I wanted to test the performance a month or so after a bad earnings release, which caused at least a 15% fall in the stocks.

Would this be the way to do that?

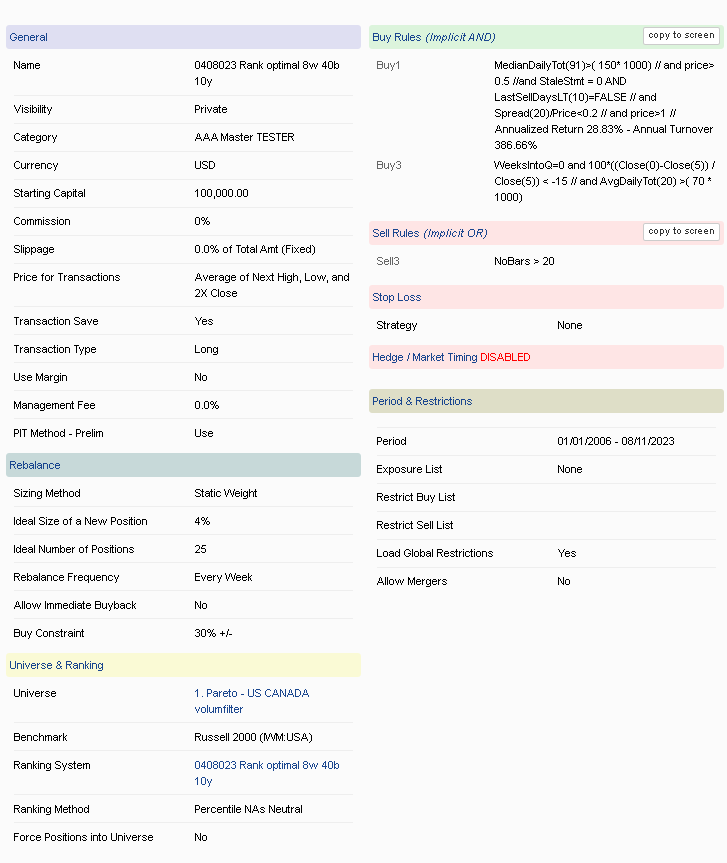

- WeeksIntoQ=0 and 100*((Close(0)-Close(5)) / Close(5)) < -15 //

I wanted to test the performance a month or so after a bad earnings release, which caused at least a 15% fall in the stocks.

Would this be the way to do that?

The Close(0) and the WeeksIntoQ are not linked precisely enough. You could easily end up with a stock that had a 15% fall right before the earnings release.

Try something like this:

100*(close(barssince(latestnewsdate)-4)/close(barssince(latestnewsdate)+1)-1)<-15 and between(barssince(latestnewsdate),5,10)