Value comp:https://www.portfolio123.com/app/ranking-system/268516

where $NewSYield = Yield + (EqPurchTTM-EqIssuedTTM)/ (SharesPYQ*1000)

Value comp:https://www.portfolio123.com/app/ranking-system/268516

where $NewSYield = Yield + (EqPurchTTM-EqIssuedTTM)/ (SharesPYQ*1000)

Well the shareholder yield equation you’re using is different that what I’ve used, which is:

100*((DivPaid(0,ann)+( EqPurch(0,ann)-EqIssued(0,ann)))/mktcap).

How did you develop your equation?

What’s your 26wk%chg ranking system look like?

Here are all mine:

Trending Value: https://www.portfolio123.com/app/screen/summary/164761?st=0&mt=1

VC2: https://www.portfolio123.com/app/ranking-system/292980

6 Month % Change: https://www.portfolio123.com/app/ranking-system/292122

Is your value comp ranking system set to have N/A neutral?

My formula for ShareholderYield is not correct - I have now changed my formula to be:

$NewSYield = Yield + (EqPurchTTM-EqIssuedTTM)/ MktCap

Now I’m getting 14.40% CAGR for the time period. Are you still getting 17.4%?

I have amended my Shareholder Yield formula to equal your one and I get CAGR = 7.62%.

I have checked your model and the difference is in the Universe. I have created a custom Universe called “All Stocks>200Inf” which starts with the All fundamental -USA universe and applies one rule: MktCap>200*close(0,#CPI)/211.49.

Your screen used the All fundamental -USA universe and then with a rule excludes companies by using this rule: MktCap>=200 * Close(0,#CPI)/210.228

I am surprised that this gives such different results.

O’Shaughnessy calculates his buyback yield on shares outstanding instead of the equity purchased/issued portions of the cash flow statement. Effectively SharesQ/SharesPYQ.

The issue I’d see with using EqPurch and EqIssued is that you don’t know the price at the time of purchase/issuance, you are comparing it to current market cap instead which may or may not be the same as the market cap at the time of the transaction.

mbclark, you are right. I have now changed my formula to be:

Yield + (SharesPYQ-SharesQ)/SharesPYQ

I actually use the universe labelled “No OTC Exchange”. I believe O’Shaughnessy stated that he did not include OTC stocks. This gives me 15.46% CAGR.

In your value comp ranking system, do you have N/A as neutrals?

Interestingly, using this results in worse performance in my trending value screen and my consumer staples screen which ranks by shareholder yield than my old formula of:

100*((DivPaid(0,ann)+( EqPurch(0,ann)-EqIssued(0,ann)))/mktcap)

On his website, O’Shaughnessy lists the equation for buyback yield as:

(100*(1-CM_SHS(#1)/CM_SHS(#1-12)))

link: http://whatworksonwallstreet.com/pdf/wwows_appendix.pdf

I have amended my formula again as it still was not right if I was adding it to Yield. It should be:

Yield + 100*(SharesPYQ-SharesQ)/SharesPYQ

This is the same as:

Yield + 100*(1-SharesQ/SharesPYQ)

Also, I have checked WWoW 4th edition and can’t see that OTC are not included in his All Stocks universe

Using this formula, I have a 12.44% CAGR using the No OTC Exchange universe.

Using Universe = No OTC, I get a CAGR = 12.01%

I have narrowed it down to 2 differences. Our ranking systems are different in two ways:

Caley89 pdw

PEExclXorTTM: lower EPSExclXorTTM/ Close(0): higher

Pr2BookQ: lower BVPSQ/Close(0): higher

Although I think these should deliver the same results, they don’t. I have started another thread ([url=https://www.portfolio123.com/mvnforum/viewthread_thread,9897]https://www.portfolio123.com/mvnforum/viewthread_thread,9897[/url] ) on just this topic so as not to dilute this thread with a technicality that has little to do with WWoW.

For what it’s worth I’m also finding that the cash flow methods (DivPaidTTM + EqPurchTTM - EqIssuedTTM) are giving better backtests in my sims than the share count and forward yield methods. Will need to do some thinking about why that might be and the likelihood that it will be that way in the future.

Would be interested to know what you find out.

So… Is value investing still working? The underperformance seems to continue. One to three years of underperformance can happen, but five to six years in a row (OK, maybe we can exclude 2013… maybe not) seems a lot. Maybe the market has changed?!

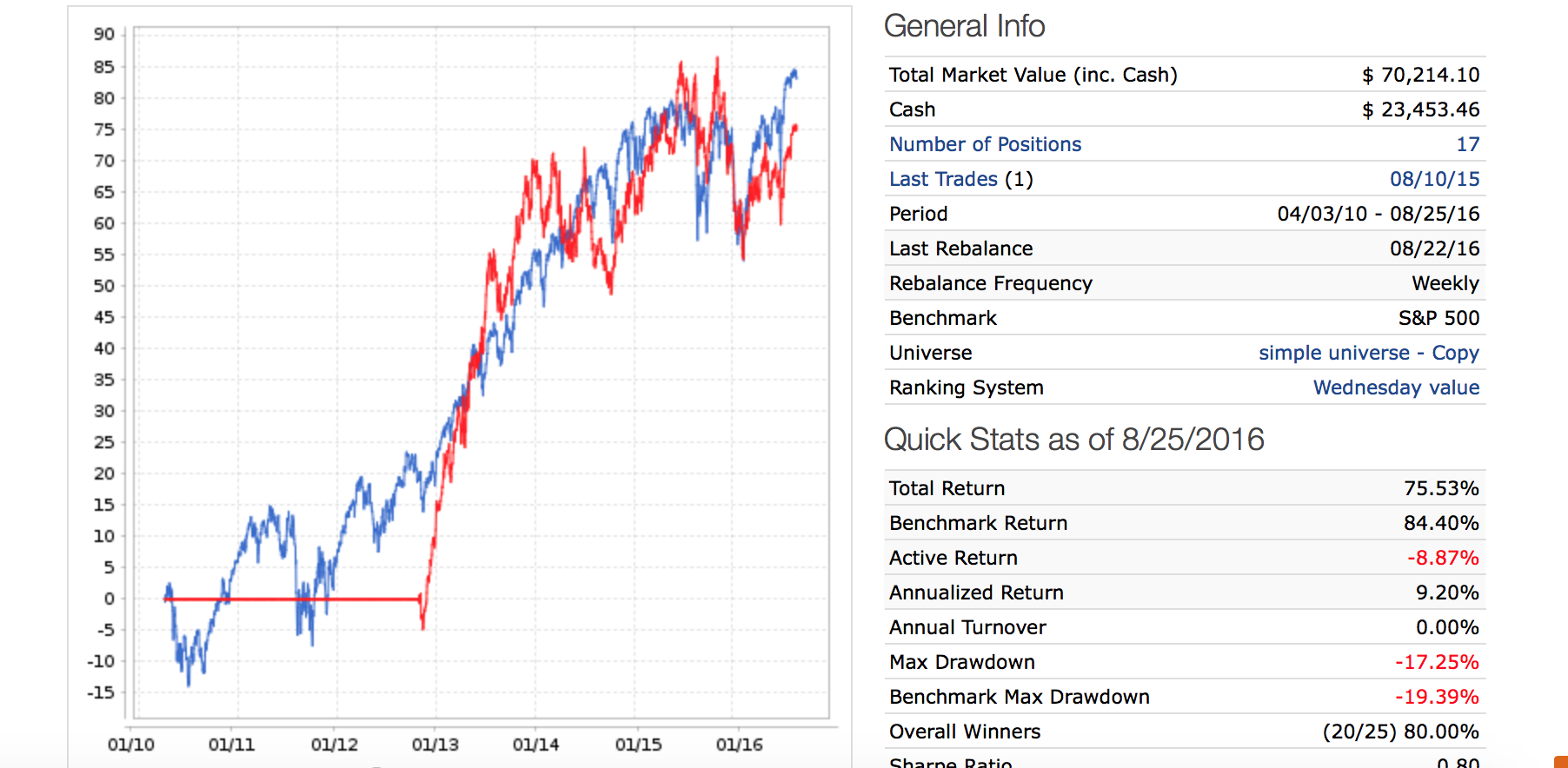

Value has worked just fine over the last 6 years. My simulation is here: https://www.portfolio123.com/port_summary.jsp?portid=1444886. My ranking system is here: https://www.portfolio123.com/app/ranking-system/296322. My universe is here: https://www.portfolio123.com/app/universe/summary/160105?st=0&mt=7.

My results: 23% annualized return since April 2010.

My system: buy top 25 ranked stocks, sell if rank goes below 80.

My ranking: 20% low market cap, 40% low price to sales, 10% each high forward earnings yield, high forward sales yield, high free cash flow yield, and high unlevered free cash flow to EV.

My universe: Russell 3000, minimum $50,000 ADT, minimum price of $1, minimum float of 5 million, no MLPs, no REITs, no utilities, no stocks from corrupt countries.

Additional rules: current quarter EPS estimate has to be bigger than same quarter last year’s GAAP EPS (which also means the stock has to have at least one analyst covering it), most recent quarter EBIT has to be bigger than same quarter EBIT last year, and short interest has to be less than 3% of shares outstanding.

My conclusion: there are plenty of value stocks still to be found if you know where to look. Just look at the top five holdings in this sim: KOP, PFSI, CVGI, BRSS, and CMT, with an average return of 52%.

Add some quality rules here, and you’ll get even better returns.

Yuval,

Nice!

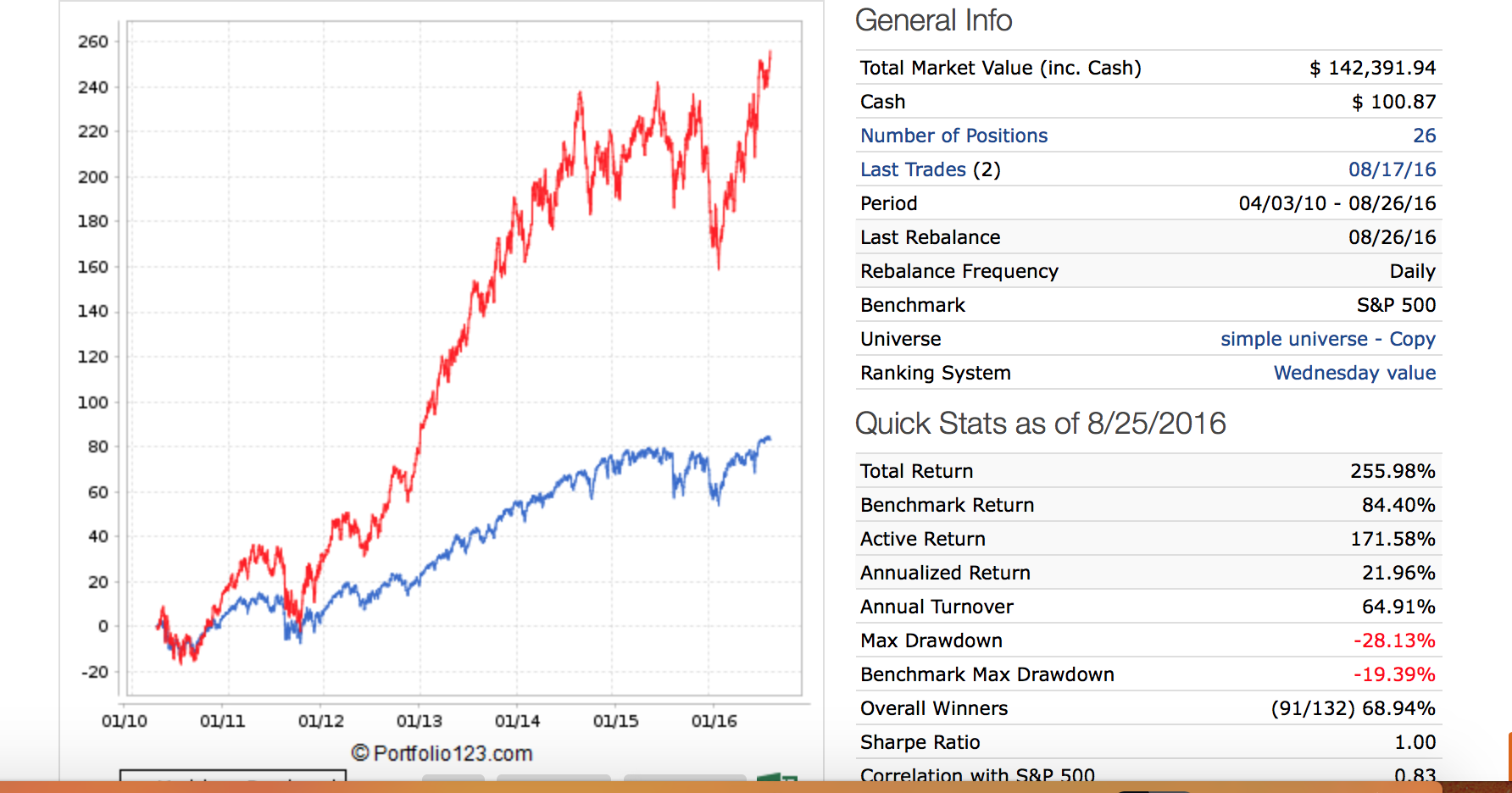

And when I run it with Weekday = 4 and remember to rebalance daily (the second image) your results hold up well: as we discussed in another post. Very nice.

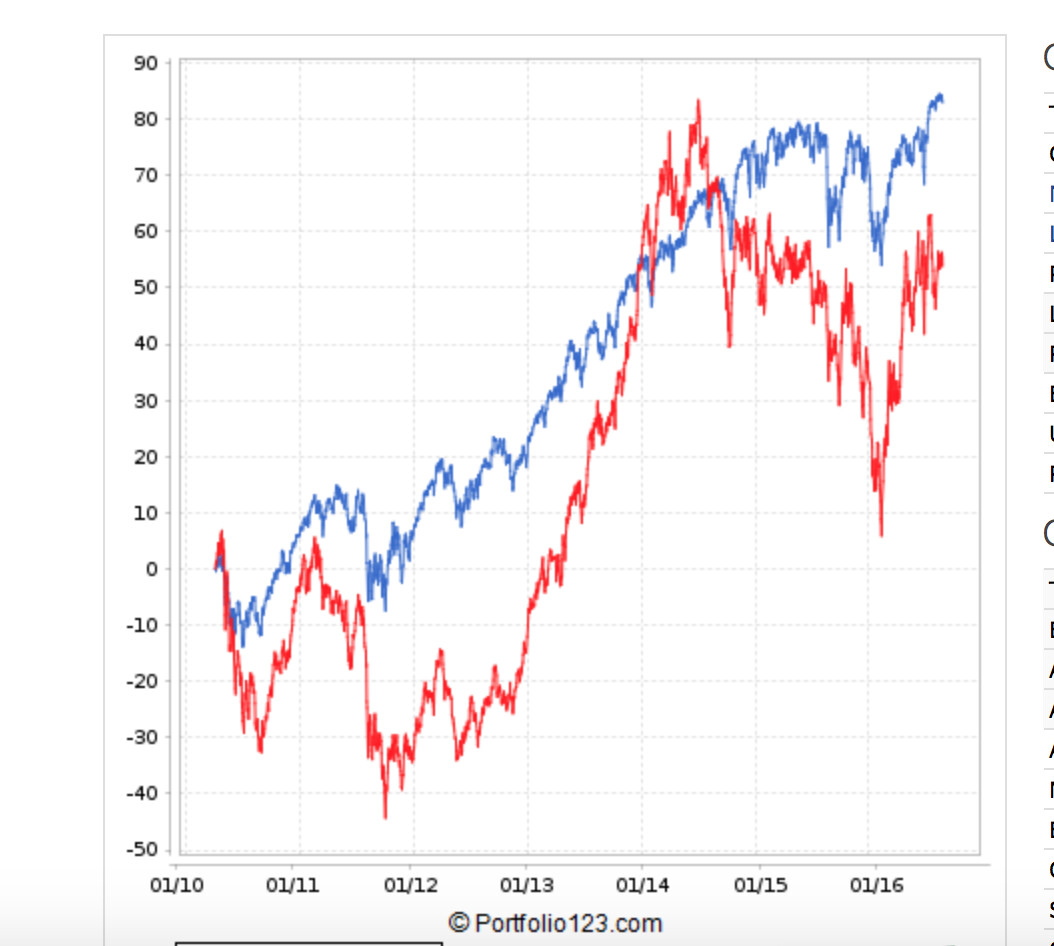

Just for fun I ran your sim using a more liquid universe that I usually use (variable slippage and Next Average of High and Low). Last image.

BTW, another value system that had a drawdown starting the middle of last year and has already had a good recovery it looks like. Actually good on the drawdown over that time period for a small or all-cap value system in my opinion.

Thanks.

-Jim

Value investing will work as long as people ignore mean reversion, succumb to recency bias, are loss averse, etc. So in other words, for a very long time.

Matthew- you have summarized what I was trying to say (poorly) in another long post and what C. Thomas Howard took a whole book to say("How The New Value Investing: "How to Apply Behavior Finance to Stock Valuation Techniques and Build a Winning Portfolio’). His title was almost as long and he didn’t say any more!

Did you add to your universe my growth and short interest rules? If not, the sim won’t work nearly as well. - YT