[quote]

FWIW, my market timer, which is closely based on this blog post - https://www.philosophicaleconomics.com/2016/02/uetrend/ - indicates that a recession is imminent (unless the S&P 500 gains another 35 points today). Basically, the unemployment rate has been above its 12-month average two months in a row

[/quote]How much of that spike in unemployment was temporary and due to the government shutdown?

Unemployment rises as the economy strengthens due to people who had given up looking for work starting to look for jobs again. At least that is what the talking heads say …

The best part of this shutdown will be when people realize how much of the federal gov’t has zero impact. From my own experience, saying this in a federal government office gets frightened looks. It wouldn’t be scary unless there were at least some truth in it.

This is a good thing. Damn the torpedos.

Earnings growth isn’t looking too good either.

The debt markets seem to be saying right now that the sky is not falling.

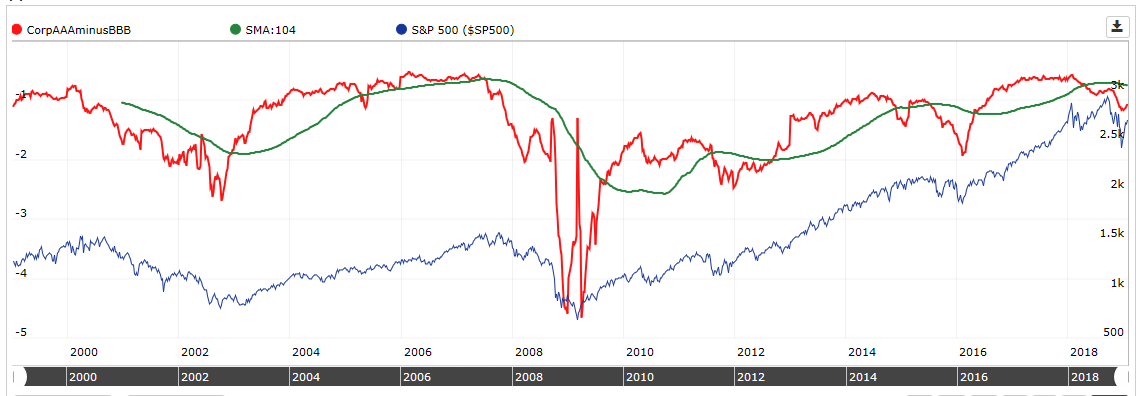

The CORPBBBOAS spread, AAA-BBB spread and TED spread all seem to be shrinking (very slowly) and the way I interpret that is the debt markets think company’s free cash flow can handle debt (which is high). I think that is a good indication. Another POV on earnings stability, at least.

Am I reading this right?

David, your post leads me to point out how a recent post in this thread by me was absolutely wrong, and I’m surprised that nobody called me on it!

In a post on my 2-factor timing model, regarding one of the factors, I said it: “… compares the average corporate AAA and BBB bond rates for the All Fundamentals universe and signals bearish when the difference in rates is low relative to their historically averaged difference. I think of it as signaling a concern by investors that the best AAA rated corporations, on average, don’t have significantly less risk than BBB rated companies. The comparison also works nicely between AAA and B rated bonds.”

There is a slight bearish potential when the difference is small, but the much more obvious ongoing effect occurs when the difference is larger than on average. The AAA bond rate is less than the BBB rate, so AAA minus BBB is a negative value. A bearish signal from this factor, as I am using it, happens when that difference becomes more negative, not less, as shown in the plot below. The difference between AAA and BBB rates increases, not decreases, so my reasoning for the effect, as I am using it, was bogus.

Regarding the recent narrowing of the rates that you point out, the narrowing is in place but my model still shows this one factor as a bearish signal, for now.

have been Long and still ling until sp500 75 ma is broken and (!) 75 MA of Earnings are broken too…

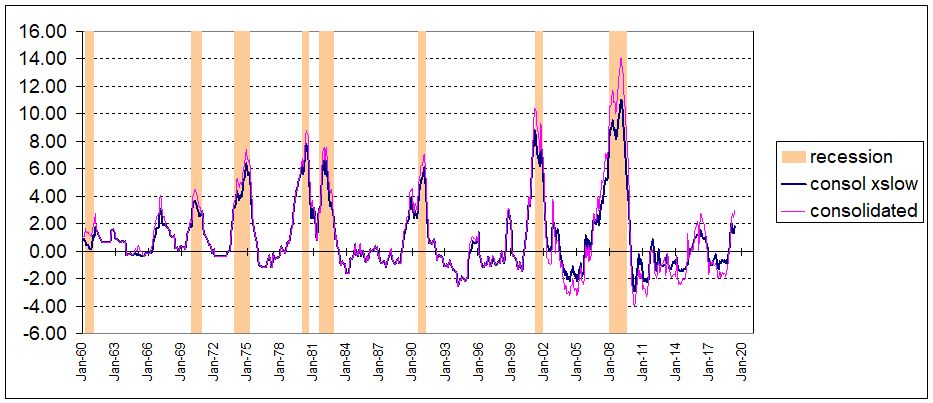

Hi all. I’ve been working on a recession indicator also and figured I’d share this.

- It’s new and still under development -

- It uses mostly FRED data, and a lot of recent government data is not updated yet due to the shutdown - so December data is pretty spotty and end result will probably be higher, but I don’t expect much more given the remaining series.

- some of the most recent updates are better than I expected, so what looked like some worrying trends in housing and corporate spreads seem to have reversed.

- some data didn’t exist the farther back in time, so the growth of amplitude of the signal over time is due to that.

So I guess overall, the signal I’m looking at is inching up, but some of the scarier trends from a few months back seem to have stabilized some, and the absolute magnitude is of the signal is small presently.

The model does not incorporate global pmi, so the developing bad trends in Europe and Asia are not showing up in the indicator. That is probably the main external factor that I’m concerned about now - lots of major economies like China, South Korea, Germany, Italy have mfg pmi below 50. Japan is close at 50.3. Almost all countries are downtrending. I don’t how the deteriorating global pmi feed into US, but I suspect it’s not helpful.

Statistically speaking a recession must be around the corner i.e. within a two year time frame.

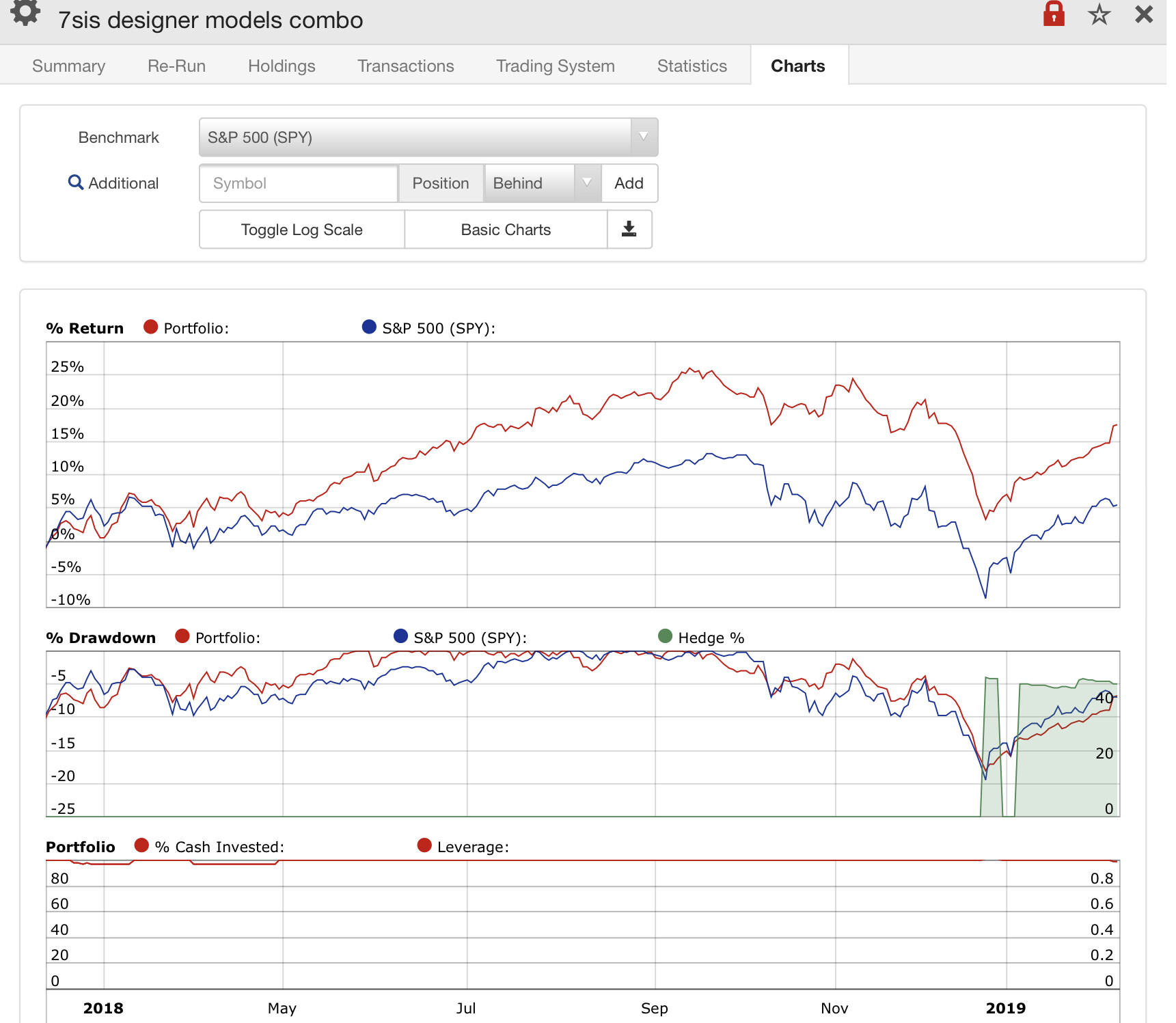

I follow trading my two designer models: one has market timing active right now, the other one not yet. Overall I can‘t complain about performance, although big tobacco has spoiled the party a bit in December.

I was re-looking at all of my port’s return and they all started to deteriorate at about the same time, last summer, 2018.

I think it was due to the trade war with China: “China’s Commerce Ministry accused the United States of launching a trade war and said China would respond in kind with similar tariffs for US imports, starting on July 6, 2018.”

The markets have been going up steadily, partially, it seems, because of the ‘good news’ about easing trade tensions.

Projected SP500 earnings have slumped so it is real but I wonder if this whole thing was effectively news-driven by worse case scenarios of trade? The analysts who created the projections were in the same negative and fearful state of mind as everyone else.

It now looks, to me, like this was a false downturn caused by a perceived macro event, ie, jawboning on a trade war. The other indicators for the economy remain strong.

Too bad we had to go through this. It is not clear at all that it was worth it.

If I was a technician, I’d think we just broke trend in housing starts. It’s just one datapoint in a single month (December) where alot of things were going on, and seems perhaps conditions improved since then. On positive side permits held relatively flat. It’s of note the market did not seem to react very negatively to this though.

My 2 factor market timer, based on corporate bond rate spreads and a comparison of S&P500 earnings to yield, is signaling an exit tomorrow (6/10/19). Other timers I am tracking are still in the market. I probably won’t act on this signal but will watch.

Bob, in the interest of sharing, these are my five indicators. I need a total of any four of the five to be negative to sell. As of yesterday’s P123 update, all are still positive:

showvar(@SPprice,sma(50,0,$sp500)>sma(200,0,$sp500))

showvar(@SPeps,sma(5,0,#spepscny)>sma(21,0,#spepscny))

showvar(@Fedmodel,Close(0,#SPRPBlend)>1)

showvar(@Unemp,(Close(3,#UNEMP)-Close(0,#UNEMP))>0)

showvar(@credit,(close(0,##TEDSPREAD)<.8) & (close(0,##CORPBBBOAS)<2) & (close(0,##CorpBBB)-close(0,##CorpAAA)<1.5))

credits to P123, George Vrba, Steve Auger and others

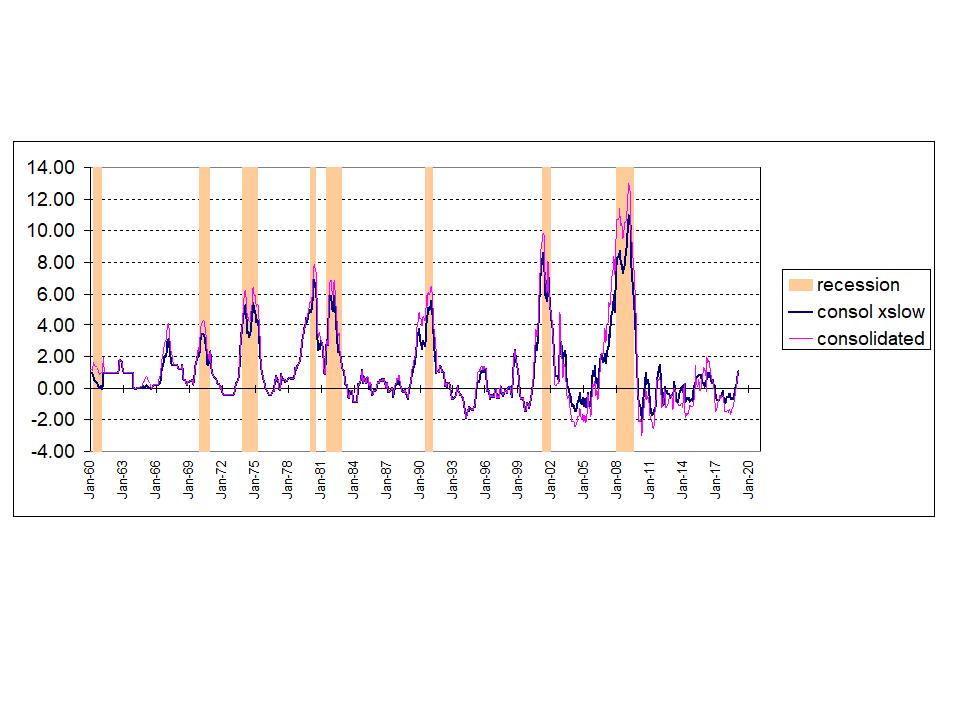

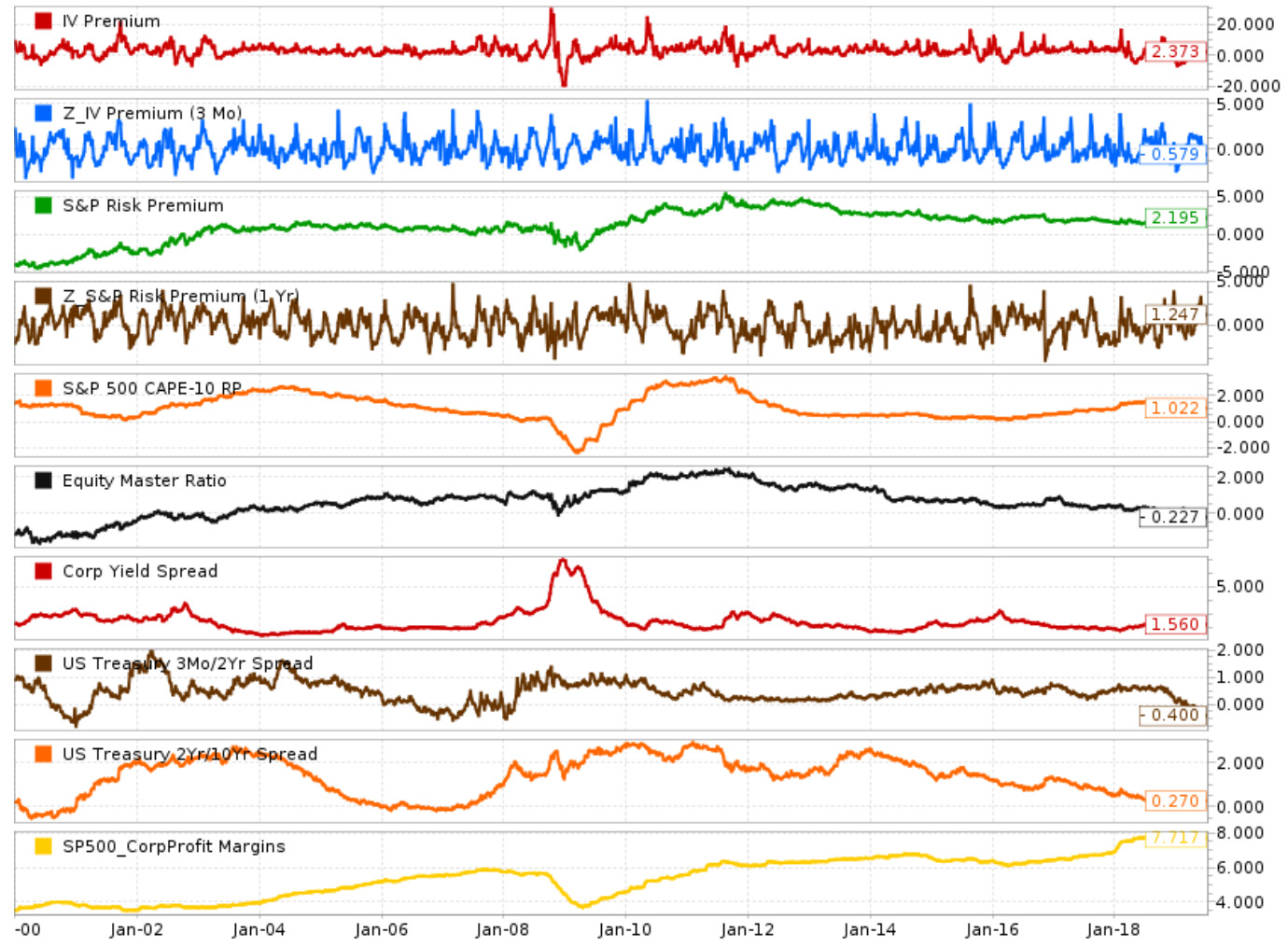

fwiw, here’s what my macro recession tracker looks like now. I’ve been in the “pay attention, be cautious, but stay engaged” state for a while now.

In a linked article, Growth and Trend: A Simple, Powerful Technique for Timing the Stock Market, the author points out:

So, basically, with perfect foresight, we could’ve had 170 bps over the market. And that’s excluding all alpha decay that has occurred over the past 70 or so years.

BORING.

Stay invested, my friends.

As a follow-up, my two factor timer jumped back into the market today, only staying out one week.

I have bullish view on fixed income and bearsih on stocks, probably gold and oil up.

Of all the market indicators I follow, the flattening of the US Treasury yield curve and corporate margins (vs GDP) are the most worrisome. Everything else is business as usual.

I don’t even worry about the unemployment rate because the correlation between stock market returns and the broad economy is almost nil. And the same could be said about the corporate margins versus GDP, except that forward earnings are meaningful.

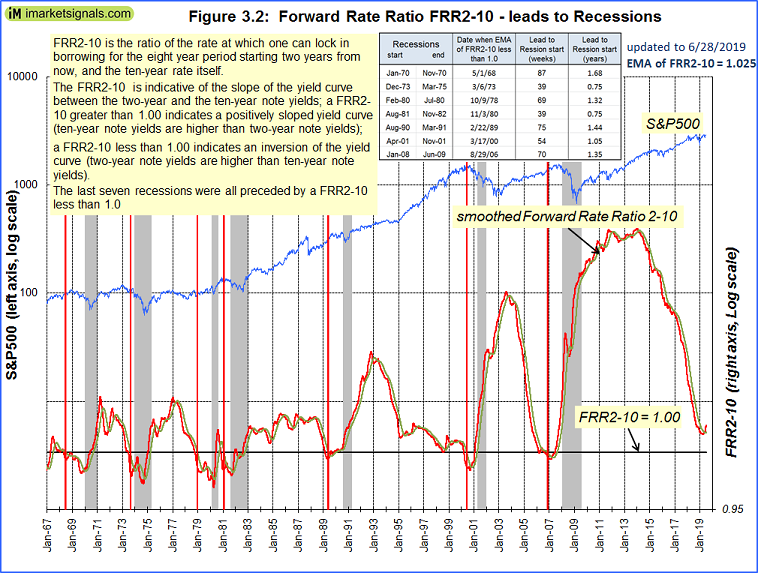

I am not particularly concerned about the yield curve. I follow the 2yr-10yr yield spread as shown with the Forward-Rate-Ratio which has not inverted. As one can see from attached chart the FRR2-10 made a trough before it reached 1.00, indicating that the yield curve is steepening again. So recession warning is not coming from the yield curve.