There is a reason why institutional investors and hedge funds are often labelled "smart money". I personaly think it is useful to compare performance with the average hedge fund performance (pls see the two links below). It is actually more difficult for most institutuional investors and hedge funds to deliver performance due to their large AUM and lesser ability to profit from and invest in the small caps/micro caps space. In addition, they have significant operating expenses that needs to be covered first.

Therefore, if the performance of some of your P123 models underperformed by a lot. You maybe onto something...

I do wonder what role P123 should play when it comes to strategies that attempt to predict market direction. I'm not entirely against them—I think they might work in some contexts—but I also question how reliably they perform in practice myself.

What seems far less debatable is that volatility is significantly more persistent than returns. That appears to be a widely accepted point, both in academic literature and in practice. For example, option writers rely heavily on implied volatility, not directional predictions—and I believe there's a good reason for that.

So I’m curious: what do others think about incorporating volatility signals, such as the VIX or realized volatility, into portfolio strategies? Not necessarily to make outright market calls, but perhaps to adjust exposure or manage portfolio risk more adaptively.

I’m not saying I’d definitely use such signals in my own models—but I think it’s a conversation worth having, and it could be a factor-based algorithm consistent with what P123 is doing now: not moving into something different (crowdsourcing or prediction markets), which Yuval is concerned about. I also wonder if we have enough members who would actively participate to make a good prediction market (or robust crowdsource).

There’s a solid scientific basis for using volatility to control risk, and I suspect members here could find something practical in that space—regardless of where we ultimately land on broader market prediction.

I personally would not use market direction predictions and generally agree with Yuval on that point. I think there is not much signal and it is a noisy one at that. I agree that I would not use it whether it is a poor signal or there is no signal at all (making that discussion purely academic to me personally). But I would be open to something that uses the VIX or volatility-based signals to guide risk-on or risk-off exposure, and I’d like to see that included in the discussion.

I note P123 does plan on bringing on an EXPENSIVE and professionally developed risk strategy method developed by professional people trained in finance including people from Goldman Sachs. I might prefer to see that emphasized when it becomes available—consistent with Yuval's concern about P123 endorsing and using established methods for risk reduction.

I agree with Yuval. Portfolio123 should not endorse specific indicators or models. But I also think there should be an outlet so we can make community research projects that is separate from Portfolio123's brand.

For example, myself and others have research groups where we share models and ideas openly. It would be great for it to be integrated with some type of message board for community interaction. Recently I sent a message from my personal account to those in my research group and it was misinterpreted by some as an official Portfolio123 announcement somehow.

A lot of what we do on Portfolio123 is self-guided and often isolated. Tools that bring us together for collaboration or discussion would be an improvement. The forums we have now is fine for general purpose discussions. But if someone wants to go down a rabbit hole of machine learning or market timing or dividend growth investing, there should be a separate forum and shared group specific to that which doesn't show up on your feed unless you belong to it.

I don’t disagree with your broader point. But if P123 provides risk strategies—which I think it plans to do—then P123 would benefit from being actively engaged with members. Not benefitted by being less engaged by moving the discussion to a separate forum not monitored by P123. I think members have something to contribute in their areas of expertise when P123 decides to provide services in the areas of member’s expertise.

Not a separate forum. Still P123. But one that you join the groups you are interested in. The current setup is a massive mishmash of topics. 90% of them are not relevant to me so I end up missing the ones I do want to read. Even a way where I can select just the topics and groups I want to interact with.

Sort of like having an X (Twitter) feed where you control the content you see instead of everything all at once pouring in. As it is, 95% of the people don't regularly use the forums. We need a lot more interaction but the current set-up isn't well suited for that.

I actually agree I think. My point is P123 might benefit from actively participating in a forum when it is about a service P123 provides or intends to provide.

For example if this thread were in a separate forum I would suggest that the a staff member actively engaged in providing a risk management module for P123 take a broad selection of ideas from the P123-member finance professionals who take the time to post.

I note that Marco started this thread and is a professional involved in this risk management module. And it is a new feature HE proposed that is being discussed here. Personally I am good with the discussion in this thread. I do not think this thread is a good argument for making a separate forum, myself.

If P123 moves machine learning (which you describe as a rabbit hole) to a separate forum I would like to see Pitmaster and others involved directly with an advanced machine learning P123 staff member that understands machine learning and can interact with Pitmaster in an informed way. I understand that P123 would not be obligated to do that.

A staff member involved in the development of machine learning and making feature suggestions in this forum? Maybe he stopped making suggestions (but didn't he just make a suggestion with a quote from me with regard to crowdsourcing?) Or maybe he is not involved in development? How does that work exactly? I have not been keeping track.

But if he is involved in the development of machine learning and active in the forum that is IDEAL IN MY OPINION!!!!!!l. And in fact, I made the suggestion to hire Pitmaster directly to Marco when he was discussing hiring people a few weeks ago. Specifically: That he hire Pitmaster as part of the development team and that, if possible, Pitmaster might continue to interact with us in the forum to facilitate an informed exchange of ideas, including perhaps, a few useful advanced features suggested by members. But is that what happened?

So my suggestion again: Make an offer to Pitmaster (and whomever else you may consider knowledgeable in machine learning but Pitmaster for sure) to be a member of the development team. And it would be nice if he or some other staff member on the development team interacted with P123 members on advanced machine learning topics.

Ditto for risk management I think. Does any of the discussion in this thread reflect the actual direction P123 is taking with regard to risk management?

Just a suggestion but @hemmerling actually has a point about the level of the discussion in the forum as it is now… We do manage to make the discussions both uninformed and overly advanced at the same time.

Just to keep your hedge within a range. If it gets lower than X% of your portfolio, buy more puts or short more stocks. If it gets higher than Y% of your portfolio, exercise or sell some puts or cover some of your short positions.

I agree with @yuvaltaylor , who has made a very compelling argument against market timing. I have been coming around to this view for a while now.

I have in the past waited until it gets painful, then sell some or all positions and then miss the initial upswing.

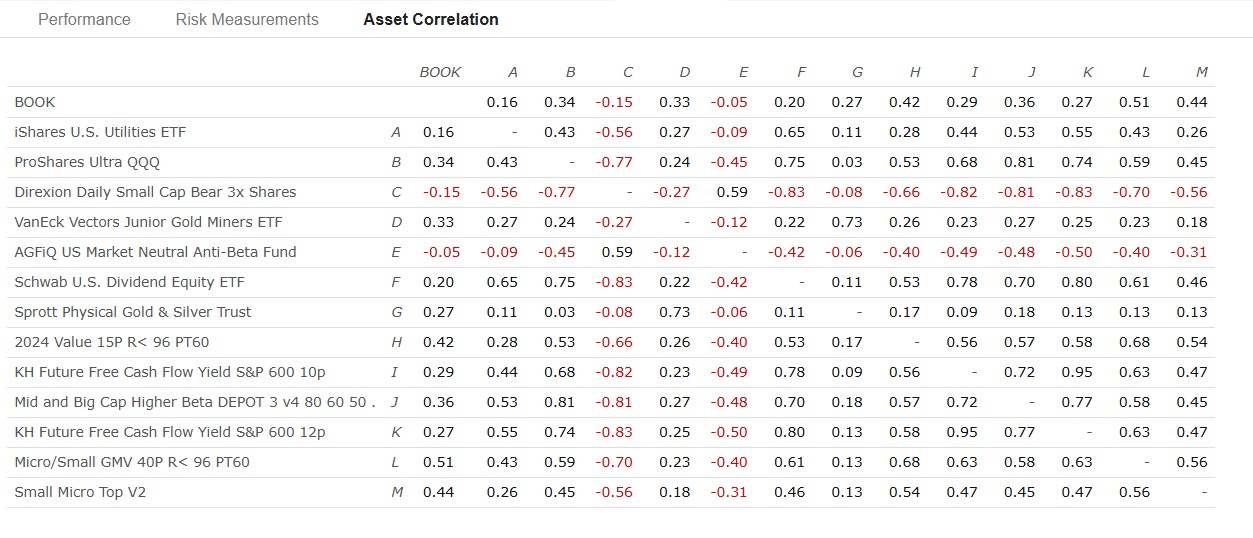

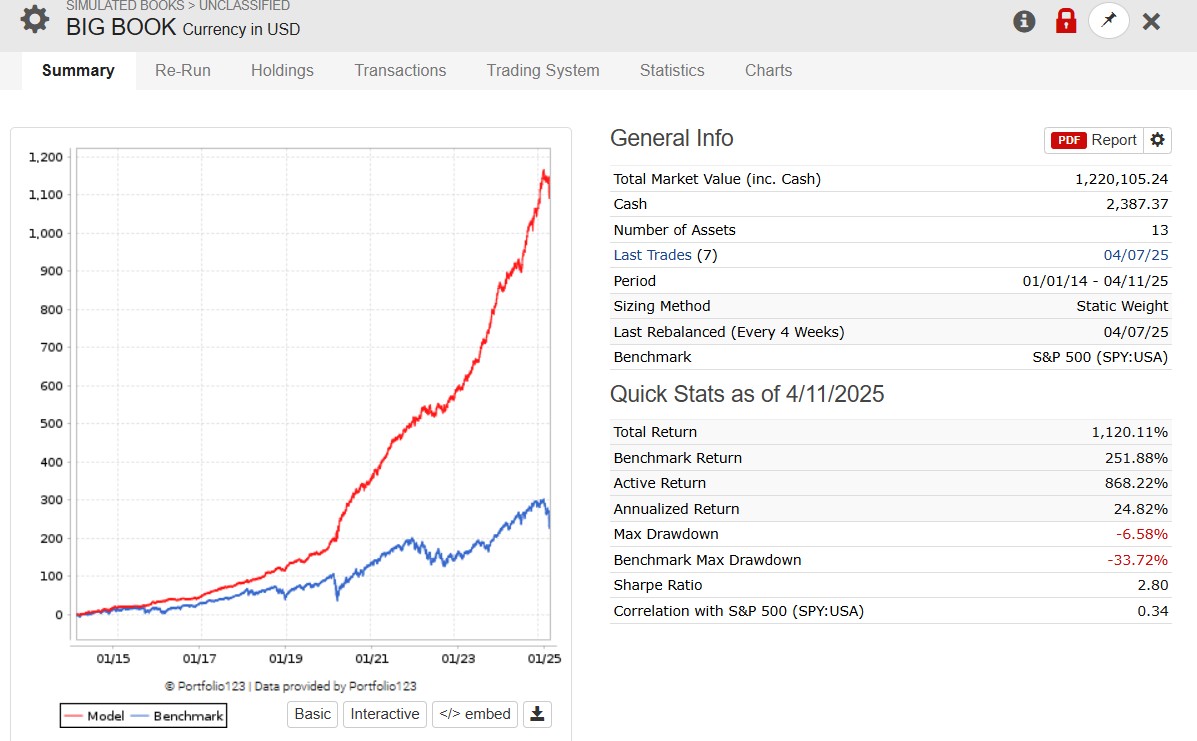

A constant hedge including some poorly correlated ETf's combined with multiple systems seems a much better solution. I have used the excellent Book feature to put it together.

Thanks but we've been a bit embarrassed of it. It has not not been developed in a long time and is missing lots of things. For example the weights are fixed during the sim. And how did you determine the weights?

I agree with plan_trader, Yuval, Kurtis, and others here. I have a hard enough time trusting a market timing approach that I can backtest even over 20 years, as there may be such few events that it's hard to have much statistical confidence in one's approach. And a proposed community driven index would be both discretationary and unable to be backtested, so I'm not sure what trust I could place in it. The idea just seems very antithetical to how most people, I think, use portfolio123.

Ask yourself this question: given limited development resources, is this risk index in the top 5 or 6 most useful things we could deliver to our users right now? I think most people would answer no.

As for the book functionality, it's already a good feature today -- as @plan_trader's book results show. But with a little development, it could be a fantastic game changer for a lot of users. I already export strategy returns to python and use mean-variance optimization to set static book weights in p123.

I made this post 2 years ago about books, and I think it still rings as true as ever:

What you have produced is a survivorship biased portfolio. At inception of the backtest you would not have known the composition of this book. This book will fail eventually, like all other models that are survivorship biased.

As for the "excellent book feature" Marco is correct calling it a bit embarrassing. We have for years tried to get a dynamic allocation into the book module. Or try to incorporate a long and a short strategy, that just does not work unless one goes to some extraordinary length to fool the algorithm.

@geov I think it illustrates a couple of important concepts - diversification using multiple equity models and a constant hedge using lowly correlated assets.

If we are going to say the equity systems have survivorship bias and must be discounted, then what is the use of P123. In regards to the ETF's, maybe BTAL might qualify but it has a CAGR of less then 5% and is only 5% of holdings.

@marco I didn't use any advanced techniques to adjust the weights, just looked for assets with lower correlations and ran it a couple of times with a view to having about 80% equites, hedged with an inverse ETF.

I see I have a 1% allocation to GDXJ, but this was a mistake I actually meant to take it out and just have exposure to physical Gold.

For me the book is extremely useful - I certainly wouldn't describe it as embarrassing.

Coming back to the original thread whether a Community Sentiment Indicator would be of any use. I don't think so. A better indicator (at least for me) is reading "The Economist" magazine. Here is the latest leader: "How a dollar crisis would unfold".

From The Economist:

Since its peak in mid-January the greenback has fallen by over 9% against a basket of major currencies.

So what does that mean? Never mind the tariffs, imports will be more expensive just because of the dollar devaluation. As a result inflation will go higher, interest rates will not go lower.

We don't need a Community Sentiment Indicator to tell us this bad news.

And the price of gold will go higher, $3,386 /oz at the time of writing this.

And has anybody in the P123 community followed what's going on in the bond market?

It's just an experiment, and relatively easy to do. That's all. The most famous subjective sentiment indicators according to chatgpt are below. Why can't our smarter P123 users be famous too?

Investor Intelligence (Advisors Sentiment)

Measures the opinions of financial newsletter writers (bullish, bearish, or neutral).

Conference Board Consumer Confidence Index

Consumer outlook on economy, jobs, and income

University of Michigan Consumer Sentiment Index

Gauges consumer confidence and economic outlook.

So your gold allocation is going up even at these levels? That actionable info is exactly what I consider useful!

And I don't have the time to read The Economist, or any other financial articles. And they put me to sleep literally after a few paragraphs. I'm just not tuned for that type of macro info.