Hi,

does anybody have success in building a shorting model?

I tried it for about 12 hours but absolutly no sucess.

Any hints or is it generally much more difficult to build shorting systems?

Thank you in Advance

Best Regards

Anreas

Hi,

does anybody have success in building a shorting model?

I tried it for about 12 hours but absolutly no sucess.

Any hints or is it generally much more difficult to build shorting systems?

Thank you in Advance

Best Regards

Anreas

My $0.02:

Long-short models that look to play a factor or set of factors and remove market direction can work from what I’ve seen.

Aside from that, shorting is likely best when done opportunistically; i.e., with stocks about which one has a strong bearish conviction.

Systemic short models face a very powerful headwind. Just run any rolling backtest on any model and scroll to the bottom; you’ll see that the market has a heck of a lot more good periods than bad periods. But to make money shorting, you actually need stocks that go down – underperforming an up market is not good enough.

Going forward it will be interesting to see if this changes. We’ve had 30-plus years of declining interest rates pushing stocks upward. That’s over. So if stocks are to continue to rise more often than not, they’ll need some other source of propulsion. That likely, will have to come from earnings.

Very long term, the bias will likely always be up due to population growth, productivity improvements, etc. that influence GDP and profitability. Short term, or even for a couple of years, though, anything can happen.

So in a sense, shorting might be the other side f the coin I’ve always been advocating: Don’t assume from your backtests what something has the potential to do going forward. So if you are bearish and do want to short, you’re pretty much going to have to downplay the impact of raw testing and rely mainly on theory and intuition (as a complete alternative to testing and/or to identify tiny pieces of a test that may show you things at variance from the headline conclusions).

Wow, Marc, you are up early ![]()

It got better during the last 2 hours.

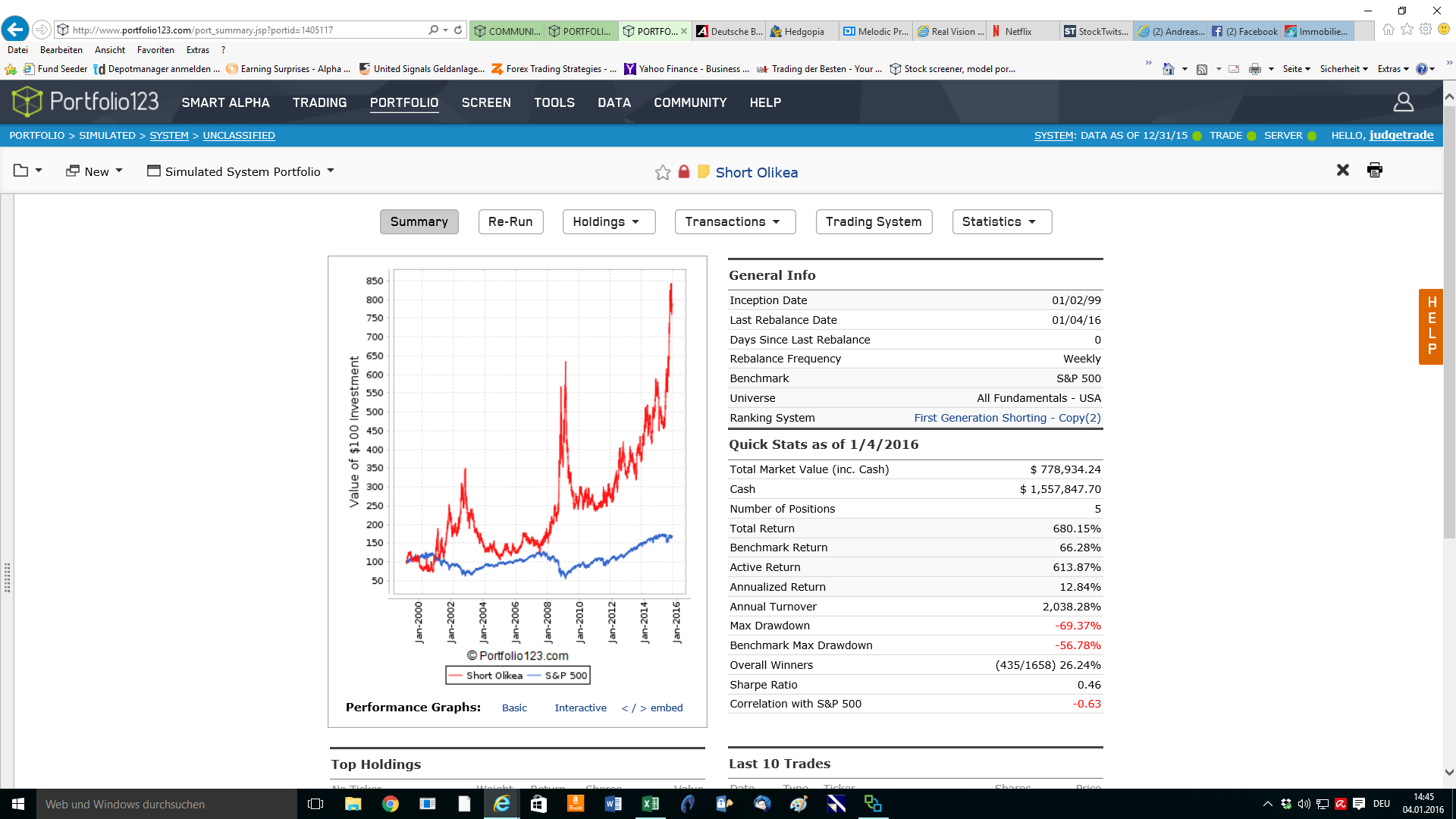

The base, as with my long Models, is once again Olikeas work:

short olikea.bmp (5.93 MB)

here the link, it is public now, it would be great if we could work on it together…

Regards

Andreas

Thank you very much for raising this question.

Is this link meant to be public? I was not able to access it.

http://www.portfolio123.com/port_sim_go.jsp?1451915414533

Hugh

One of the key issues with P123 models and shorting for me is the rebalance. A stock that falls a lot becomes a small position, rebalancing it brings it back to a bigger size. Stocks with big falls tend to have strong percentage rebounds, in which, if a position has been rebalanced, a lot of the profit and more can be wiped out, and then the next rebalance might reduce the position, making it hard to recover the loss if it falls again.

The other issue is obviously that small caps can often be hard or impossible to borrow, especially if there is a high short interest.

Interesting sim Andreas.

Shorting can work, subject to the issues mentioned.

About half the time there are no shares, but when it all lines up you can do well, or not.

I must admit that I usually have insufficient courage to trade this thing.

PORTFOLIO - Summary.pdf (83.6 KB)

Hi Andreas

I have spent a lot of time on shorting models for the healthcare sector. I find that the best I can do generally is find a model which hedges the downturns on the long side without too much loss in return over the long term. If the healthcare index is up x% annually over 5 years and the short portfolio is down x/2% annually over the same time frame than that is good.

I would like to test the First Generation Shorting model you are testing. How can I see it?

Thanks

Mark

I’ve been using P123-created systems for my shorts for a couple years.

It’s certainly possible, but I’ll point a few things out.

Live trading of a short portfolio will diverge substantially from a sim. There are considerations the sim can’t take into account. For instance the Fee Rate of each stock, availability of shares, and margin requirements (if you’re using margin - which pretty much all long/short investors will). P123 can’t sim these considerations, and the stocks my systems want me to short often have fee rates that are impractical, or the stocks aren’t marginable, so I’m forced to drop down to the next rankpos on the list. This isn’t a huge deal in practice, but be aware that simulated results aren’t dealing with these obstacles so they’re probably inflated.

Next, I don’t really expect to make money from my shorts long term. Its possible, but I’m not convinced the systems are strong enough to overcome the headwind of the market and extra trading costs consistently. So far with a somewhat neutral/volatile market my shorts are in the black, but my long term goal for them remains any AR >0%. The goal is to not lose money on the shorts while becoming more market neutral and achieving a much lower risk profile.

I agree with all of the comments above. I would add that the best short candidates are often found among those with weak balance sheets (as opposed to focusing on the income statement).

I started live trading a short portfolio last year, and agree with SUPirate’s philosophy, as my primary goal is to achieve negatively-correlated performance. Ideally, long-term returns are flat or slightly positive, but I would be satisfied with negative performance if the short portfolio underperforms the market (e.g., S&P500 returns +3% annualized and the short strategy returns -1%). I’m currently targeting a beta of 0.25 in my taxable book, and I’ve been happy with the overall results so far.

I would add that due to the issues of shorting (e.g., availability of shares, cost to borrow), I believe it is even more important to diversify with a high number of holdings across many sectors. A short portfolio of 5 stocks is highly problematic when a security cannot be shorted, or the cost to borrow is prohibitive. My short strategy targets 40 positions across a R3000 universe, and I’m not sure if that is sufficient.

Sorry, here is my link… https://www.portfolio123.com/port_summary.jsp?portid=1405117

Hey U5YJ52993752gH7p5fx8,

Wow, that is a great sim! Would love to trade this with a small amount.

Hi Andreas,

I like the idea of working together for developing a robust short-logic. It should work as a hedging instrument in a book and better than shorting an index…

Usually bad fundamentals and negative momentum lead to lower prices. I found out that the following combination works quite fine:

https://www.portfolio123.com/port_summary.jsp?portid=1405151

The model also works with 10 or 20 stocks, but isn’t always fully invested.

Any suggestions are welcome.

Sebastian

EDIT:

One thought: Can the rule “SI%ShsOut != NA” be used as a filter for shortable stocks (because other traders are shorting the stock) or is there a better rule?

Hi Sebastian, wow, that short looks good! do you dare to puplic the ranking system as well?

wow, getting better: https://www.portfolio123.com/port_summary.jsp?portid=1405368

Public!

Unfortunately the ranking is a secret sauce for other models which I may convert to R2Gs ![]()

But the inverse of the bompus-rank is quite similiar and works also good:

[url=https://www.portfolio123.com/port_summary.jsp?portid=1405373]https://www.portfolio123.com/port_summary.jsp?portid=1405373[/url]

If we use the rules of momentum and earnings/cashflow as a rank, this rank is also working. In my opinion we should get a more robust system if we try to create a universe of shortable stocks and a sound short-ranking. And after that use the universe and rank in a sim.

The link to the rank:

[url=https://www.portfolio123.com/app/ranking-system/281448]https://www.portfolio123.com/app/ranking-system/281448[/url]

The ranking is still ok, when switching on the slippage. But it could be more rational to use some kind of “negative Valuations” instead of the absolute values of the earnings/cashflow.

And I found out, that it’s pretty hard to run a short-sim with the rule “SI%ShsOut != NA”. I will consider this in a new shortable universe.

I also switched my universe to public, because it effects the returns positively… Maybe it comes from the exclusion of the cinese stocks, which are often have a downward trend but seem to be unpredictable even in shorting!?

Your sim has really a nice small drawdown!

It seems to be usefull to have a stop-loss, so a single position can’t destroy the whole portfolio…

Usually I don’t like stop-loss in my models, but in short-model it should be more necessary than in a long one.

EDIT:

Here is the model with the rank from above:

https://www.portfolio123.com/port_summary.jsp?portid=1405245

It has a positive return in the shortable universe.

Please check but I believe p123 can stop a short position at the stop targeted price when the daily high exceeds that target price.

For example, one of my models shorted ADPT on 6/1/15 at the closing price of $72.84 with a 50% entry based stop.

The stock was covered on 7/24/15 at $109.26 which is exactly 50% higher than the entry price of $72.84.

On 7/24/15 the open was 105.20 the high was 113.55 and the close was 108.90.

So it stopped out at 109.26 when the high of the day exceeded (or equalled) 109.26.

This can be a problem in backtesting because the target price may not be available to trade at.

The more conservative approach would be an exit at the high but this is not an option

{kind=link}