Yuval,

I will check that out but I already like your sim. Even though it is lower liquidity it has over 20 stocks. And as you illustrated one could buy in over at least 2 days (until Wednesday at a minimum) and probably much longer. Not to mention long holding period.

Your system is interesting, thanks for sharing. I backtested it on Russell 3000 and indeed it works well for 2011 to 2016. However, when running it for the last three years, it’s not that clear.

Also, when looking at your universe, I see “opincq > opincpyq” and I’m not sure if this is value. It looks to me as a growth scan. e.g. a lot of good value stocks have temporary declining operating income. Same thing for “si%shsout < 3”. Many good value stocks are shorted a lot. I wonder how those characteristics are related to value investing.

Another question: In your formula (opercashflttm-capexttm+0.87*intexpttm)/ev what is the 0.87 for?

Last point: I backtested your system from 1999 and there is a monstruous -75% decline in 2008. Maybe it’s OK, maybe it’s not, but I’d have to have complete confidence in a system to deal with such a decline.

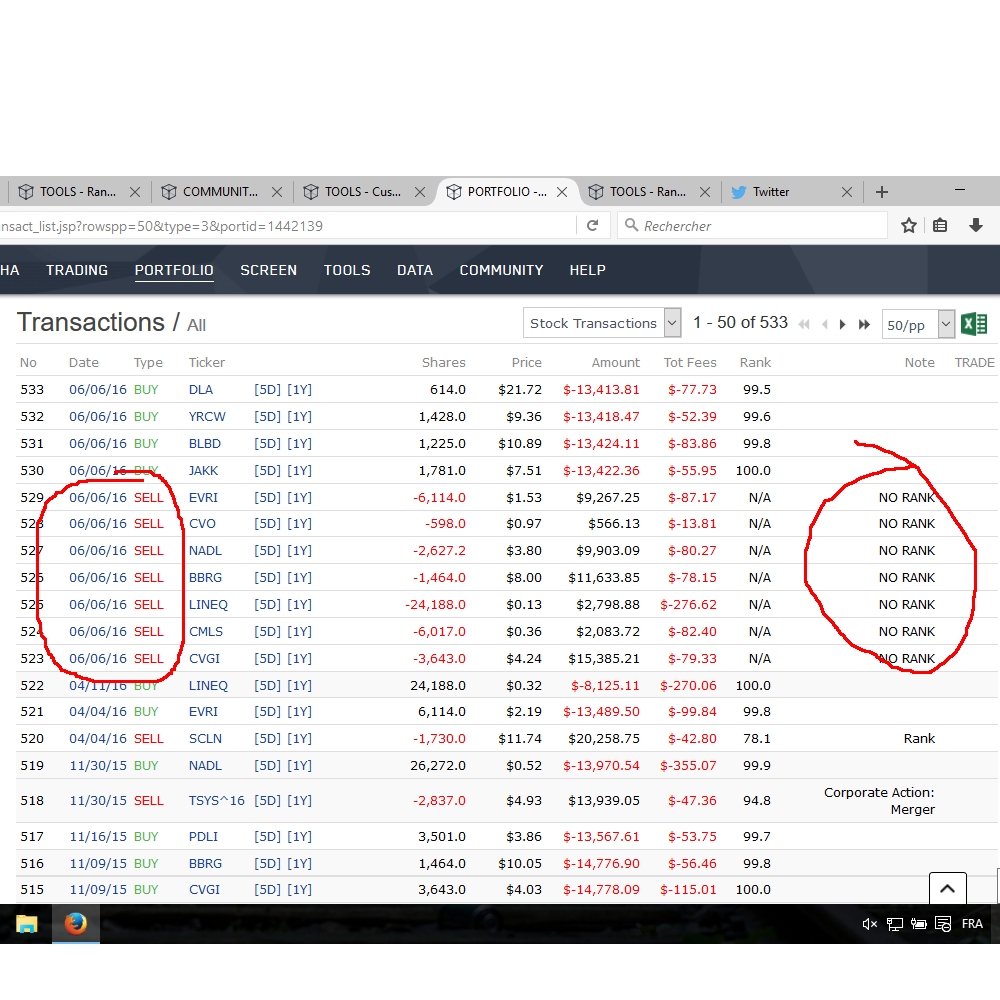

A very last question/observation. When backtesting, I found that a lot of stocks sold on the same days, and the reason was “NO RANK”. I am wondering why it’s that way (what is wrong in your rules to create this or if it’s not wrong… why did you make it this way?!) and also if this could cause some kind of curve-fitting?

When you say that if one could add quality rules… well it seems to me there are already a lot of rules, so how to avoid curve-fitting with so many rules already?

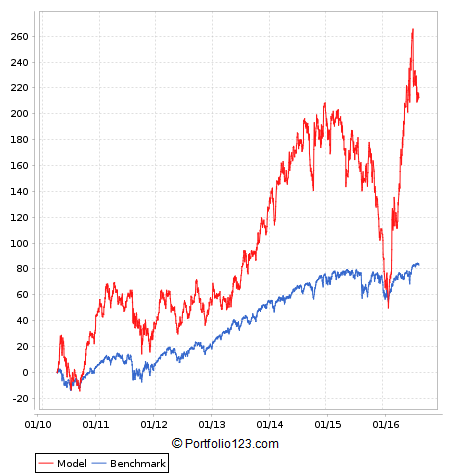

First, this isn’t a system I myself use. I put it together in about half an hour. So I’m not an advocate of it. The system I use does about three times as well as this. I just wanted to show that value could still easily work in the last six years. If I worked harder at this system, I’m sure I could have improved it a lot.

I don’t think any value investor looks ONLY at value when choosing a stock. You have to look at some other things too. Since I myself am more of a growth-and-quality investor than a value investor, I chose two things that I look for–earnings growth, low short interest. But I’m sure other things will work instead of those, and you make very good points about that. I don’t think I could create a sim that worked on value ALONE. There are just too many stocks that are cheap because they deserve to be cheap, and will never rise much in value.

A lot of stocks declined in 2008, and I don’t think you could have been fully invested and gotten away with a decline of less than 40% or 50%. At least a value strategy would have given you a fabulous 2009.

I believe that the NO RANK thing probably means that the stock was no longer in the universe. Maybe the short interest went way up.

Maybe I don’t understand something, but you showed your system (which is very good and congratulations if you did it in half an hour!) saying that value investing still works but a big part of your system is about growth, with rules against short interest, against a decline in operating income, etc. So wouldn’t that make it a GARP system or an hybrid-system rather than a value model? This is not trivial: if major components of the system are about growth, then the fact that the system works doesn’t mean that value investing still work.

As for the NO RANK, do you see the same thing when backtesting it? Is it normal that like 7 stocks sell all on same day because of no rank?

And about further working on the model… Don’t you fear it would become curve-fitting?

Last thing: what about bid-ask spread with lower market cap stocks?

I think O’Shaughnessy–or ANY value investor, for that matter–would say that value can’t be the ONLY thing you look at when you’re deciding what stocks to buy. Now, value investing is based on DCFS theory, which holds that a company’s value equals its net present assets plus its discounted future cash flows. Discounted future cash flows are very hard to measure, but they’re predicated on having not just strong revenue, strong earnings, and strong cash flow–which is what those price-to-whatever ratios are about–but INCREASING cash flow, which is dependent on increasing earnings, which is usually dependent on increasing revenue. In other words, DCFS falls apart if you don’t take growth into account at least in some measure. If an investor thinks that a company’s future cash flows are going to decrease, that company’s intrinsic value is significantly lower. But as I said, you could eliminate the growth factors and substitute in some quality factors–say, for instance, stable operating margins, low accruals, high return on capital–and you’d still have a system that worked pretty well. I personally would never invest in a company that did not have a good price-to-sales ratio in comparison with the rest of the industry, and that’s the real takeaway from What Works on Wall Street.

I’ve never seen the NO RANK thing before and am pretty mystified by it.

To eliminate curve-fitting I subject my models to iterations using different numbers of stocks, different sell rules, different universes, etc. Then I average everything.

I don’t often run into big bid-ask spreads as long as I keep my price above $1, my float above 5 million, and my ADT above $50,000, and as long as I only use limit orders. I never use market orders. I do get partial fills, and sometimes I have to replace my orders three or four times, and sometimes it takes a few days for me to fill my order, but my overall slippage–and I buy almost exclusively microcaps–is only about 0.6% per trade.

Your Sim may not have “Force Positions into Universe” like Yuval’s Sim does. His Sim does not sell any stocks due to No Rank.

A stock is sold when it no longer meets all the Universe rules. The Universe has many rules that can cause a stock to be sold due to “No Rank”:

avgdailytot(90)>=50000; If on rebalance, a stock’s value is $49,999 or below it will be sold.

curqepsmean > epsexclxor(3,qtr); If a stock’s curqepsmean falls slightly below epsexclxor(3,qtr), it will be sold.

opincq > opincpyq; If a stock’s opincq falls slightly below opincpyq, it will be sold.

si%shsout < 3; If a stock’s si%shsout becomes slightly greater than 3 it will be sold.

I don’t think that you intended this behavior to occur. To avoid that move these rules to the buy rules, or set “Force Positions into Universe” to yes.

Problem with setting “Force Positions into Universe” is that his selling rule is rank < 80 so if I do that those stocks will never ever sale! I don’t know how to deal with this problem and don’t know why I get such a bunch of NO RANK all at the same time.

I see things differently concerning the DCF model. It doesn’t need to have growth at all. In fact, right now I am invested in a company with decreasing cash flow, decreasing operating income, decreasing sales, etc. But running a DCF shows that the market overestimates the decline and since I consider that the decline is temporary, things will get better eventually.

Setting a rule that says that the operating income must grow “now” is not something that need to happen in a DCF model. Many of the stocks that are bought by value investor are beaten-down stocks, with temporarily setbacks, temporary decline in operating income, etc.

So my point is that if you set your universe to include only stocks that are growing they operating income and that have low-short interest, you restrict yourself mostly to growth stock. Then, you try to find the growth stocks that offer the best value, and this is an original idea, and I believe this is why it seems to work.

However, I wouldn’t say that it proves value investing is still working fine. On the opposite, it shows that growth investing is working fine as well.

I believe your universe is down to 500-550 stocks. Isn’t that a little low to get a good sampling? And did you think about other sell rules than “rank <80” to get over the NO RANK problem?

OK, I redid my sim. I eliminated the growth and short interest rules. Then I ran it with the top 10 stocks instead of the top 25, and changed the sell rule to rankpos > 40. That means you’re only holding the absolute CHEAPEST stocks out there, regardless of growth or short interest. DIRT cheap.

The result was still pretty good, but with a truly terrible drop in 2015.

What about the “curqepsmean > epsexclxor(3,qtr)” rule?

I tested your rules on a little system I built (nothing great… I wish I could build neat systems like you do) and the 3 “growth” rules are underperforming before 2010 and outperforming after 2010. Said differently: if I don’t put those rules, I get better results since 1999 and if I put those rules I get better results since 2010.

So maybe it’s not value that’s doing fine since 2010, but rather growth!

It’s kind of difficult at this point to decide if it’s worth adding or not. I feel like it’s simply curve-fitting, trying to decide if it’s better to fit the 1999-2016 curve or the 2010-2016 curve. A simple EBITDATTM/EV strategy worked like crazy since 1999, but not so much anymore.

I wonder what would be best: enginering since 1999 or considering data older than 10 years mostly irrelevant because people have better access to quant models like P123.

It’s about mean reversing and if something changed in the market. The author says, amongst other things, that value investing comes from mean reversing and that mean reversing was a prominent feature of the 20th century, but it doesn’t mean it will continue to be as important as it was.

Just a few thoughts on your last two posts. I myself tend to follow T. Rowe Price’s idea: companies are either growing, mature, or declining, and one should invest in those that are growing. But I always want to buy them cheaply and, most importantly, I want to only buy companies of high quality. That’s my strategy in a nutshell. So I don’t look at the market in terms of whether value vs growth, or whether one’s winning or one’s losing.

There’s been some discussion on other forums about what time period to use when backtesting. Marc Gerstein believes that the market between 1999 and 2002 (or 2004?) made no sense at all and one shouldn’t look at it. P123’s data prior to 2004 is a bit spotty when it comes to certain things like short interest and sales estimates. Everyone here seems to agree that looking at what worked the last few years more than what worked over the last 100 years will make you more money than looking only at the big picture because of the huge changes in the market that have occurred recently. Market trends can reverse but usually not all of a sudden. I like to look at the last fifteen years as well as the last five, and weigh the last three to five more heavily.

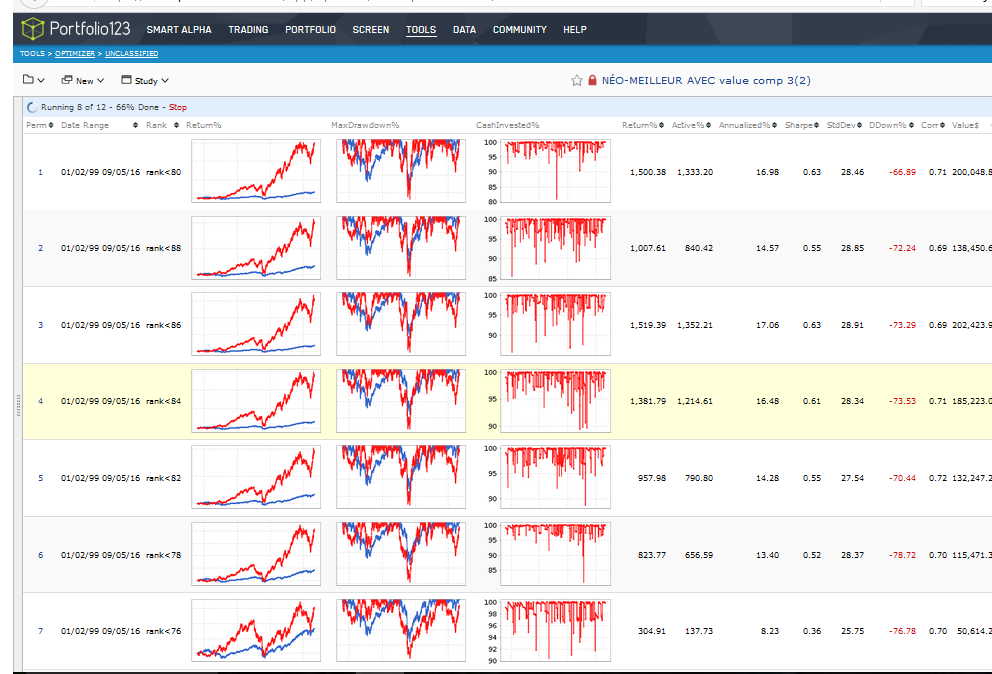

I retested your system and as good as it looks on the screen, I believe there might be some way to make it more resilient, concerning the selling rule per example.

I optimized it with a simulated portfolio and tried with different selling ranks.

As one can see, the results are all over the place. Going from rank 80 to rank 76 nearly kills the system and going from 80 to 82 cuts profits in half.

Here is a very simple system I built. As you can see, the active results aren’t jumping all over the place. That’s what I meant when I said that fewer rules means less chance of over curve-fitting.