Set offset periods and length of each run. Great for models with very loose selling rules or perhaps even those with none at all. You can monitor performance over 5 years (and rolling periods) for buy and hold strategies based on your initial buy criteria.

I use it because my sell rules are often looser than my buy rules (unlike the screener). And different start dates can mean different holdings even though there is time overlap. e.g. if you buy on one week reversion and then hold for 6 months, you portfolio offset of 1 week will have every portfolio with very dissimilar holdings despite time period overlap.

My frustration wasn’t directed at you. Just how hard it is to ‘hit the next level’. You’d think that providing free models, offering free work and having years of out-of-sample work and clients vouching for you would be enough to have someone give you a shot for half the wages of the guy who cleans their office toilet. But not so. Just re-thinking what’s really the best strategy here. So far it seems that swirling the toilet wand provides a steadier return with very defensive properties that has low correlation to momentum and value factors (but positively correlated to the # of office workers with IBS).

Kurtis, have you ever thought about getting a certified financial planner degree? and just doing modelling on the side? CFPs always seem to be in demand and it might be easier to break into on the retail side than the institutional side.

When I was taking a graduate level finacne class recently, the instuctor was trying to encourage everyone to get a CFA, but the students themselves said it was an awful amount of work and testing with an unsure payoff. But the CFP was faster out of the shoot.

I started down the CFP route but decided that at my age it would take too long to build up a business. But younger folk could have a good run at it.

The really big incomes always seems to revolve around managing other peoples money directly. And not working for someone who is the ‘front guy’ (who is usually, as Buffett says, more salesman than anything else).

I did take the Canadian Securities course. There are some add-on’s if you want to be a Financial Advisor or such. However, I really don’t have interest in that. I love research and model development and over the years I have had some really good gigs. The goal is to bury my head in the data and keep designing and doing research.

I am actually in Indonesia right now. Previously spent 2.5 years in Malawi Africa. Remote work developing models helps me do that. Really wish WorldQuant would pay at least one-fifth the going rate for quants but they hire 1,000 quants to manage 5 billion. And there are many layers of PMs and staff above them. A real shame that they are hiring an army and paying them so little.

Anyway, this discussion got kind of derailed. It’s time to clean the toilets again.

Isn’t one of the critiques of the current state of capitalism that most of the wealth is going to the top? That would partly be reflected in the largest companies accruing most of the wealth. If true that could explain a weakening small cap premium.

I think that some of us are conflating two issues:

The size risk premium

The size-inefficiency relationship

While both of these are related to size and returns, they have very different implications. The first says that investors can earn a risk premium by agnostically holding small companies. The latter says that there is greater opportunity in small cap stocks, but not necessarily a latent risk premium.

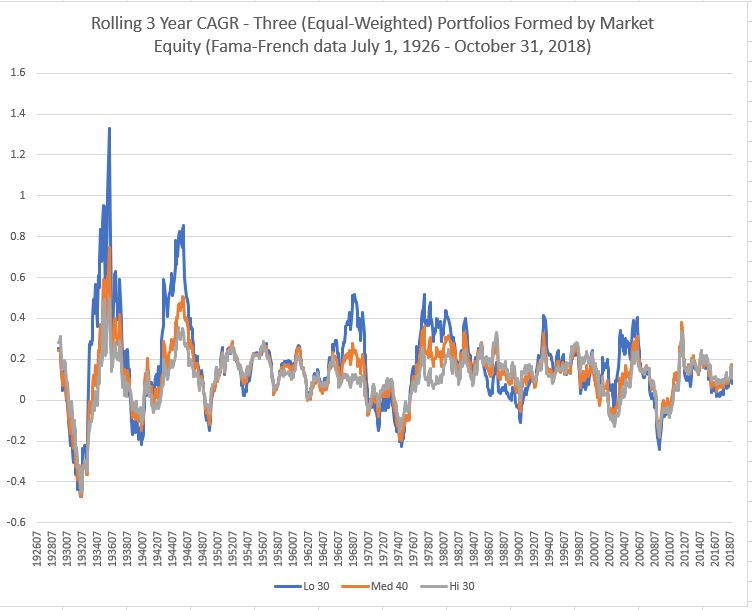

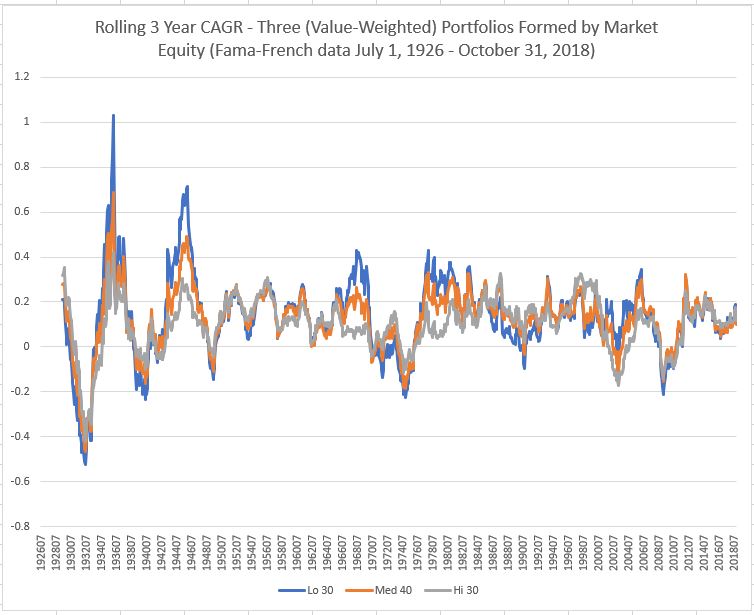

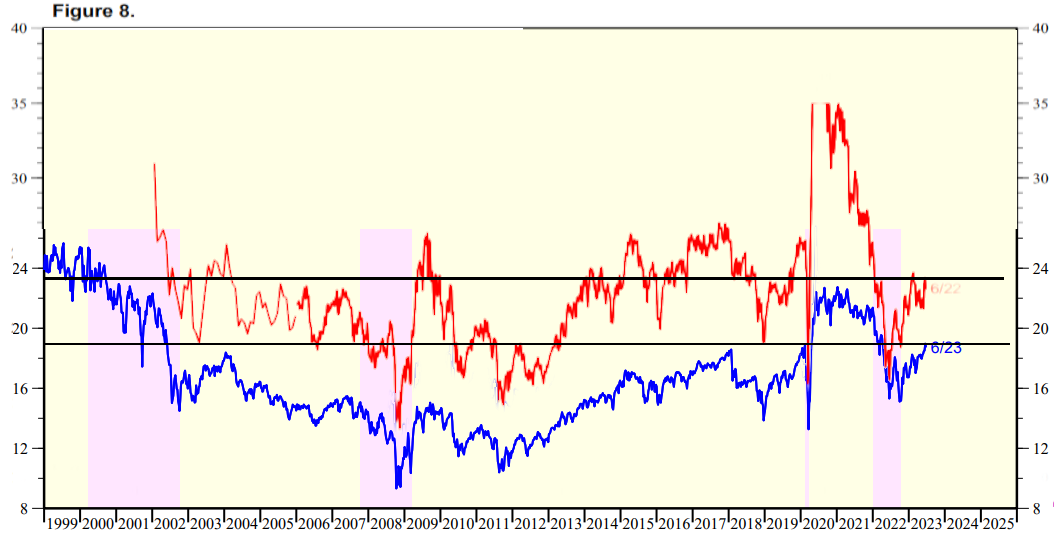

But let’s bring some data to the discussion. This is an analysis of the size premium based on Fama-French data:

Revisiting the above graphs, the most prominent feature is that small has significantly outperformed big in only five distinct time intervals since 1926:

Mid 1930s

Early to mid 1940s

Mid to late 1960s

Mid 1970s to early 1980s

Early to mid 1990s

This I think begs a reversal of the question, “is the small cap premium dead?”

Here is an interesting read that uses an adjusted way to calculate size and addresses critisisms of the size premium. They conclude it’s not dead if you calculate size correctly. Worth a look. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3275366

Aswath Damodaran thinks it is “fiction”

He notes that it doesn’t appear in other countries. Maybe it is only in the US markets because US dominated the 20th century and US small caps killed it. What happened to Argentinian small caps? I think the word for that is survivorship bias.

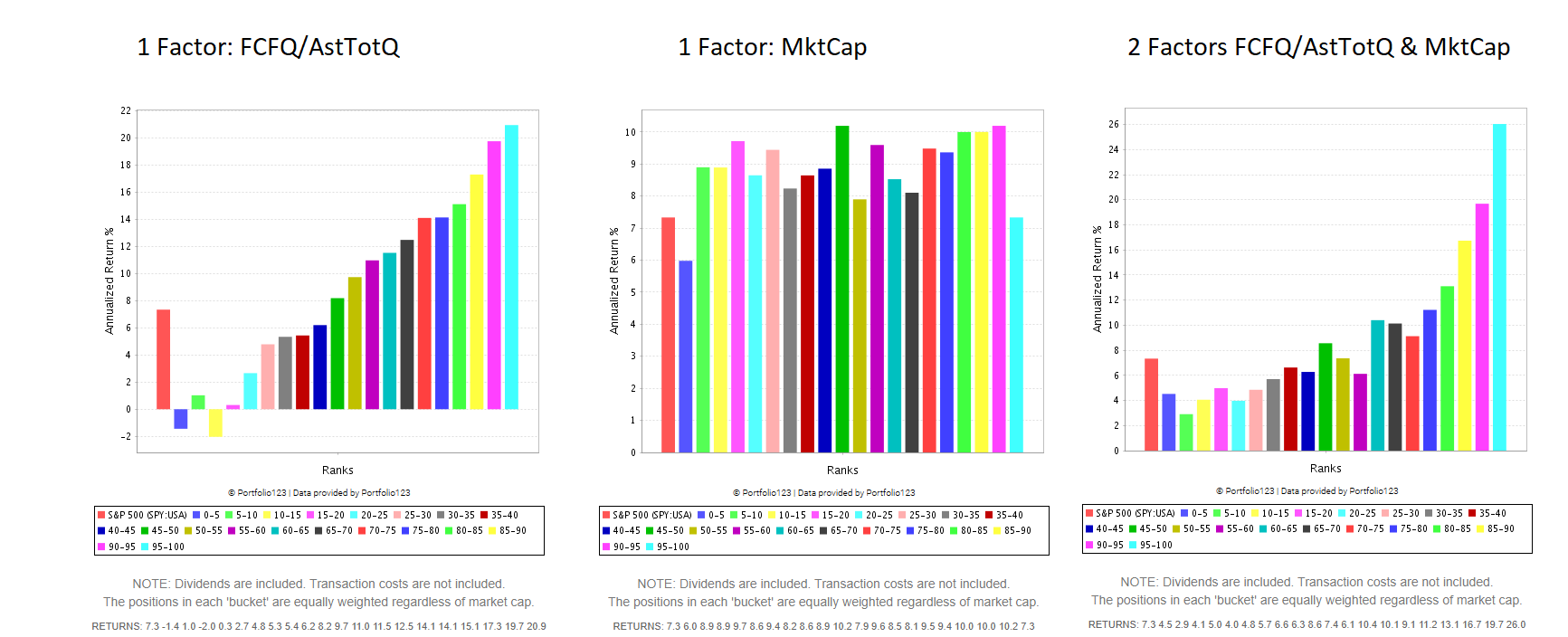

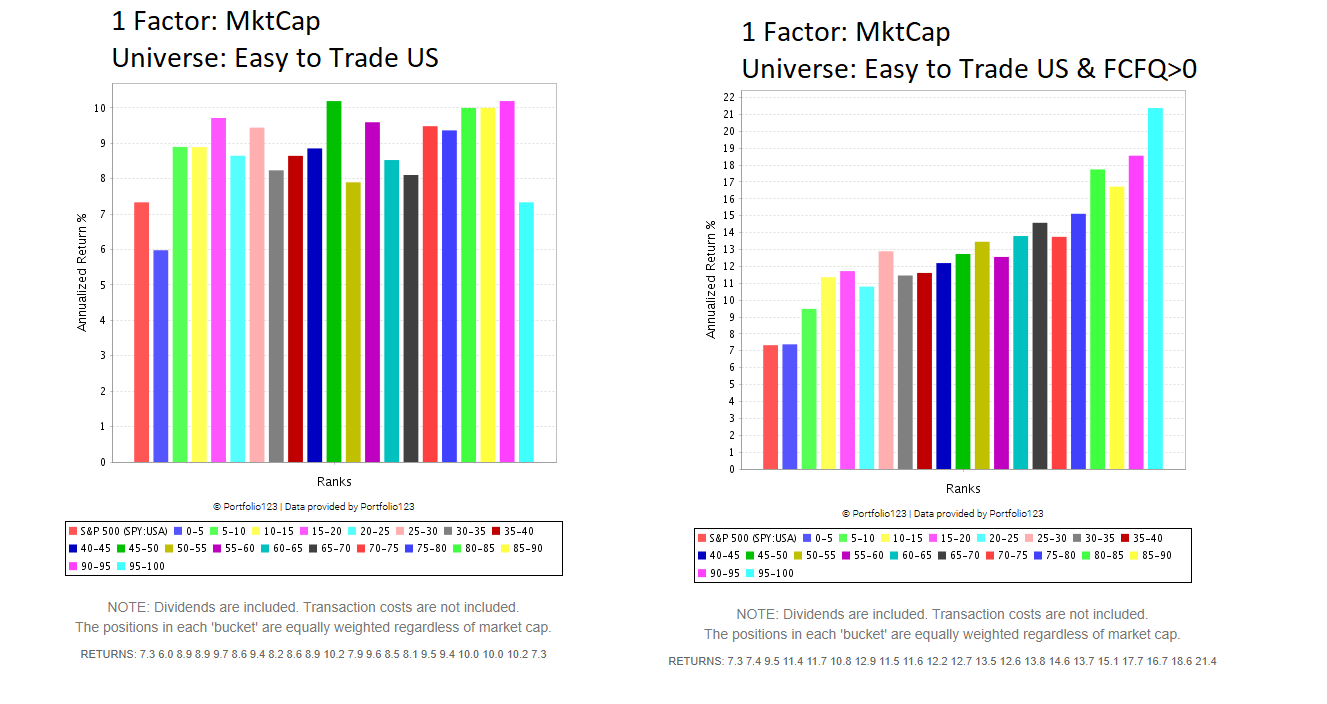

I find a very strong size or liquidity premium once you remove ‘low quality information’ stocks. I researched this primarily because of this forum and hopefully it will add another perspective to the topic. Similar to the idea of ‘Quality Minus Junk’ but attacked from a very different angle. And I find that the size premium is present in this sub-universe even between cap ranges of $1mm and $1B. It should be on Seeking Alpha in the next day or so. It will likely get a lot of opposing voices but that’s okay. Just a viewpoint.

I wanted to revive this topic and saw that this forum thread had some very good discussions.

It has been a few years since the debate, but has anyone given any thought to why academic studies often agree that the small cap premium is very small, but here on p123, it is often the small and microcap strategies (Model portfolios) that seem to be the best?

Is it only because we do not use the size effect as a standalone, but together with the other factors, and that the factors tend to make it better in the small and microcap segments?

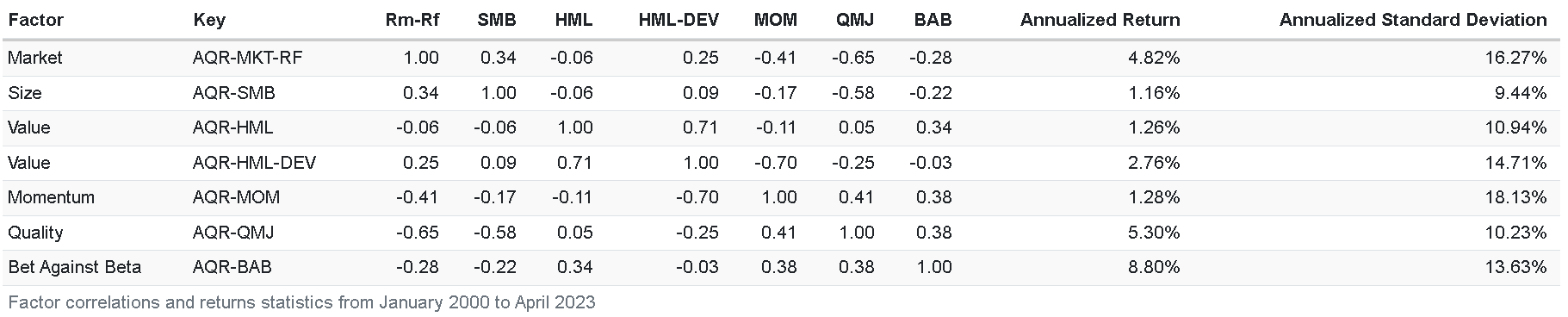

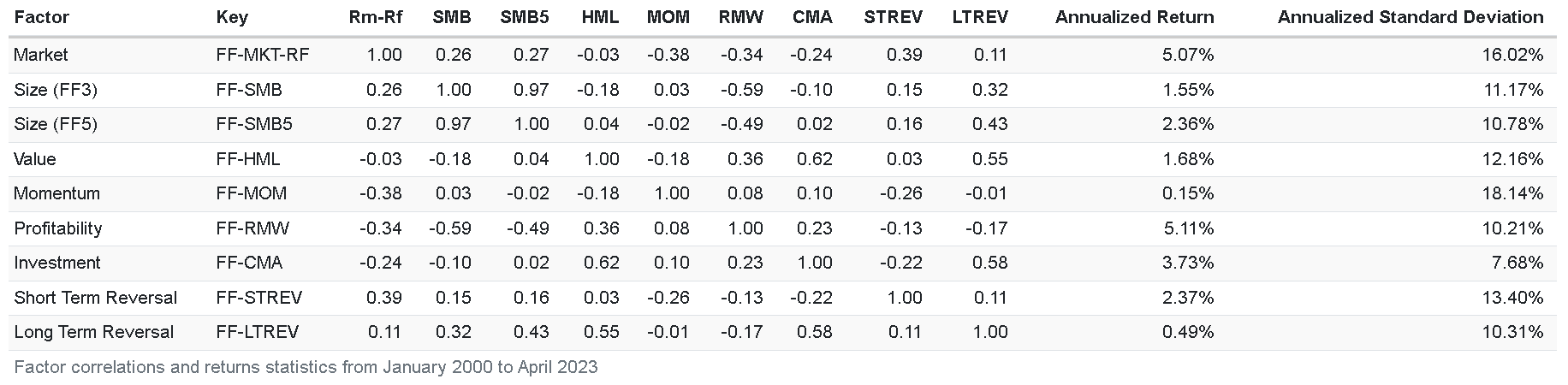

Here are the returns on the various factors over the past 20 years, measured with the AQR F&F and Alpha A databases:

As James O’Shaughnessy noted in What Works on Wall Street many years ago, small caps are much more sensitive to value, quality, and growth factors than large caps are. So it’s easier to design strategies that outperform using small caps than using large caps. Conversely, it’s easier to design short strategies, or strategies that underperform, using small caps than using large caps. O’Shaughnessy has a good discussion of exactly why this is so. I wrote an article about the phenomenon way back in 2017: Why I Invest In Microcaps | Seeking Alpha

I think they should separate profitable from unprofitable small and microcaps. Unprofitable ones with very young companies are more like gold stocks or bio-tech in my opinion. Lots of narrative and story telling but so many unknowns that it is more like rolling the dice. Once they make a sub-category of this, I think the story would be much different.

The S&P 600 small cap index beat the Russell 2000 small cap index (^RUT). It also beat the S&P 500 large cap index (^GSPC).

The large cap index took seven years to recover from dot com bubble popping. Small cap indexes avoid bubbles, almost by definition, and tend to me more volatile but with quicker recoveries (4 years is practically a worst case scenario for small caps).

I can confirm the previous posts that the small cap factor positively interacts with other factors, esp. with profitability and other quality metrics and that it is hard to capture the small cap factor without any other factors. It is well described in the book “Your Complete Guide to Factor-Based Investing: The Way Smart Money Invests Today”, which is quite cheap and which I can recommend.

When I analyse a factor in a ranking system, I usually add a small cap factor in order to see, if there is a positive influence. Example:

You can find similar differences, if you use a small cap universe and applying a ranking there (but I personally do not like to cut away large caps - to remove non-profitable stocks seems more logical to me and this leads also to a more “static” universe, which has less turnover/slippage in a Strategy).

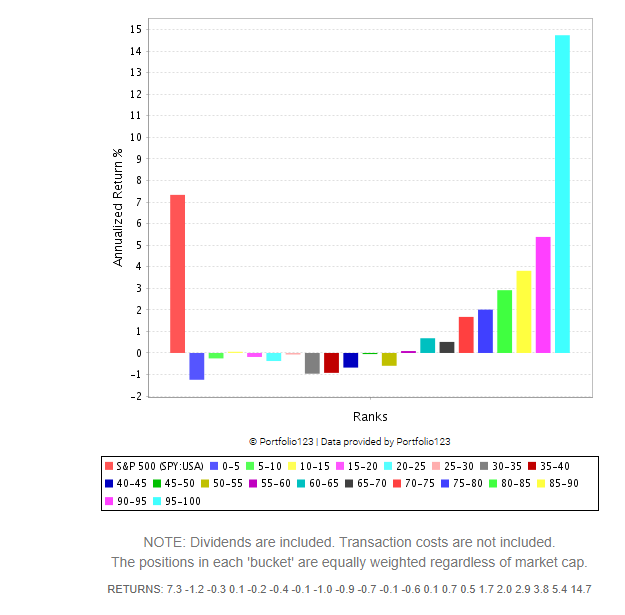

Other approaches to find the small caps are more sophisticated. For example it is well known that small caps outperform during bull runs: So you could use sth. like a market timing formula like (I don’t recommend to use this formula by its own, because most of the time the ranking is “inactive”):

eval(close(0,getSeries(“RSP:USA”)) > highVal(60, 0, getSeries(“RSP:USA”))*0.99, MktCap, NA)

(you can use also other treshholds)

Resulting in a ranking backtest, where the smallest stocks outperform all other:

I think this related to what @yuvaltaylor calls augmenting factors and what you described here are examples of procedures of finding these augmenting factors.

I’ve had some succes using a similar factor using the high yield spread as pointed out here: Crisis Investing - #4 by RTNL. Basically it is the same but instead of RSP:USA, ##CORPBBOAS and a minimum treshhold for the high yield spread (>5). Gives similar resuts.