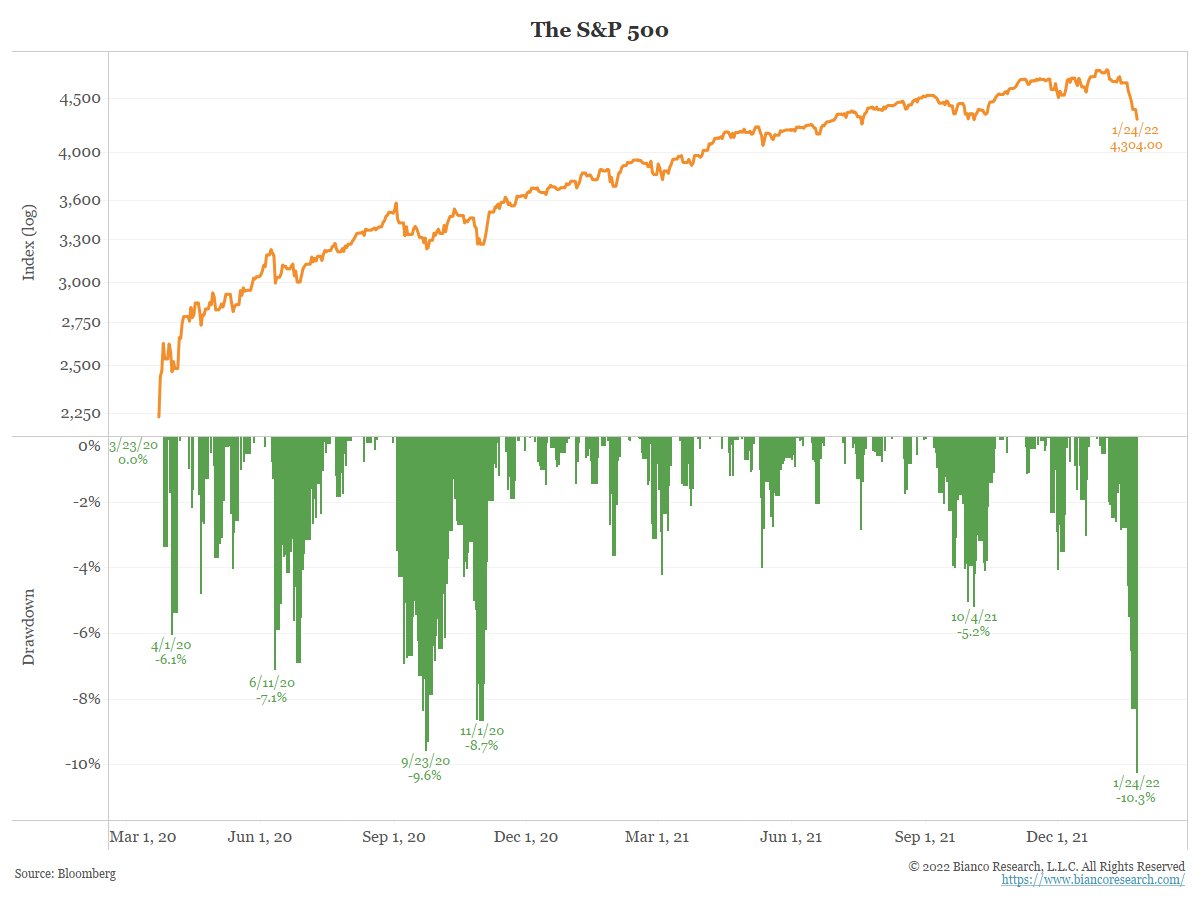

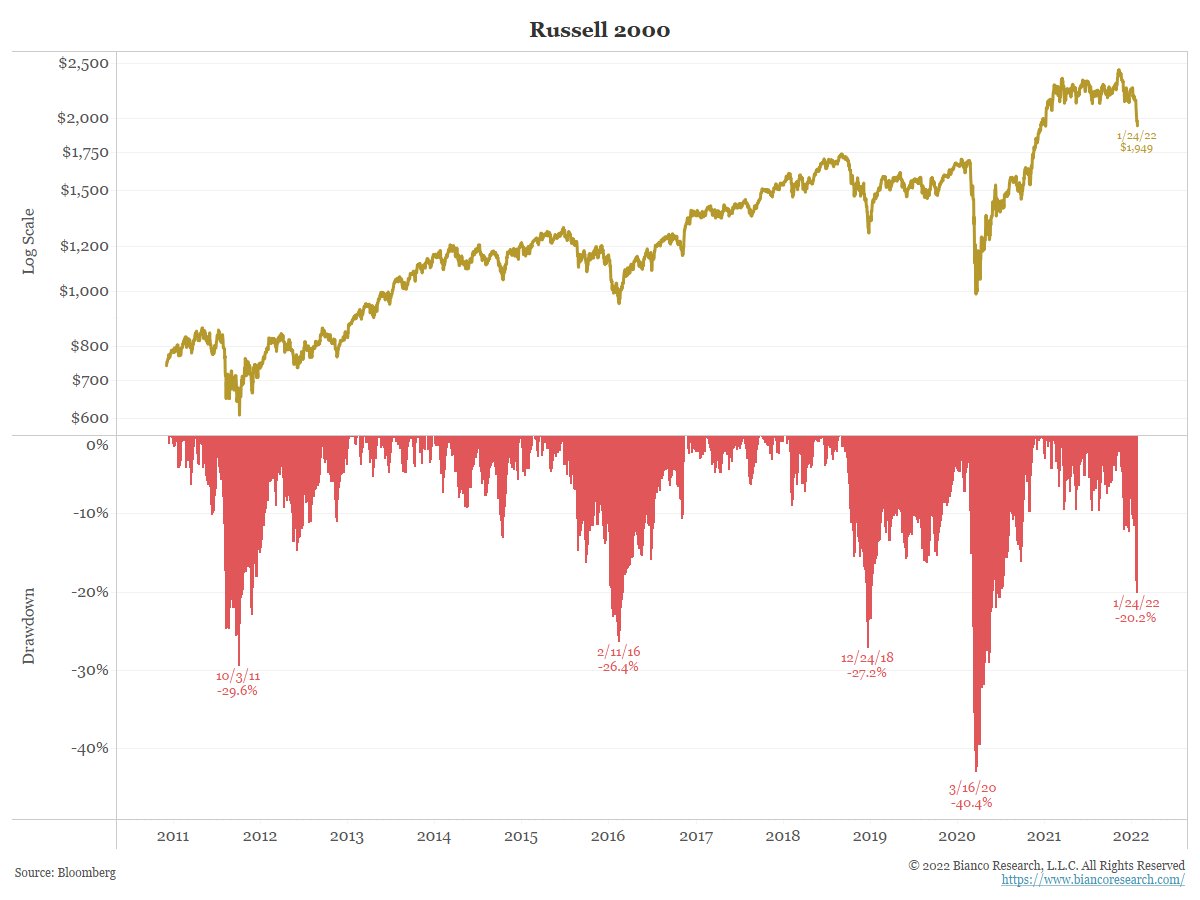

Yes, I agree that it’s impossible to predict, but I’m also astonished by how strong the entire year of 2021 was, and had expected some huge annual corrections but didn’t see them. So I’ve been thinking that this is an expected correction that should have happened sooner, but like I mentioned, no one knows.

I do not believe it is possible to time the market, but we do have some economic indicators that can provide some hints. It is used slightly differently in each model, and the best link to one of the models is probably this: http://www.philosophicaleconomics.com/2016/02/uetrend/

You are correct that the text are insufficient to completely comprehend the model, however they do provide some insight into which metrics are employed:

"…Real Retail and Food Services Sales (RRSFS, a measure of economic consumption) and the Industrial Production Index (INDPRO, a measure of economic production) " … " GTT-UE Rate: At the close on the last trading day of the month, calculate the 12-month average unemployment rate (UNRATE) as of the end of the previous month. “…”… “If recession is signaled, compare the S&P 500 (SPY) to its 10-month moving average. If it will close above the average, go long the S&P 500 (SPY) at the close, otherwise move to cash.”

“… To know when to switch between them, SPY-COMP monitors 6 different economic indicators. When no indicators are signaling recession, the strategy remains long SPY, regardless of what price is telling us. If any one of those indicators is signaling a potential recession then it defers to trend-following to confirm”…

Macrochart on P123 is also a good place to test the predictability of different indicators.

But, as I previously stated, I don’t know, but I’m not Jeremy Grantham, so I don’t see a bubble that will send the market down 50%…