Here are four models, Best12(USMV)Q1+Q2+Q3+Q4, that have consistently beaten SPY out-of-sample over the last three years. You can’t have them as DMs because I update the universe every 3 months with the holdings of ETF (USMV). (P123 only allows changes every 6 months max.)

The min hold period is specified as 1 year, unless a position makes a big loss. There is no market timing in the models.

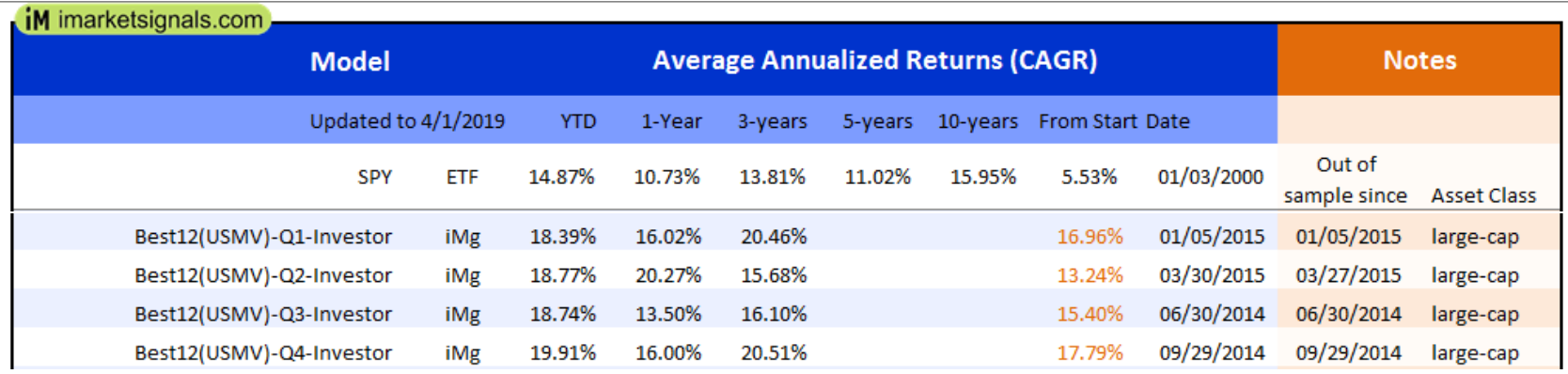

Here is a view-thread from 2 years ago. By now the combo has out-performed SPY by 54% from inception of the first model in July 2014. https://www.portfolio123.com/mvnforum/viewthread_thread,10288#56434

Return of the combination:

YTD = 18.95% (SPY + 4.08%)

1 yr = 16.45% (SPY + 5.72%)

3 yr annualized return = 18.19% (SPY + 4.38%)

This is all done without much trading. Perhaps longer molding periods make more sense.

Georg - I’m not sure exactly what your issue is but can the custom universe call up an InList? The InList can be modified anytime and I don’t believe that the DM module checks on InLists being modified. I could be wrong but I ** think ** I’m right.

Steve,

This is how the model works. My custom universe is called USMV. I update this universe with a new inlist every quarter, which are the holdings of iShares ETF (USMV). I have been doing this since June 2014. I guess a DM would not know whether the universe has changed - so one can update the universe as often as you want, but I assumed that 6 months was the limit for DMs.

I was trying to point out that the ranker has subtleties that should be explained. I didn’t expect that moving a factor into a composite node would make a simulation difference. I thought the results would be identical and they’re not. When there are many NAs, the ranking range become “compressed”. At least, that’s how I think of it. It’s hard to explain which is why I thing P123 should do a write-up.

I’d also like to see articles like those found in the AAII Journal but with added rigor and working code. Maybe even taking the prior subjects and adding code w/ additional commentary. Some examples;

Will Stocks Always Outperform Bonds Over a Multi-Year Period?

Revisiting the “What Works on Wall Street” Screen

Bucket Strategies Underperform Static Allocation Strategies

Momentum Investing the Richard Driehaus Way

Whatever you guys do, please don’t forget about to have a good editor process. Speaking for Millenials everywhere, we will tl;dr anything that’s not to the point.

Georg - I am not sure why P123 had the six-month rule, perhaps to force designers to exhaustively test their releases. But in any case, you have a bona fide reason to update your universe more frequently, and so long as it is explained on the description there shouldn’t be a concern. In any case, changing the contents of a list won’t get flagged. So why don’t you make a DM out of your strategy? You know the old saying, “it’s easier to ask for forgiveness than for permission in the first place”

Walter, of all of your suggestions, I think this one is the best, though I’m not in favor of adding working code. (I also like InmanRoshi’s idea of discussing how to measure earnings growth, with all the different things you should take into account.) The idea behind the blog is not to service existing subscribers (that’s the idea behind the forum) but to attract new ones, and discussing the different treatments of N/A would probably just turn away new visitors. I would like you to post to the forum some of the questions you’ve been asking in this thread–they’re good questions!

We’re hoping to launch the blog within a month with three articles by yours truly, one or more of which might be previously published on Seeking Alpha and/or on my blog, Invest(igations). All blog posts will be published on Seeking Alpha as well (usually a day later) in order to drive viewers there to Portfolio123. We’ll be happy to also publish posts by other members, though I will be editing them so that they’re to the point in order to avoid, as Primus puts it, "tl;dr"s; members will then try to post those articles to Seeking Alpha as well after publication here. All articles will need to refer to Portfolio123 somewhere in the text so that the Seeking Alpha versions actually drive traffic here. My articles tend to be quite long, but I will be breaking them into bits, making use of headings to do so, and occasionally breaking up a long article into several posts (Part I, Part II, etc.) posted on different days.

I’m constantly looking for ideas, so if anyone has ideas for an article that’s not of too technical a nature, please let me know either here on this forum or by e-mailing me at yuval@portfolio123.com.

Ok, I have a better idea of what you want to do. I hope this is part of a sales funnel strategy. Using blogs to collect emails (i.e. leads) for drip campaigns and ‘call to action’ pages is pretty standard marketing practice nowaday but I have yet to see P123 engage like that.

However, I would still like to see blogs on more advanced subjects. The forums don’t work for that. With a light P123 presence, the forums are what members use to discuss issues w/ each other.

Bear in mind that that posts not confined exclusively to Seeking Alpha are not eligible for payment from Seeking Alpha. And exceptions made that allows authors to re-publish a limited portion of the SA article elsewhere and link back to SA for the rest.

If you’re willing to post to SA on a non-exclusive no-payment basis (as I do), this being the first thing on which one needs to click when launching the write-and-article platform, then you have no problem. But anyone taking money from SA, or planning to take money or planning to continue taking money will need to work within these limitations (publish excerpts on p123 and link back to SA or create original work for p123.)

If someone is really adept at utilizing the IB trading algos to minimize friction costs, I would be very interested in that topic. Especially since we can create our own specific order types. Seems like this topic would also lend itself into the new P123 direction, especially for people who aren’t that familiar with IB.