Here is my input:

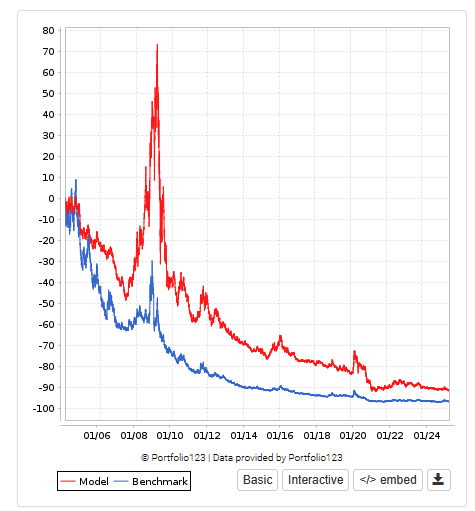

Below is a sample short sim with 40 S&P500 stocks. For all the risks mentioned above, I am using SP500 stocks to reduce the chances that a stock goes up 500%. The benchmark here is (short Russell 2000). Ideally R2K stocks would be the more inversely correlated hedge to my microcap longs, but even a group of 40-50 stocks short in the R2K are too volatile.

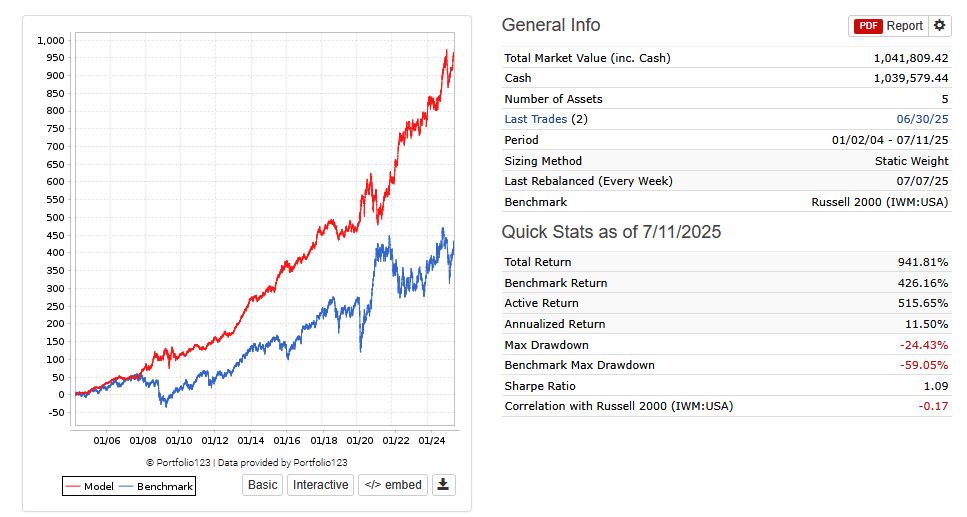

On it's face this short strategy looks superior to shorting the R2K. Here is this strategy 50/50 long short with my long microcap:

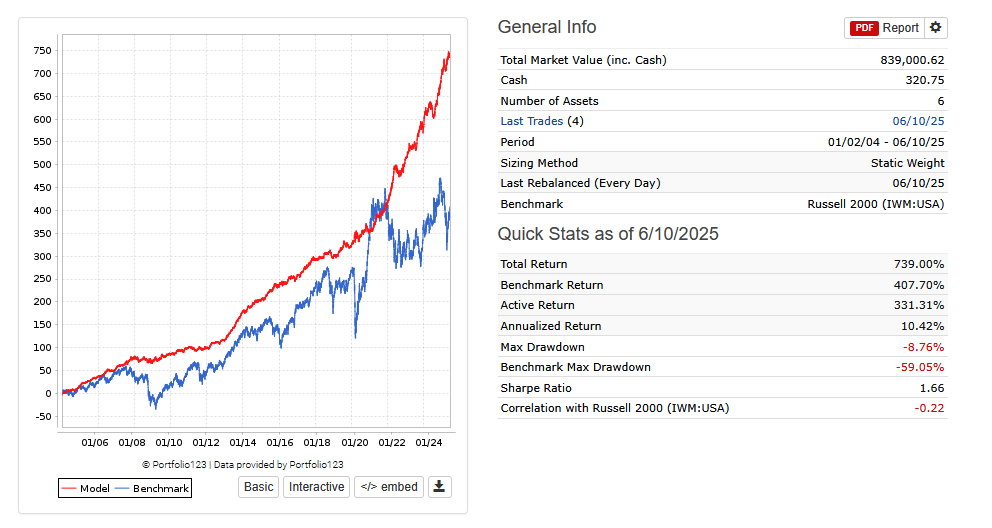

Looks pretty good. But here is my microcap longs with 50% long and 16.67% long TZA:

Slightly less return, but much better curve and sharpe.

What I have found is that TZA is a great tool for those with decent alpha small/micro strategies. It is precise, resets daily, and is highly liquid.

Also now looking at 10% OTM 6 month puts in S&P 500 stocks as a tail risk component. It seems even a 1-2% portfolio allocation can really payout during extreme events.