2020 due to miner demand as a result of the ethereum price spike, NVIDIA didn't get a sales increase and even by 2021, when the supply chain issues have eased, only had less than 50% sales growth compared to 2019, which accompanied more than 100% CoGS growth. So how is it possible that sales growth of nearly 200% with only less than 100% CoGS growth is now possible without graphics card prices skyrocketing, but instead only graphics card prices dropping? Also, the m-score is very high for NVDA:

If one's book is considered more fake than Tesla's, then you need to be careful.

Of course, I have not and am not prepared to short NVIDIA at all, nor am I encouraging anyone to short it. Even given its factor rankings, I think those who are long it are making a good choice among large-cap stocks. But I just find it amazing that this is so patently ridiculous and yet hardly anyone sees it.

Edit:

The article to make me do the research.

I thought it's just another claptrap doom-monger trying to con viewers to get advertising revenue through baseless nonsense without any basis in fact. But now I'm not so sure.