Microcaps have been capable of lagging for decades at a time during the 20th century.

One possibility is that decadal (de)conglomeration fads are at the core of the microcap vs large cap performance differential. I find this plausible since fads actually do drive investor behavior.

You know bridgeway capital? Its BRUSX fund (bridgeway ultra small company fund) was the best performing fund for a long period, focusing on very small value stocks. Same with Fidelity Low Price stock fund (FLPSX) run by Joel Tillignhast which was also one of the best performing mutual funds for quite a long time. These had amazing historical track records, even just a few years ago. Now look at them. The are getting crushed by the S&P 500.

I’m not quite sure what to make of it. My guess is a lot of people using this site are suffering big time because all the historical backtesting would show that small undervalued and quality companies outperform. They did, no doubt. Up until about last year. I’m quite frustrated with it, but i’m not changing. What am I going to invest in otherwise? Momentum stocks? lol that is the quite the dumbest strategy i’ve ever heard. Let me tell you these folks are going to be burned eventually just like all the bitcoin/beyond meat/netflix investors. What else, treasuries? lol inflation adjusted 0% returns, no thanks. S&P 500? That has been going up to no end. You’ve got these ultra big stalwarts that seemingly never go down. They will. I just can’t pull myself to buy a fund the weights expensive stocks more than cheaper stocks.

Tell you what. I’m going to keep buying these companies that are quality and undervalued and unloved. I don’t care if they go to 10 cents, i’m just going to keep buying them. I may be wrong, but if thats the case, we are going to have MUCH bigger things to worry about if all these non S&P100 companies all disappear.

If small/microcaps underperformance are the canary in the coalmine for risk off sentiment (not unlike an inverted yield curve), it seems to fall in line with continued pessimism for future earnings. People are preparing for pain.

The past is never a reference for the present or the future. If it was, there would be no evolution and no development.

The economy and capital allocations have changed in big ways over the last 40 years. Banks and pension funds hold much more capital than before and their preference is investment in large blue chips.

I am sure that they looked at mergers and acquisitions but this was not address in the article (or I missed it).

Seems this would affect the numbers with the good (small) companies disappearing—along with their profits. Or often the companies are bought before there is much profit—skewing the results in another way (maybe).

The profits of the small companies would then move to the big companies then wouldn’t they?

Who thinks a small drug company with a great new drug will still be here in even 3 years. Could be a good stock to buy before the merger.

Again, I am sure they thought of this. I wish I knew whether they found it to be a significant factor.

A lot of what they say relates one way or another to scale, which is standard stuff. I’m quite surprised though that the authors did not consider the spectacular and obvious impact of M&A.

Seems like they determined at the outset to conclude that investment in intangibles is where its at (a nice HBR-ish theme) and molded the data to fit the conclusions. Nut even with R&D, they don’t see, to have dug below the surface. If that’s the key to growth, then why is big pharma struggling? You can’t divorce R&D spending and productivity from the nature of the technological life cycles in different areas. Pharma seems to have shifted and it looks like the new paradigm will be in the biotech-genetic areas, so there, the mega caps of the next generation may more likely be today’s small companies rather than the Pfizers of the world . . . Unless the M&A folks stir the pot.I’m sure there are many p123 users involved in scientific areas who could speak a lot more eloquently on this angle.

There’s also the pace of technological development. It’s a lot faster today than it used to be, meaning the UBERs of the world don’t need to spend a lot of time as micro caps, small caps, mid caps, and then large caps. They go through all the stages, but some are so fast, they barely get noticed and are over and done with before the company even goes into the public markets.

There are also a lot more crappy small companies today; as I said in a prior post, it’s easy for lousy companies to get capital. When it’s harder to get capital, companies need more talent and better ideas than many have today.

I also think the HBR folks underestimate the impact of large firm bureaucracy. It’s there. But some companies are more talented than others at controlling it and speed/momentum/M&A helps them continue to run.

‘THE PUTS HAVE EXPIRED’: Morgan Stanley warns that neither trade nor the Fed can save them now

“We think many have been misinterpreting the signals from the market to be a bullish signal for growth when in fact the market has been signaling since April that growth was likely to disappoint,” Wilson writes.

“The S&P 500 is the most defensive, highest quality and liquid stock market in the world, so if it is outperforming strongly, it is likely a bad sign for future growth. The dramatic underperformance of the small cap Russell 2000 and cyclical sectors all year was a clear indication that things were not improving, nor were they likely to this year.”

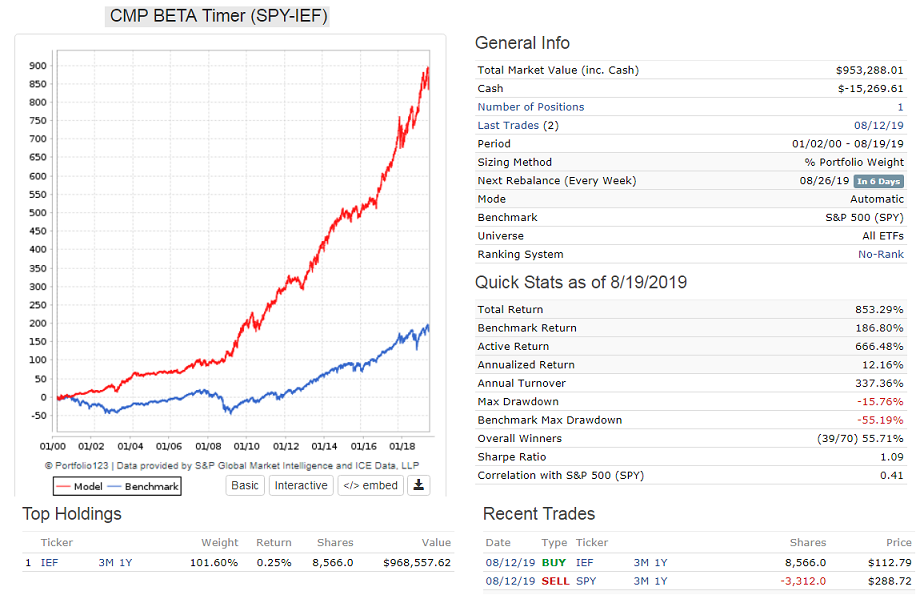

This indicator was brought to our attention by Andreas Himmelreich (judgetrade) who noticed that it correlated well with his 5-stock portfolios, e.g. when high beta stocks were doing well, his portfolios went up in value, and otherwise it under-performed. Subsequently Steve Auger (InspectorSector) provided an algorithm to model this on Portfolio 123. This is all on the Forum.

Michael Burry, of The Big Short fame, thinks there is a “bubble” in passive investing and ETFs that skews towards large cap companies and small value cap companies are being neglected.

Yeah, its been trending that way for a while now. Its part of my explanation for why small value and foreign stocks are getting hammered. Hasn’t yet reversed course though. It will in time.