Hi,

first of all, I love O’Shaughnessy “What works on Wallstreet”. For me it was the best book about stock selection. He has billions under management, I have far less.

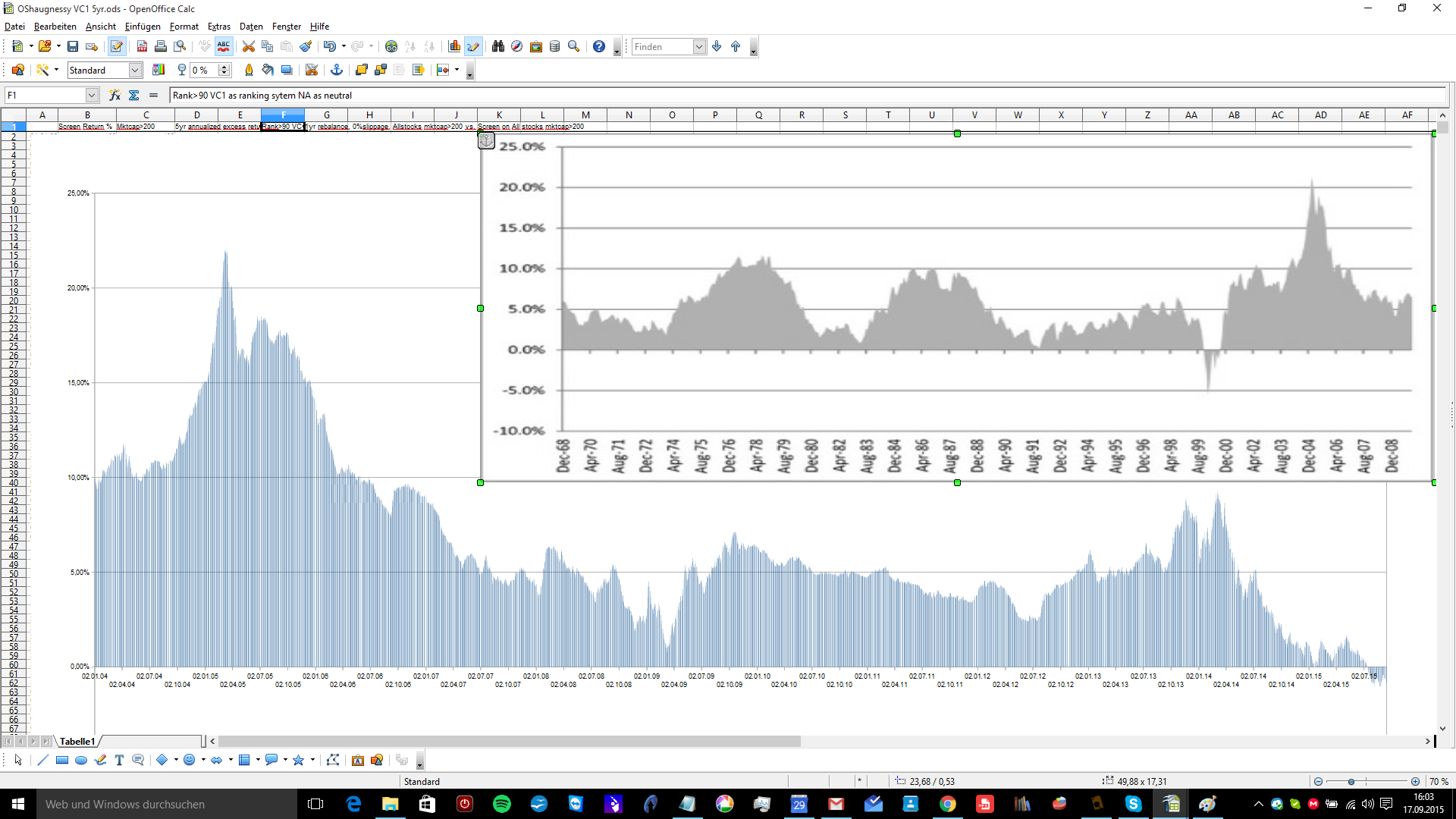

In his fourth edition Chapter 28 Ranking Strategies on page 597 he lists all of his best performing strategies with performance data from 31.Aug.1965 to 31.Dec.2009

So what I did:

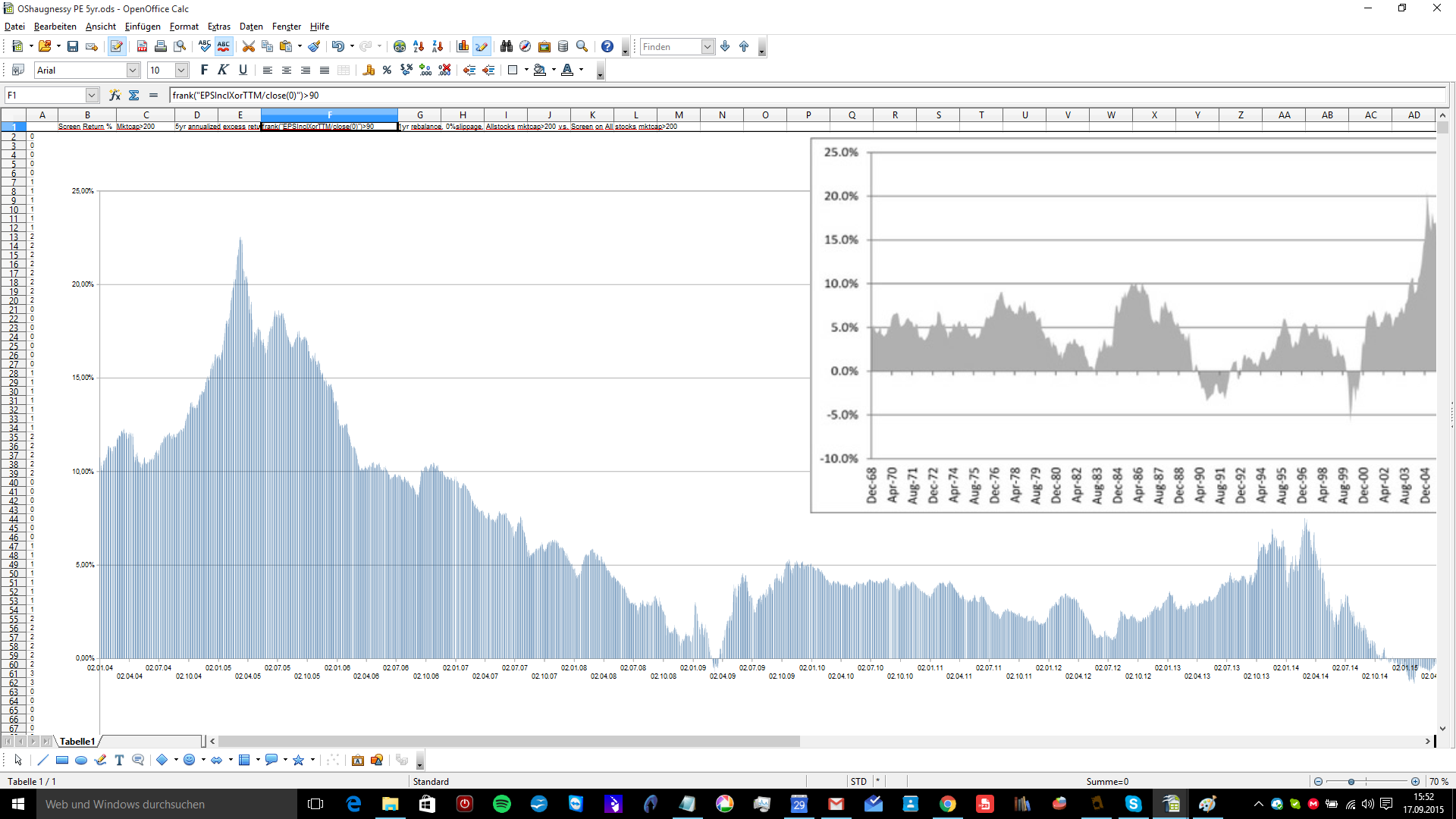

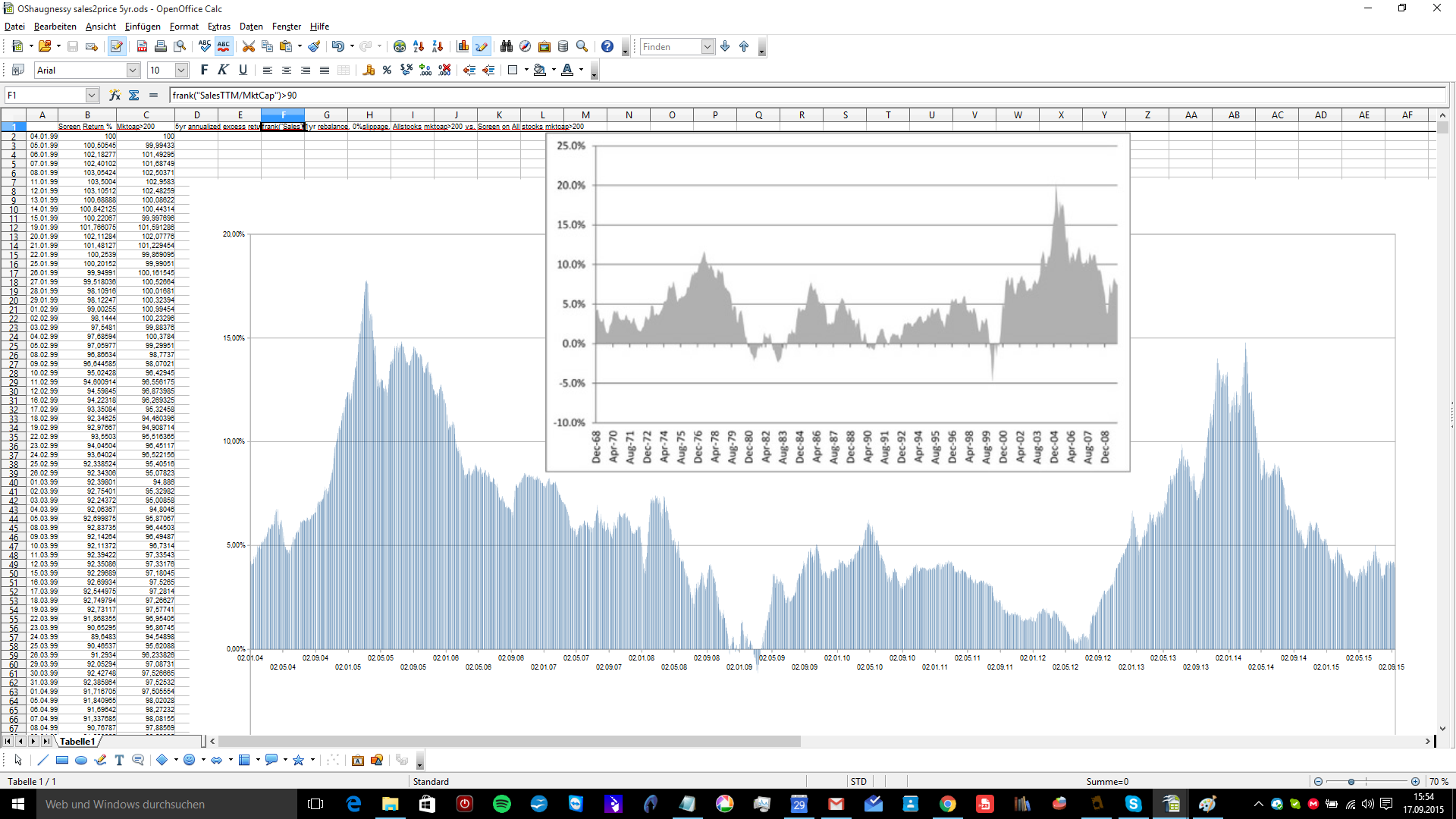

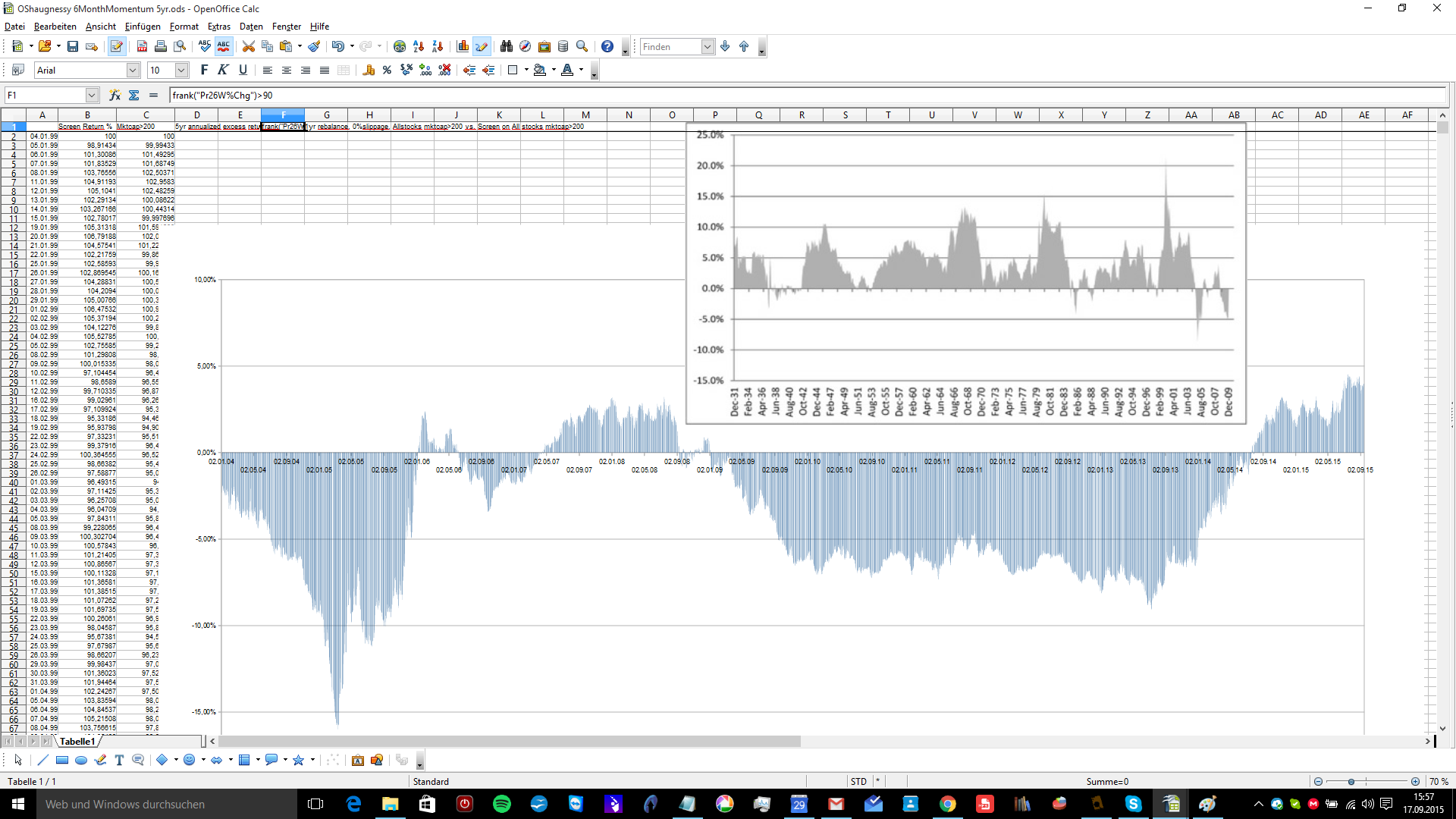

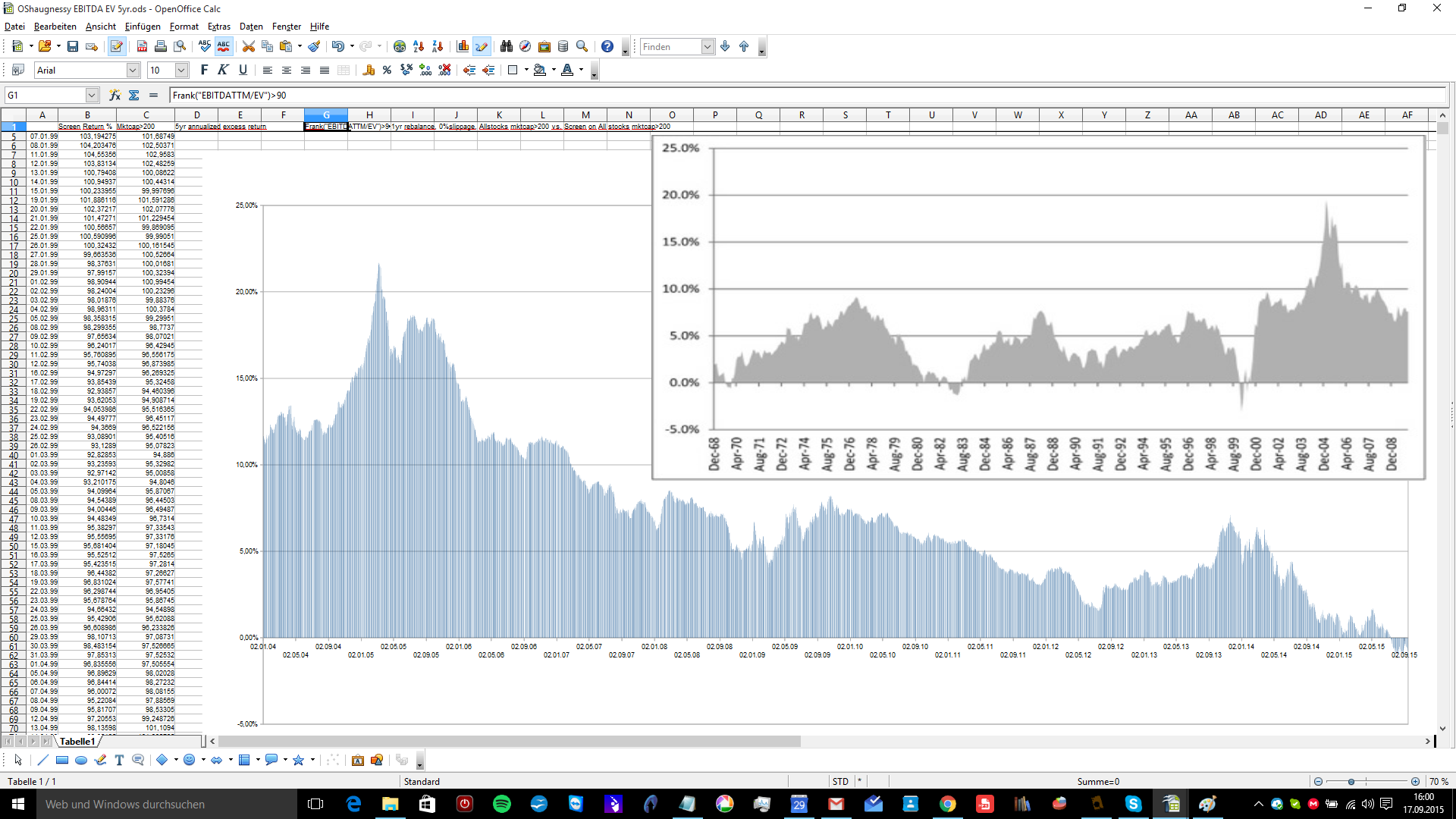

I backtested his top 19 Strategies out of sample from 1.Jan.2010 until today. At least as close as possible. His strategies might have slightly different calculation order and slightly different formulas and different Compustat data, etc… But I am very close, as you can check for yourself. I have made everything public.

The result is shocking. It would have been better to buy and hold Russell 1000, Russell 2000 or Russell 3000 ETFs instead, especially after taxes.

Name and Alpha vs. Benchmark (Russell 2000 w/Div for Small Stock and microcap universe and Russel 3000 w/Div for All Stocks universe)

Small Stocks, PSR<1, 3mom and 6 mom>0, Top50 by 12 mom -0.2%

Trending Value 50stocks -4.5%

Trending Value 25stocks -4.6%

Small Stocks, Value Composite2 (VC2), Decile 1 -0.0%

Small Stocks, Value Composite (VC3), Decile 1 -4.0%

All Stocks, VC2 Top 3 Deciles, 3mom and 6 mom >Median, Top 25 by 6mom -7.6%

All Stocks, VC2 Top Decile, Top 50 by 6mom -4.6%

All Stocks, 3mom and 6mom >Median, Top 25 by SY 0.5%

All Stocks, BP and 6mom >Median, Top 25 by SY -0.2%

Small Stocks, PB Top 3 Deciles, 3mom and 6mom >Median, Top 25 by SY -2.4%

All Stocks, VC2 Top 3 Deciles, 3mom and 6 mom >Median, Top 50 by 6mom -6.7%

Small Stocks, VC2 Top 3 Deciles, 3mom and 6mom >Median, Top 50 by 6mom -2.9%

Small Stocks, VC2 Top 3 Deciles, 3mom and 6mom >Median, Top 25 by 6mom -4.6%

All Stocks Growth -8.0%

Microcap, PSR>1, Top25 by 12 mom -6.4%

microcap, BP Top 3 deciles, 3 mom and 6 mom >0, Top 25 by 12 mom 4.2%

Microcap, BP Top 3 deciles, 3 mom and 6 mom >0, Top 50 by 12 mom 4.6%

Microcap, PSR<1, 3mom and 6 mom>0, Top10 by 12 mom -12.1%

microcap, BP Top 3 deciles, 3 mom and 6 mom > Median, Top 25 by 12 mom 6.8%

I have attached an excel spread sheet with links to each of the sims above and to a few screens with similar bad results.

If you do not want to download the spread sheet, then just search for my public sims username tobiasberr

https://www.portfolio123.com/app/opener/SIM/search

I still want to believe in value and momentum factors. But they did not have a too good run in the last 5 years.

Do you think they will have a come back, a great reversion to mean? Like O’Shaughnessy keeps claiming. You have to stick with your system for 15 years…

Or have his strategies become crowded since he published his bestseller.

Any ideas, opinions or critique are welcome!!!

WWOW sucked.xls (25.5 KB)