In the financial press today is an article from James O’Shaugnessy and what he describes as the best quant formula for the past 50 years.

In a nutshell

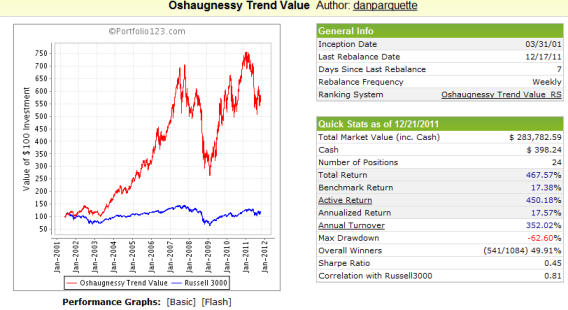

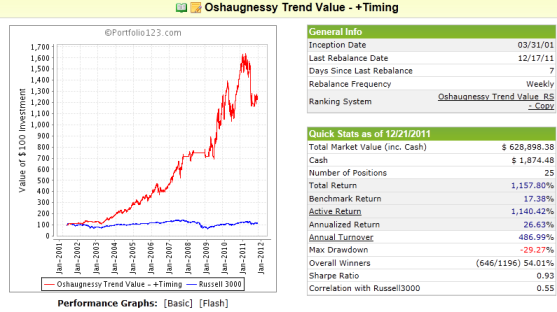

Trend Value strategy

• Price-to-Sales

• Price-to-Earnings

• Price-to-Book

• Price-to-Cash Flow

• EBITDA/Enterprise Value

• Shareholder yield (dividend yield + rate of share repurchases)

Each stock in the universe gets a score of 1 to 100 for each of these factors. The final value score is an average of these scores. The Trending Value portfolio narrows the investable universe to the 10% of stocks with the best score based on the value composite, and then selects a concentrated portfolio of 25 stocks based on trailing six-month momentum.

This simple combination builds a portfolio of extremely cheap stocks that are on the mend. The combination of value and momentum works better than either of these factors on its own.

Examples of stocks currently passing this strategy are Advance America Cash Advance Centers Inc. AEA -1.15% , Tesoro Corp. TSO -3.98% , and Smithfield Foods Inc. SFD +3.15% .

Of course, we certainly expect there to be stocks in our strategies that underperform, and these three stocks may not perform well in the coming year. But we also know that a diversified portfolio of stocks with the characteristics these stocks currently posses has fared extremely well over time. By focusing on the long term, and taking advantage of market volatility rather than being scared off by it, investors can beat the market in the long term and achieve their investing goals.

James O’Shaughnessy is Chairman and CEO of O’Shaughnessy Asset Management, and author of “What Works on Wall Street.” Patrick O’Shaughnessy is a Research Analyst at O’Shaughnessy Asset Management.