Portfolio123 is going to be starting a blog, and I’d love to hear from you what you’d like to see in it.

I see the blog as giving specific advice about designing stock-picking models; offering more general financial advice such as the stuff you see on Financial Samurai; commenting on recently published research; and covering a range of other topics, including transaction costs, mistakes beginning investors make, and when to sell your holdings.

To start with, I have a backlog of close to fifty articles that I’ve written for Seeking Alpha and my own blog, Invest(igations), some of which I’m going to be revising and repurposing. The same is true for some of the articles Marc Gerstein has written for his blog, Actiquant. We’re planning to post an average of two new articles every week, and I’d welcome articles written by P123 users. These will, of course, be edited by yours truly.

The idea is to make Portfolio123 a destination for people who care about stock analysis, backtesting, financial data, asset allocation, and portfolio management. I’d like to see people visit the site every few days to see what’s new, and, ideally, to get some of the posts linked on Abnormal Returns. I feel certain that this will increase the number of subscribers to the site.

If you have any suggestions for articles or thoughts about the direction the blog should take, or if you are interested in contributing, please comment below or contact me at yuval@portfolio123.com.

We’re hoping to launch the blog within a month. Stay tuned . . .

Great move! I’m going to make several posts so the ideas don’t get lost.

How about a post on the effective use of the Ranking Reverse Engineer tool? A working example would be great. I think this feature has generated questions before but never really answered.

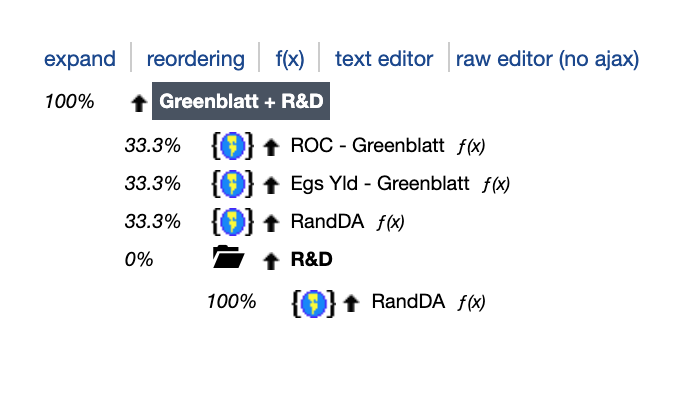

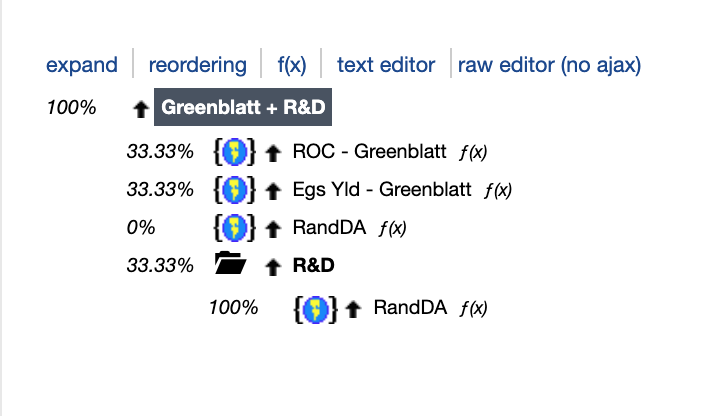

Expand the “Ranking System Computations” doc to explain why factors that have a large number of NAs return different simulation results when moved into a composite node.

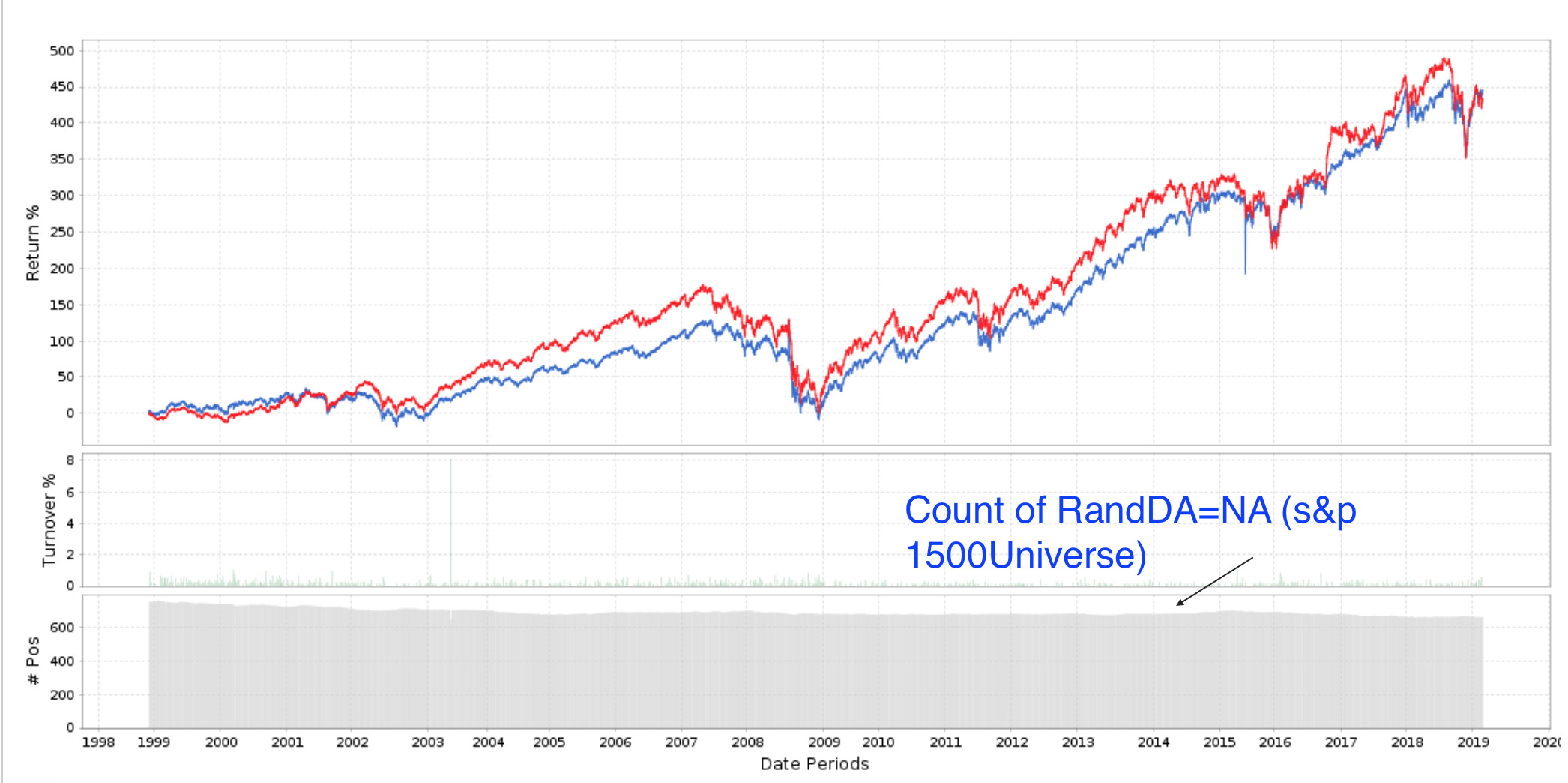

I ran into this recently with RandDA. For the S&P 1500 universe, approximately 40% of the stocks report this factor as NA. The initial ranking system had RandDA at the top-level. Later I moved it into an otherwise empty composite node. Naively, I expected the sim (w/ neutral NA setting) to return the same result. It did not.

Some pics attached w/o description. If you want a example case, I have it.

For new members, a post about how Strategies differ from Screens could be helpful. I would answer questions like, why is there even a screener? Why do its results sometimes differ from that of a similar strategy (for small-cap stocks, the different slippage models contribute to that, but there’s probably more). For what activities is the screener the preferred tool? I know how my use of the Screener has evolved, maybe P123 could help new members with that process.

The reverse engineering development has stopped long ago. It is meant to tell you which factors ranks correlated the most with best or worst performing stocks. But it does so in a clumsy way . It was put together quickly, using existing components, and it is very hard to use. It needs an overhaul before it’s talked about in the blog.

How to make effective of use CompleteStmt, StaleStmt, QtrComplete to avoid stale data.

In the past, I just used StaleStmt, but because CompleteStmt is tied to the NA fallback mechanism, I’ve started to use both CompleteStmt and StaleStmt. Is that proper? What’s the use case for QtrComplete?

A lot could be written about NA handling, too. When testing factors in the buy/sell rules, I now wrap the tests in IsNA(). I also sometimes do that in Ranking. Is that the best practice? Let me know with a blog post!

Demonstrate how P123’s Series tool can be used to replicate and expand on ideas reported in the financial press.

For example, I’ve been reading more stories lately about how analysts are still making downward EPS revision. With the Series tool, that data could easily be replicated. In addition, the analysis could be expanded to include revisions within a sector, or a market cap segment.

The Series tool can provide market insights not found anywhere else.

I’d suggest figuring out a way to publish the work that InspectorSector did on his website, while it was active. I would have never figured out the optimizer

(and many other tings) without his posts.

“If you have any suggestions for articles or thoughts about the direction the blog should take, or if you are interested in contributing, please comment below”

Yuval - I enjoy reading your articles and also Marc’s. I look forward to your blog!

I have one comment… Marc has been mentioning the possibility of introducing “channels” at P123 for several years but nothing has come of it. I assume that “channels” means that individual members can establish a presence at P123, helping them market their DMs, or attract private consulting or training. Are “channels” still a possibility, and what form might it take?

I have recently been looking into Youtube “channels” as a possible platform for providing videos on such things as system (model) development and novel ideas by way of videos. Also, tools training if there is enough interest. It seems like a plausible way of drawing new subscribers into P123 (and for myself affiliate income). I am a complete novice when it comes to video creation but it appears that Youtube has some pretty good video creation/editing tools. It would be really nifty if Youtube could be coupled into P123 by some means. Perhaps P123 could open up a Youtube channel and provide the means for subchannels by individuals. This could be integrated/embedded within P123. It ‘could’ present new opportunities for guys like me who struggle to earn an income in this industry, while equally benefiting P123.

A combination of broader stock picking criteria theory (like yuval’s blog) combined with P123 syntax lessons. I think one area that could be useful to a broader audience is more P123 specific advanced syntax related instructional topics, particularly towards people who don’t have programming or accounting backgrounds. Users and P123 staff have written and shared some really elegant P123 forumulaes on the forum, it would be nice to move those to the forefront and really breakdown what they do. Sometimes the syntax/function reference documentation is a little dry and hard for me to follow without looking at a real world application example at how it’s practically used and what it’s trying to accomplish and what parameters to pass into it. P123 has essentially developed its own programming language without the corresponding O"Reilly’s or “…For Dummies” reference guidebook to go along with it. Questions about things like how to loop through previous periods seem to be common on the board.

I agree with the suggestion of exploring deeper into some of P123’s non screen-rank-sim based tools like time series and optimizer and rolling tests. One thing I often enjoy on the forum is when people are discussing current market predictions (usually in the middle a downturn) and start showing the really cool things they’re doing with macro charts and how it’s reflecting on current market conditions. Even if I have no idea or willingness to attempt to make money off of it, it’s interesting and evergreen material.

Will some of the people who visit Financial Samurai and come here for general financial advice believe the efficient market theory? If so, they will probably head over to Vanguard for their ETFs.

If you want them to stay and use a port (a designer’s or their own) you will want to present anything that makes a good argument that the market is not efficient.

This was behind my posts in a recent thread discussing the failure of many DMs to attract subscribers. I wrote about why I thought things had not worked out. I acknowledged that there were things p123 could have done better, but I also expressed (and not for the first time) how I thought designers had to raise their games in terms of establishing public marketable personas, voices. Unfortunately, that went over like a lead balloon. Nobody jumped in to discuss that — not to agree, not to disagree, not to seek clarification, nothing.

In my opinion, the idea of channels would have no chance of success unless participants are willing to engage those kinds of issues in a substantial way. So as of now, I don’t feel able to elaborate or advocate the idea within p123. And also for this reason, I’ve been keeping quiet in terms of ideas to improve DMs, something that’s been sitting on a to-discuss list for Marco and I.

But maybe broader participation in a new p123 blog area might induce members of the p123 community to start thinking along these lines. So I would not say the idea is dead. Perhaps the blog can give it the sort of kick start I have not been able to give it in the forums.

“DMs to attract subscribers. I wrote about why I thought things had not worked out.”

Marc - I can think of at least a dozen things that could be improved with DMs. When I get the time, I’ll write out my list and send it to you privately.

I looked carefully at the overall performance of the DMs a few months back, and it appeared to be exactly what you would expect if the market were efficient. Only a tiny fraction had beaten the market over 2 years. Maybe those models will continue to beat the market, or maybe it was just luck.

Dodge - the DM environment is suffering from “Ready-to-go” hangover. The issues that allowed designers to go nuts selling snake oil were corrected with DM, but the remnants of the disease were not purged.

Blog is fine, a Podcast or a Interview Video

or Video Presentations with members that give answers to their history in the markets and how they use P123 in order to kill it would be a killer!

Next year I will turn pro (100% TradeInvesting, I will be happy to provide Content (Videos, Podcasts, interviews!) for free!

Regards

Andreas

Timing or not being fully invested in the market all of the time is part of the problem!!!

I looked at the excess returns for the last 2 years for the designer models.

Those models that were invested less than 95% performed 5% worse than the ones that were invested 95% or greater.

The reasons for this are obvious. Market timing is more easily overfit and when wrong it is likely to be harmful. For those models that are not trying to time the market (e.g., just not enough stocks meeting the criteria) then it is a simple matter of opportunity cost (economics 101).

This should be looked at more closely and if confirmed then any Model that is not nearly 100% invested should be separated from the others. Probably with a warning.

If an aggregated set of models can be found to beat their benchmarks by 5% then P123 will have something to be proud of and to advertise. Looking at this may help get you there. At least you would not be starting 5% behind.

Saying the sky is blue doesn’t entail that that all air molecules in the sky themselves are blue. It applies to the sky as a whole. (This is an allegory)

Also, the percent invested would reflect itself in the portfolio’s alphas. So the argument that leverage is the reason for underperformance is not valid unless portfolios outperformed on some (any?!) risk adjusted measure.

The bottom line is that investors only want alpha and/or efficiency. Prove me wrong.

What simple metrics would you use to see if P123 is delivering a suite of useful Designer Models?

I think averaging the Alphas has the some of the same problems as the average of the excess returns. Is that the metric you would use?

I think you cannot average the Sharpe Ratio but could consider the median—it would give some information. The mean does not work for a host of reasons. However, I generally prefer the Sharpe Ratio to Alpha when looking at single models (could be just me).

But whatever metric you would use it remains to be seen whether market timing models add or subtract from P123’s offerings other than we know that they subtract from the average excess returns.

I guess my answer (for now) would be that they would have to be looked at separately were P123 to try to come up with an overall metric. And then I would still use excess returns on the models that are fully invested all of the time. For the models with market timing you would have to look at the absolute returns or the returns relative to the risk free interest rate.

If you prefer Alpha I am fine with that.

I think you have a point about the problems of grouping them together whatever metric is used. Which is not so different than my original point: they should be separated. But maybe without the warning (if you think the timing may actually be valid).