Summary of the conclusion: (https://www.sciencedirect.com/science/article/pii/S0275531924001296)

- Outperforming the Market: Machine learning algorithms can outperform the market (like S&P 500) by using financial factors to select a subset of stocks. These algorithms adapt to changing market conditions by adjusting the importance of these factors.

- Good Practices Followed: The study followed recommended practices for applying machine learning to stock returns: reliable data, recent data for predictions, avoiding biases, time-series split training, and hyperparameter tuning.

- Limitations and Improvements:

- Transaction costs were not considered. Frequent rebalancing could erase profits due to buying/selling fees.

- Reliance on data providers: data bias or missing data can impact portfolio formation.

- Ideally, hyperparameter optimization should happen with each rebalancing.

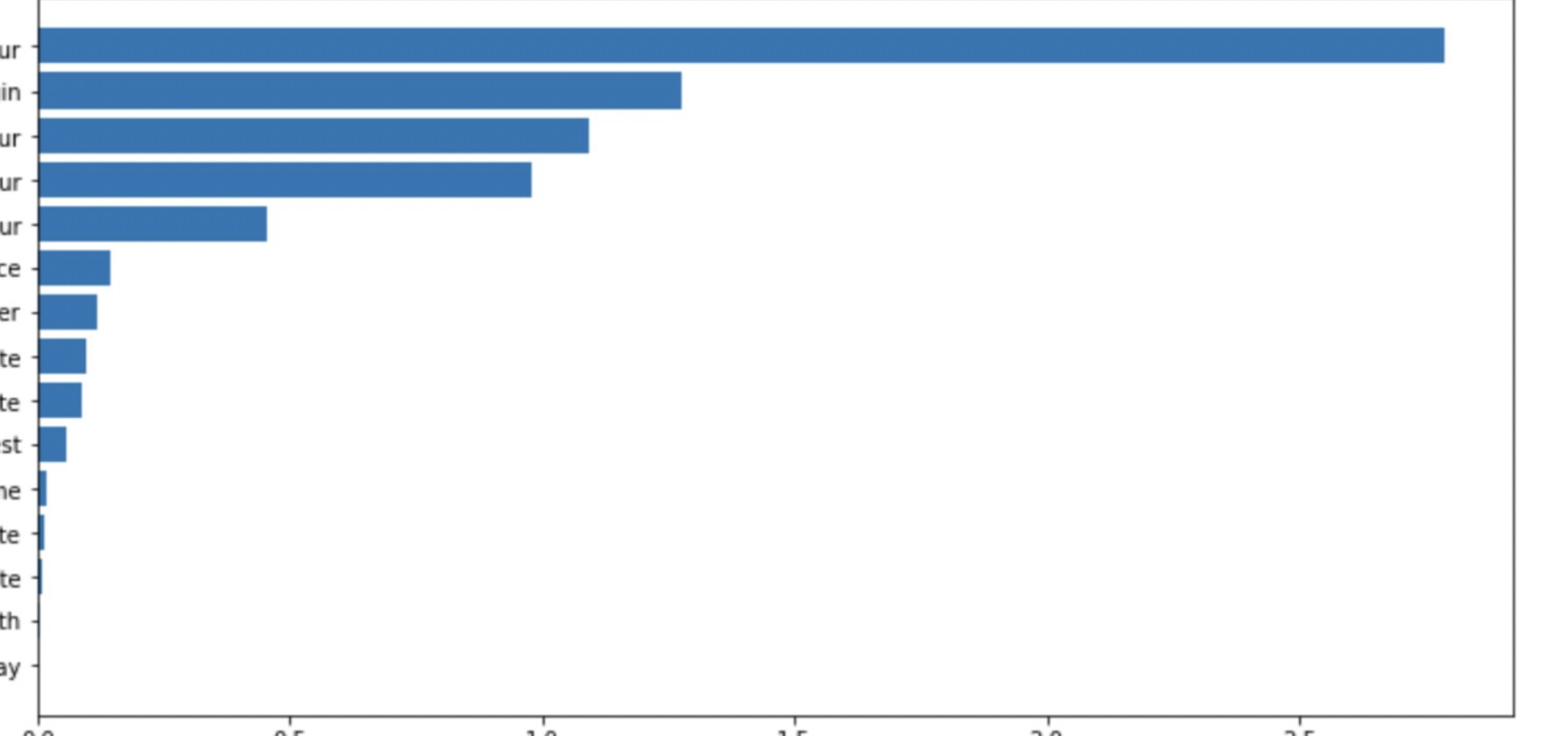

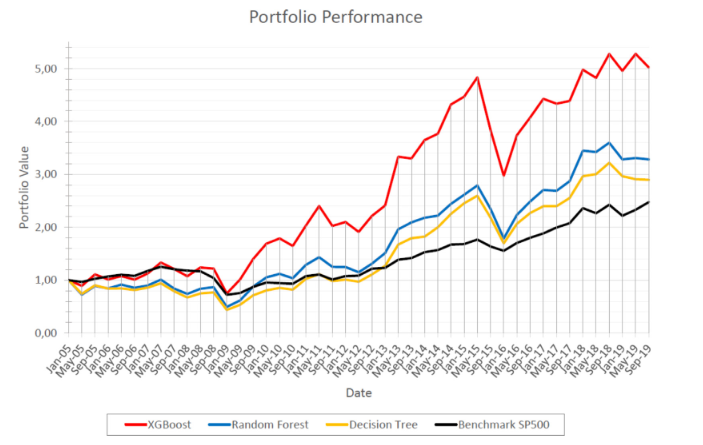

- XGBoost Performs Best: Among the algorithms tested (XGBoost, Random Forest, Decision Trees), XGBoost showed the best performance in terms of classification and financial results.

- Adapting to Market Changes: Feature importance analysis revealed that the algorithms adjust to changing market conditions by giving different weights to different factors over time.

- Future Work:

- Analyze factor importance further using tools like SHAP values to understand not just importance but also the relationship between features and stock performance.

- Integrate risk management for better portfolio stability.

- Explore applying this approach in other markets and with optimized weight allocation within the portfolio.

- Combine this model with a model that predicts market crashes for improved performance.

- Leverage ensemble models that combine predictions from different models at different points in time.