Another approach is the erosion of future margins in the buy rules (instead of negative earnings/cashflow), which is usually a red flag for going long with stocks.

It doesn’t give you a spectacular return, but the return stays robustly near zero with different tests:

evenID-tests

different universes (sectors, canadian stocks)

changing of parameter-values in buy-rules or rank-rules

using additional negative earnings/cashflows or mean reversion

switching to other the short-ranks like “First Generation Shorting Olikea”

It works also with bigger portfolios (up to 50 stocks) in the backtest.

So it should be easier to find shortable stocks in real-trading or to diversify them. I guess, the erosion of future margins isn’t profitable as single strategy, but it is very robust (i.e. for hedging) and could be a starting point for further analysis/developments:

https://www.portfolio123.com/port_summary.jsp?portid=1405383

(The rule for shortable stocks is definied in the universe. The backtest doesn’t work in the first 18 month due to the missing data of sales-estimations. The sim shows similar results with 10 and 50 stocks, but collapses with 5 stocks and the chosen rank.)

Any ideas how to further improve?

Yes, it can be really a problem in the backtests. The problem actually occurs each time when a stock is sold, but it could be bigger when a stop-loss has triggered the selling.

I don’t know any workaround for it, too. So I ran this sim without stop-loss now.

Interactive Brokers is not the place to short stocks. The fees are exorbitant and I believe the reason is they farm out the shorts to a third party (don’t quote me on that). You want to go with a large brokerage that can handle the shorts. For example, TD Waterhouse (Canada) has NO borrowing fee, only the standard margin maintenance fees.

I have been running long-short books for the past 12 months and they are working well relatively (the best performing ‘sleeve I have.’). I hold at least 100 positions on each side (usually around 200) and choose the shorts from the top 1500 or so liquidity of all stocks that are ‘shortable’ - SI% float>1 and close>10 and marketcap>500). In aggregate, these should cost under 2% to borrow historically - but borrowing costs can vary widely over time. I am beta targeting 0 to .2, using a timer to switch the overall beta target level within these constraints. So far so good - but it’s early. The large portfolios are best practice for long-short and market neutral systematic traders (most trade 100’s to 1000’s of positions). Some discretionary traders do well with much smaller position sizes on both sides. The potential to lose money is high and you should start very small and diversify over a lot of positions and also research the best funds out there until you know what you are doing.

I am invested in 2 very good market neutral funds (for past 15 months). They have Sortino over 3 in live trading over past 4 years and have been doing very well in this environment.

I wildly disagree with your assessment of Interactive Brokers. Their fees are the most reasonable of any brokerage I have dealt with, they have a gigantic borrow/lend network so shares are almost always available, fee and availability information is provided in real time, and they only charge prime+1.5% (TD Waterhouse is at 4.5% I believe) interest on margin, which is substantially lower than anywhere else I’m aware of. Plus the obvious benefit of more advanced execution strategies and lower commissions.

I could be wrong, but I would wager more short volume goes through IB than any other brokerage out there.

FYI, I traded short models for several years. Basically shorting the strongest microcaps over the last few days, and exiting on a move down. It was by far my most profitable strategy but very difficult to trade: psychologically, and due to slippage, missed trades, lack of shares, and the very high risk on individual trades. Between the difficulty in trading it and the limited amount of money that can be invested, I stopped trading it - quit while I was ahead.

I do agree that IB is one of the best places to trade short. That is why I have an account there.

your shorting of the strongest microcaps works very well in my simulations. Thanks for sharing this idea!

What is your experience with slippage - is the assumption of the variable slippage OK or is it higher in real-trading? Do you have any recommendation about diversification or risk-management?

Superate - I believe IB charges a borrowing cost and this cost varies from stock to stock. Last time I checked, that cost was 13% to short UWM TDWaterhouse doesn’t have a borrowing cost, it is zero %. So what I am saying is that although IB has advantages in many areas, shorting stocks is not one of them. You should seek a different broker if you want to short stocks. The cost is high.

“What is your experience with slippage - is the assumption of the variable slippage OK or is it higher in real-trading? Do you have any recommendation about diversification or risk-management?”

Variable slippage is probably good enough. Slippage isn’t the issue with this strategy, as much as missed trades. Many people trade something similar (search for Tim Sykes) and you will find available shares hard to find in the best short candidates. I used limit orders close to the prior day’s close. Between missed trades due to the limit and no shares to short I probably missed 1/2 the trades. For risk management I did not use stop losses but I used position sizing based on volatility and I skipped trades where I didn’t like the chart (this part saved me a few times but probably cost me in the long run). I also skipped trades if the stock was in the financial headlines (where I saw it in the news without even looking for it). For these stocks it’s generally better not to read the news because there is almost always significant news - that’s why they ran up.

In terms of IB we should be aslo aware of Short Stock Buy-Ins & Close-Outs procedure.

IB says that they can close our short out with little or no advance notice.

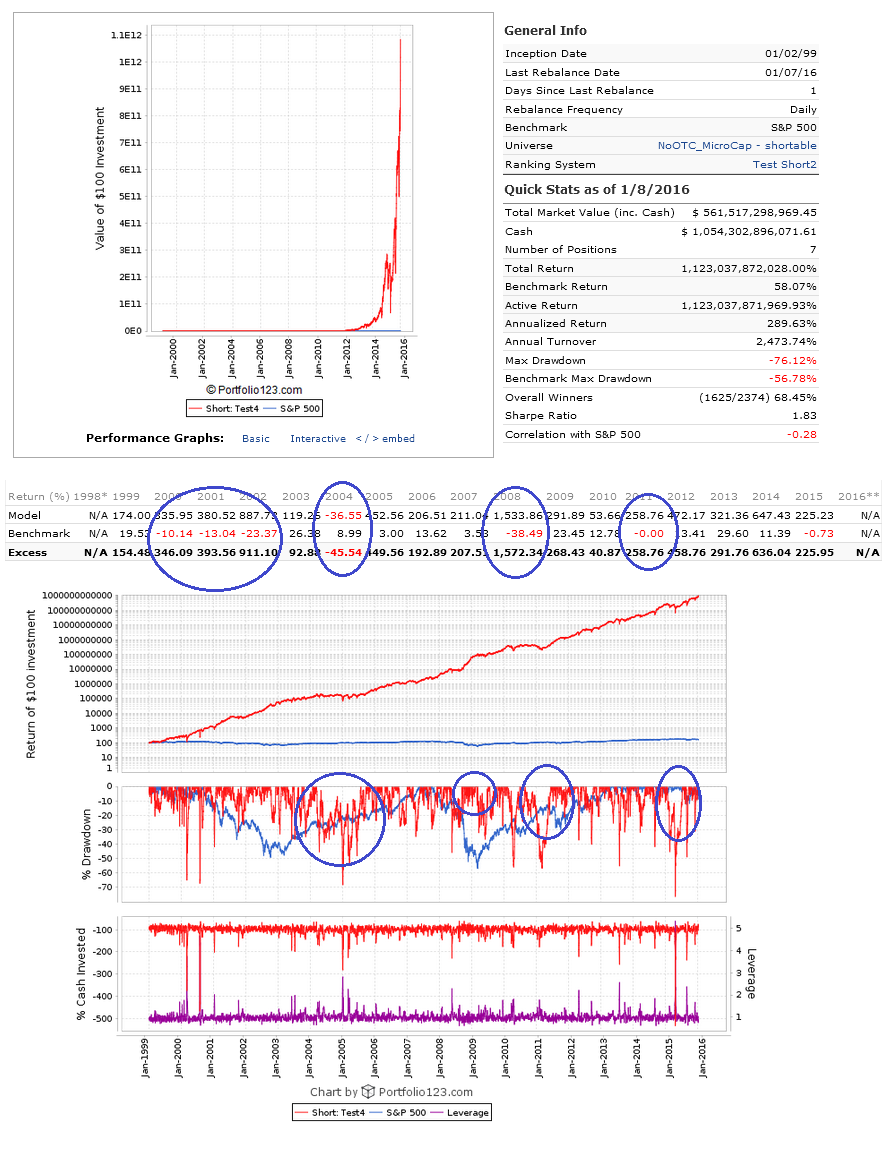

The strategy from dwpeters is a wild ride in Backtests!

Despite of its great return and good correlation to other strategies, I probably won’t use it - it has some bad disadvantages:

it is very volatile and has no fundamental background

it is hard to say, how robust it really is. It works only with a few stocks (appr. 5 stocks), but maybe has some statistic relevance due to the high turnover

if it stops working, the trading costs/slippage will increase very fast

small test in IB: from the 5 stocks with the current highest rank 3 are temporary disabled for shorting

it is probably a full-time job to handle it. It’s more trading than investing.

all the other disadvantages already mentioned in the thread and disadvantages of penny-stocks/microcaps/nanocaps

But it is worth further investigation…

The screenshot is without slippage. Variable slippage leads to 120%/ann.

I am wondering if anyone did short KBIO and what are the lessons learned?

On Nov 20 I saw IB had 7000 shares available to short if you shorted on that day what happened the next day when it went to $45 and IB had no shares to short. I presume you would have been forced to buy back the shares and take a 100% loss.

Based on this I think shorting microcaps requires the same money management as options. You can make a lot of money but you can lose your entire investment.

I did not short KBIO, and I checked my screen and it did not signal an entry either, but if I had:

I would not have shorted prior to the gap because the stock was only back to where it had been recently - this is not strength, and I filtered out stocks with large gaps. In anycase, with an entry after the gap, an exit on the first pullback would have left about a 60% loss - I’ve had worse. I shorted hundreds of stocks a year with IB and only had one or two forced buy backs, and never in a situation such as a short squeeze or huge gap up. I should mention that some of the best trades were the ones that I couldn’t get shares for. There are a number of smart people shorting microcaps.

You can lose more than your entire investment! The gap was roughly a 550% loss for those holding short. I had a 400% loss once, but because of position sizing based on volatility it was comparable to a double digit loss. I actually had losses greater than 100% closed for gains. Clearly the volatility has to be managed and the easiest way to do so is to limit the dollars allocated to the strategy and to positions. Still, as mentioned earlier there are many challenges shorting microcaps.

Use a very simple rule: no shorting of biotechs. Its not just KBIO, You can look at the gap up and screw shorts that has happened so many times in the past mostly in biotechs.