All,

In my limited experience people at P123 are not that bad at using their discretion to move into stocks near the bottom. They know there will be a bottom and are less fearful than the average investor. Nobody gets it perfect. Risks can be asymmetric and the average P123 user gets it at a gut level.

The harder question is what to do now–at a possible top in the market–to keep some “dry powder” at hand.

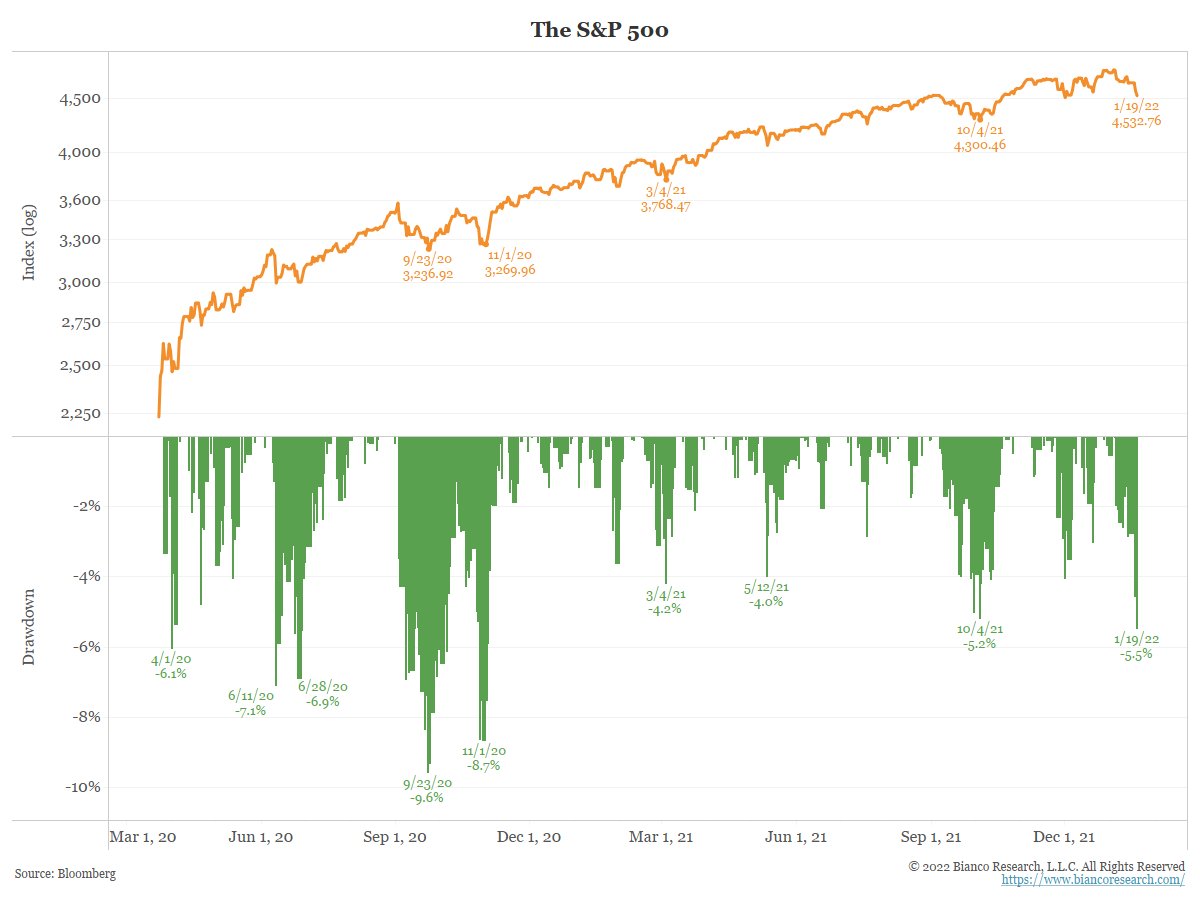

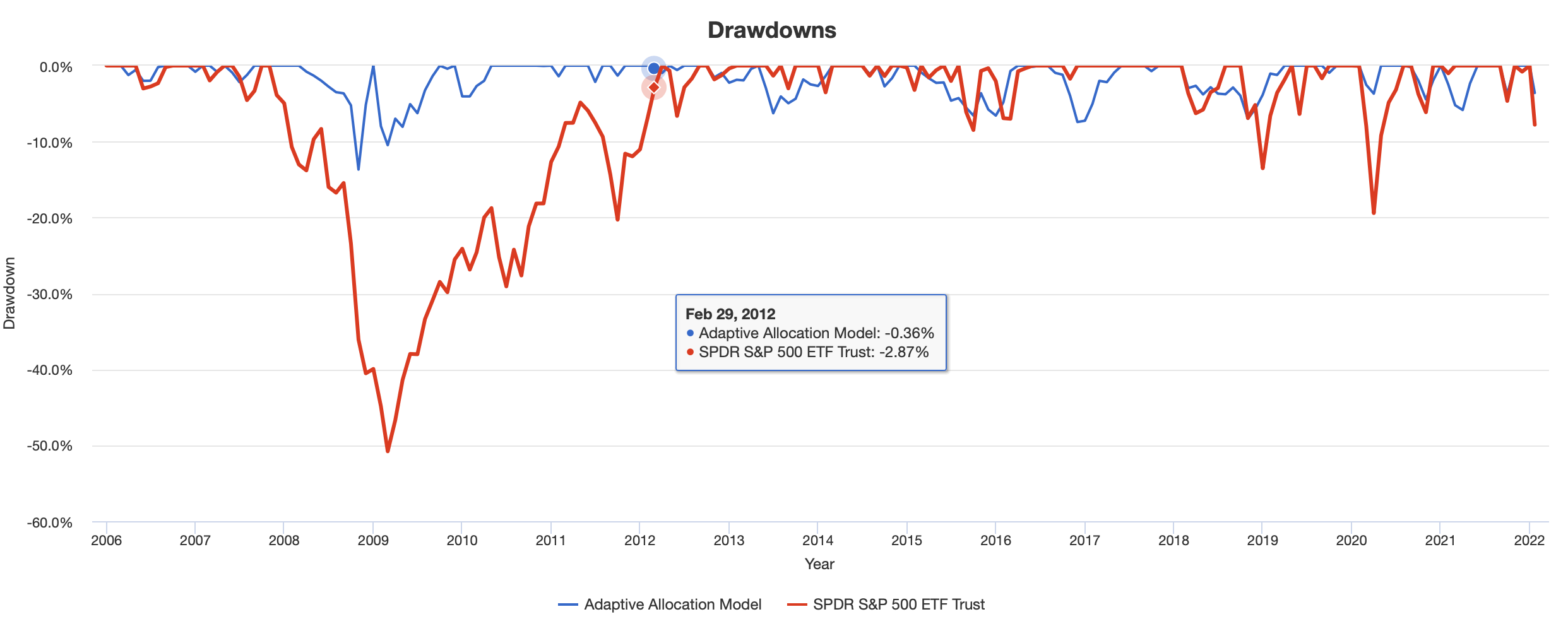

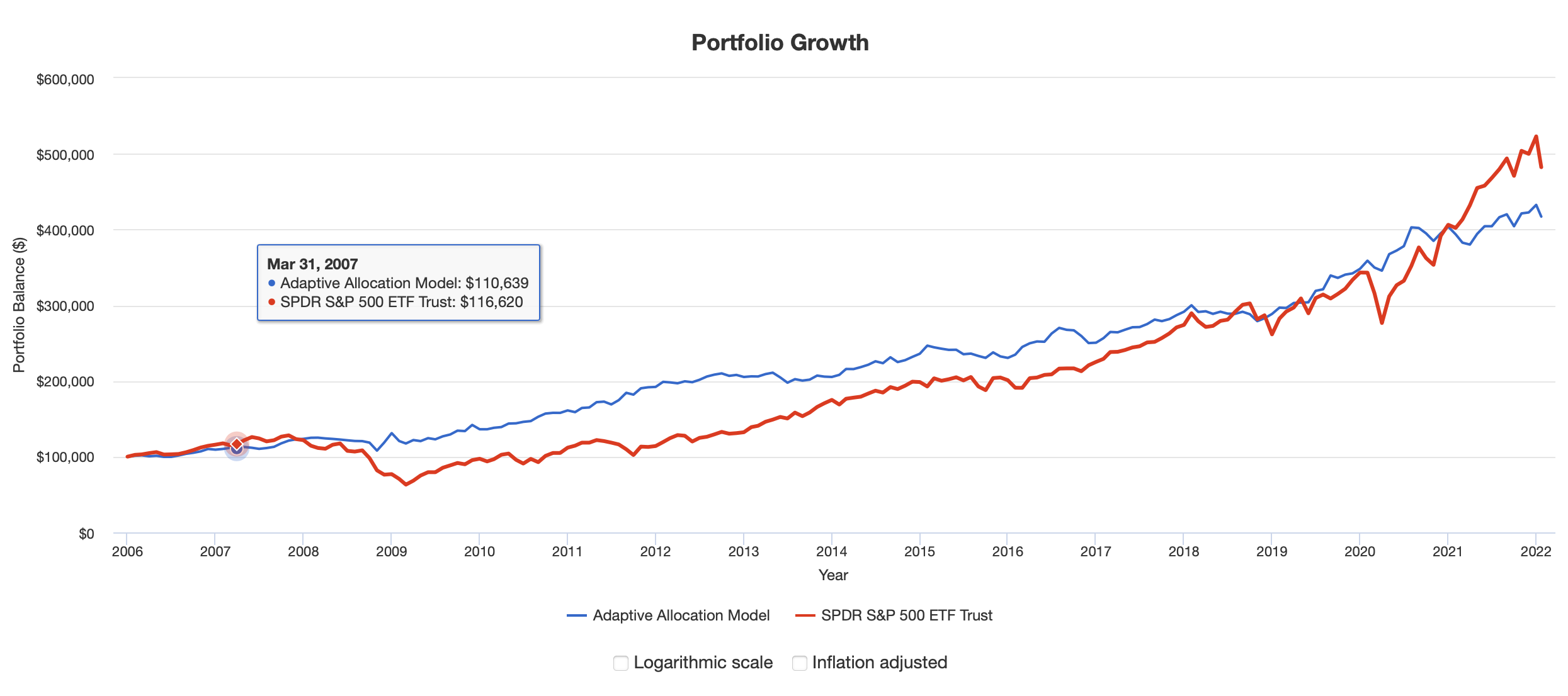

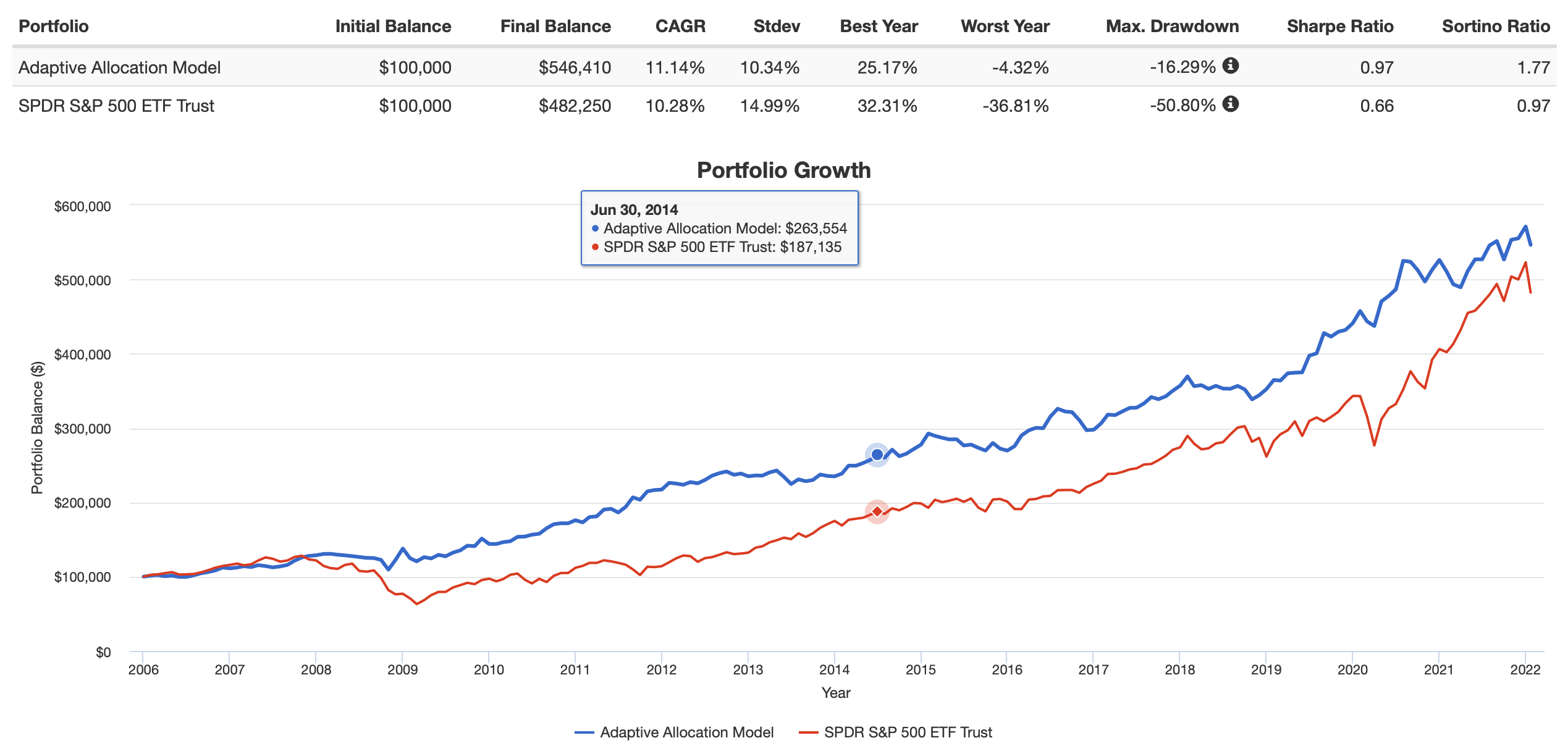

Risk parity (using volatility for the last 3 months) of SPY, TLT and GLD rebalanced monthly will probably save you from a severe drawdown (image). You could keep using your ports in place of SPY and sell TLT and GLD near the bottom–going to 100% ports when you think it is the right time. You could get more fancy at the risk of ignoring Occam’s Razor. But you could probably do a better than just SPY (or your ports), TLT and GLD.

One could also use some leverage, minimizing the underperformance of the diversified portfolio. It would increase the risk of the diversified portfolio but there could be more dry power–to switch into your ports at the bottom–if you used leverage as part of a long-term strategy.

Buying at the next bottom could be a once-in-a-lifetime opportunity. Or not (as I am not good at predicting).

As you can see you would have underperformed recently by diversifying (without leverage) but it is unclear what will happen going forward if you started using something like this today. And the real question is will SPY mean-revert anytime soon? I think Georg is right that it will do this. The only question is when.

But when it does, you might have some money to switch into your ports as Florian suggests above. Or not. Staying 100% long in a port if you are sure it has alpha and that you will not be shaken out near the bottom–especially if you are young–is fine. But you should probably be sure it will have alpha going forward.

For me it is a matter of survival instinct. My wife would kill me while I slept if a capitulated after a 50% drawdown with our retirement funds. I want to live.

Edit: BTW, here is the same strategy with 20% leverage. You would not necessarily have to even try to time it. I think this may be Mark’s point (simplified in my discussion). I think he is right. But also, the risk can get pretty asymmetric as Florian, Steve and Georg correctly suggest above. James (ustonapc) has an advance way of managing the asymmetric risk that I do not fully understand at this point. I do think some of it could be implemented in a SEP-IRA and is worth learning, I am just not there yet.

They all make great points, IMHO. No coincidence that all are professionally trained in mathematical specialties and/or finance (without exception).

A Black-Litterman model would be a formalized method to merge discretionarily ideas with a mathematical algorithm. Probably a BS, hand-waving method, IMHO. But it could be useful to prevent someone from making their bets (on the market’s direction) too large based on discretion alone. None of this is a new idea originating from me and I can say with certainty that I do not have it exactly right. There can be no doubt, however, that this short post is an exhaustive discussion of the subject and is enough to make an informed decision about your finances

Best,

Jim