Dear all,

Bluecrest capital (a family office pod shop Michael Platt) manage to make money from the recent downturn while other quant hedge funds lost money (including Man Group and RIEF/RIDA from Renaissance Technologiges - not Medallion).

Pls see the updates from Bloomberg and Reuters.

Regards

James

Michael Platt’s BlueCrest Gains 20% on Trump Tariff Volatility

By Gillian Tan and Nishant Kumar

April 8, 2025 at 8:50 PM GMT+8

Hedge fund billionaire Michael Platt’s private investment firm has netted major gains navigating the market turmoil sparked by President Donald Trump’s move to impose tariffs on allies and rivals.

BlueCrest Capital Management is up 20% so far this year, people with knowledge of the matter said. The returns are on invested capital and net of all fees and expenses, one of the people added, asking not to be identified because the details are private.

A spokesperson for BlueCrest declined to comment.

Platt, who returned capital to outside investors in 2016, has used a heavy dose of leverage to supercharge returns at his firm. As a result BlueCrest, which now solely manages the wealth of Platt and his partners, has delivered some of the best trading profits in the world.

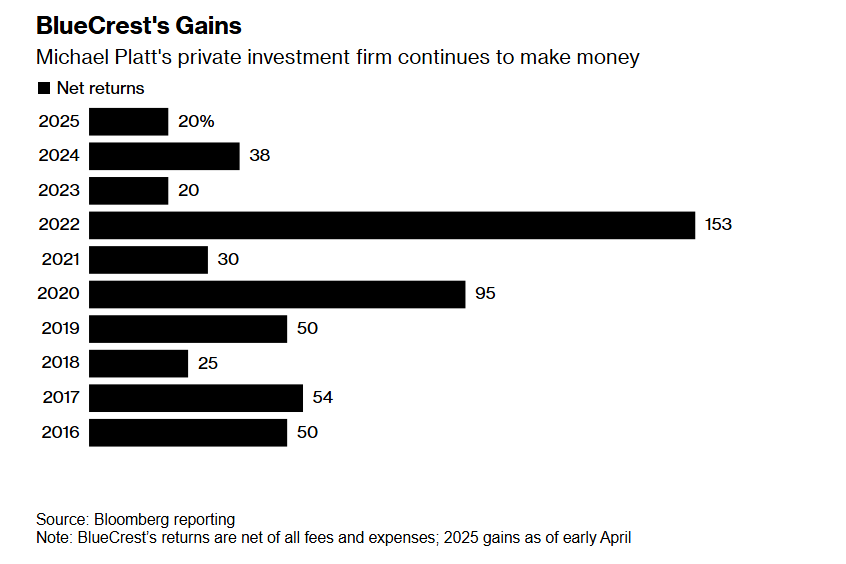

BlueCrest's Gains

Michael Platt's private investment firm continues to make money

Source: Bloomberg reporting

Note: BlueCrest’s returns are net of all fees and expenses; 2025 gains as of early April

Hedge funds have been battling to shield their portfolios from market chaos sparked by Trump’s expansive tariffs. The MSCI World Index tumbled 9.3% on Thursday and Friday, the biggest two-day decline since March 2020. Goldman Sachs Group Inc.’s global fundamental long-short hedge fund clients were down 4.7% over two days.

Multistrategy hedge funds that spread bets across trading teams and asset classes have [fared better] with Schonfeld Strategic Advisors making money this month through Friday, while Citadel lost about 0.35% and Millennium Management declining 0.7%, Bloomberg reported.

It’s not clear how much money Platt’s investment firm manages now, but a court document from 2022 described BlueCrest running $3.9 billion and allocating $15 billion in trading power to its managers.

Man Group Hedge Funds Losing Up To 15% This Year Show Quant Pain

Even the trading machines can’t keep up with President Donald Trump’s tariff barrage, which has muddled algorithms that are supposed to anticipate the direction of markets.

The four main quant money pools run by Man Group Plc, the world’s biggest publicly listed hedge fund firm, lost as much as 7.8% this month through April 9, according to the firm’s website. The declines, which pile more pain on the funds after first-quarter losses, came as their models struggled to change direction quickly enough to avoid market routs.

Three of them are trend followers — strategies that ride momentum across futures markets — and have been whipsawed by rapid reversals this month.

Man Group is not alone in worsening losses. Transtrend’s DTP - Enhanced Risk Composite fund slumped 18.2% through April 10 this year, while Aspect Diversified Trends was down almost 11% through April 9.

A Societe Generale index of commodity trading advisers, a group of many such algorithm-driven funds, shows that the three trading days after Trump’s April 2 tariff announcement were the worst run in two years. The group has now wiped out all gains since March 2022.

Positions across stocks, bonds, currencies and commodities built up over the past 100 to 200 days have all suffered together as those trends sharply reversed in April, Abhijeet Gaikwad, chief investment officer for ADG Capital Management’s Quant Multi-Strategy fund, said.

“They tend to have holding periods of a few months which makes it difficult despite their blend of models,” Gaikwad, who previously worked for Man Group, said. “Their size becomes their enemy.”

A representative for Man Group declined to comment.

| Fund |

Strategy |

April |

YTD |

| AHL Diversified Programme |

Trend |

-7.83% |

-15.15% |

| AHL Alpha Programme |

Trend |

-5.12 |

-9.35 |

| AHL Evolution Programme |

Trend |

-3.84 |

-8.30 |

| AHL Dimension Programme |

Multi-strategy |

-4.89 |

-6.88 |

| Man Strategies 1783 |

Multi-strategy |

-1.55 |

1.96 |

| SG Trend Index |

- |

-6.37 |

-10.74 |

| SG CTA Index |

- |

-5.87 |

-8.24 |

| Source: Man Group website; Data through April 9, 2025 |

|

|

|