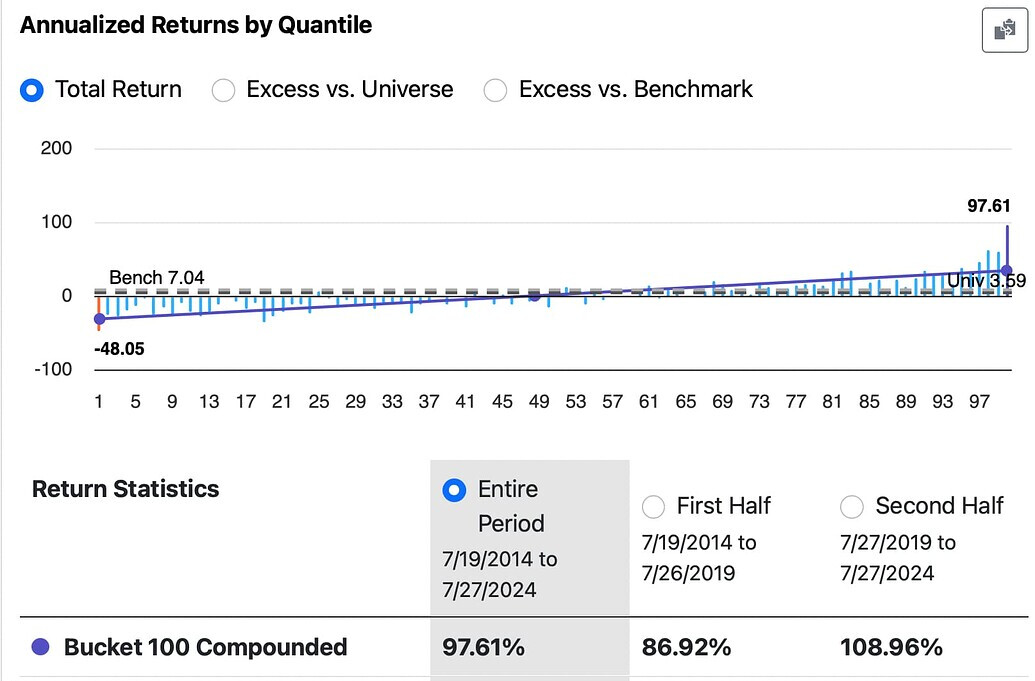

Are these out of sample returns? The 97.61% return by @Jrinne ?

Not sure where you are getting 97.61% but everything above is a validation set with a proper gap.

There can be lookahead bias with the features and overfitting with multiple validation trials. Some of that can be mitigated but I made few efforts to do that with the above.

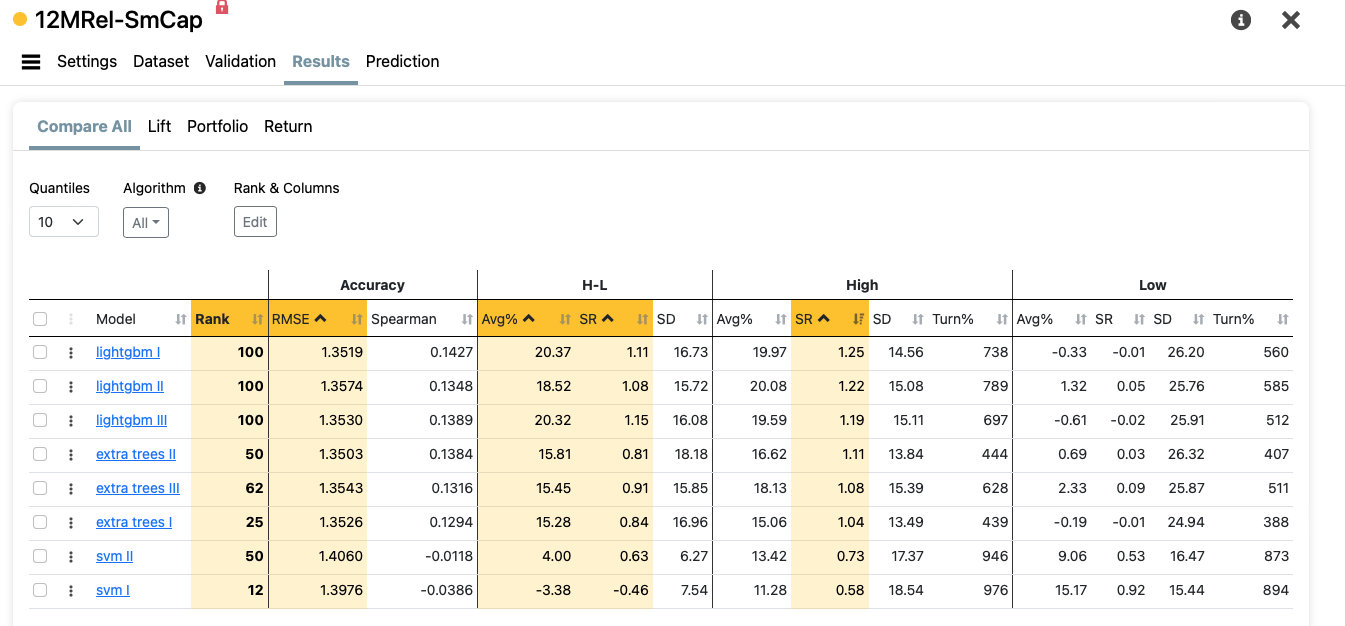

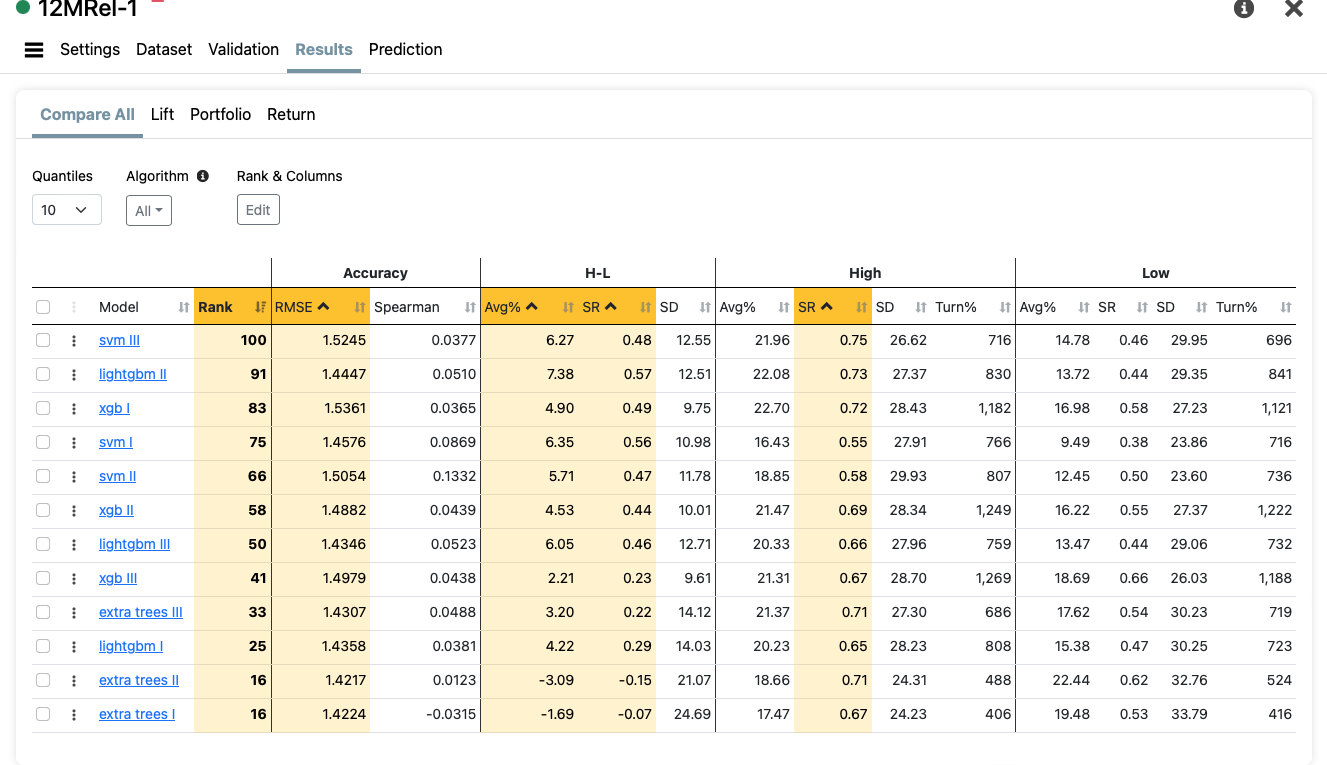

Thanks I see what you mean lightgbm does do well-- Small Caps...

Large Caps maybe I have to still play with it... both ran on timeseries...

This chart you posted - shows 97.61% return annually I think correct? (I guess 100 buckets is kinda a lot though - top bucket maybe less reliable?)

"Optimizes to a relatively low turnover (Trading System screenshot for sell rule). Because of slippage I assume. Decline from performance results of the AI model with no slippage would also suggest slippage is important, I think"

Okay. Yes. That is time-series validation for the Russell micro-cap universe with no slippage. Yes, these are validation sample results as provided by P123.

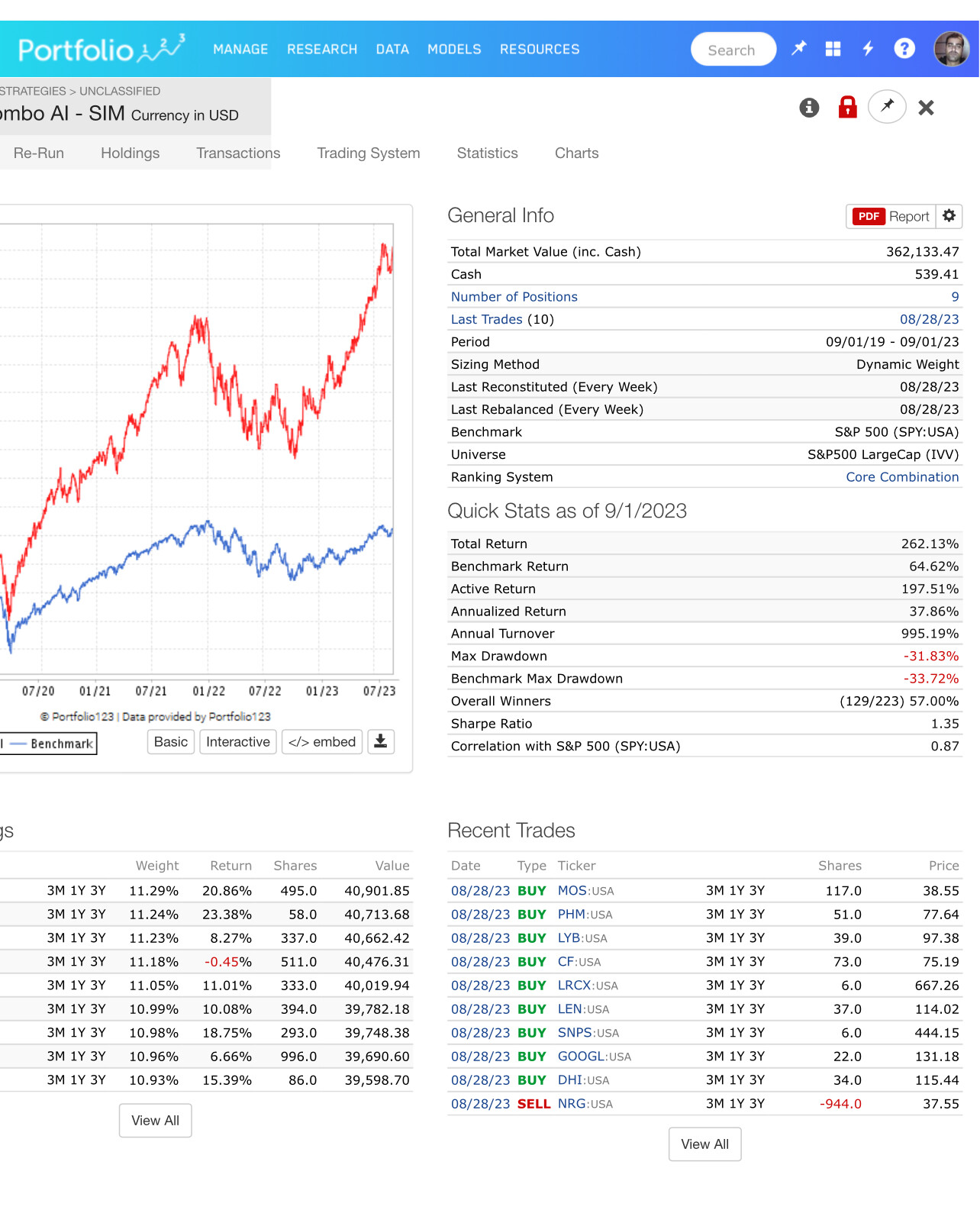

@33.66% annualized return in a sim with variable slippage I think. Makes me want to makes sure I understand the universe when I see a performance test. First time I did anything with that universe. I am not sure trading that universe is for me so forgot about that. ![]()

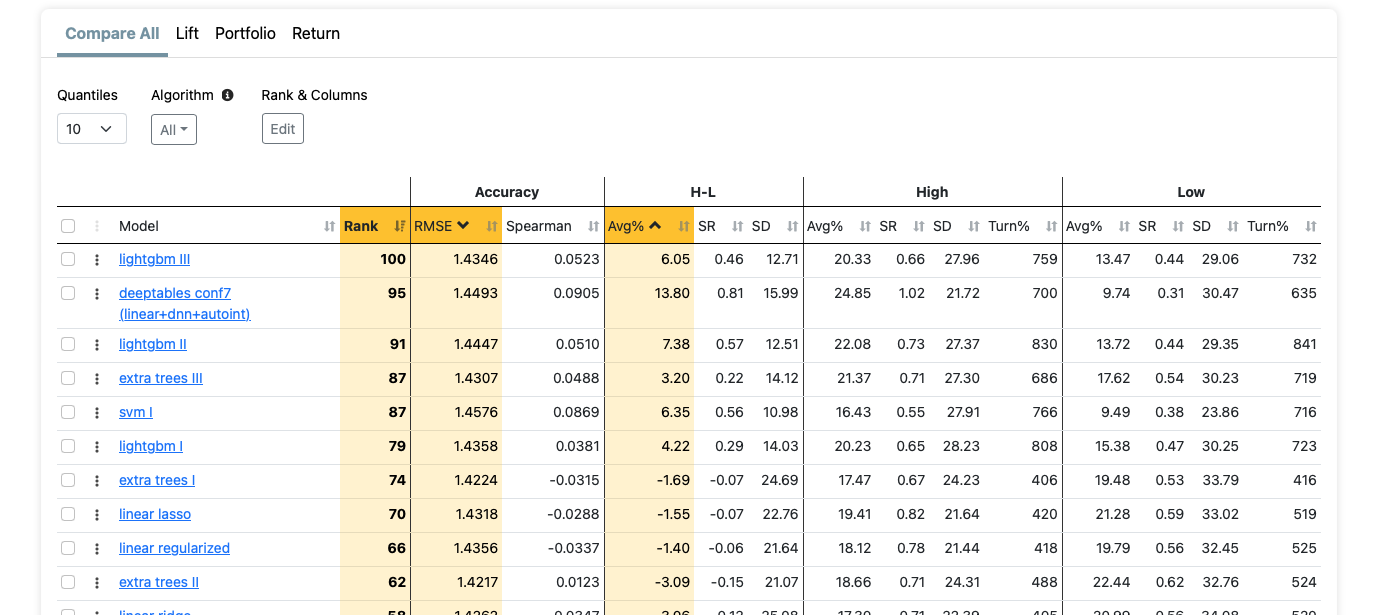

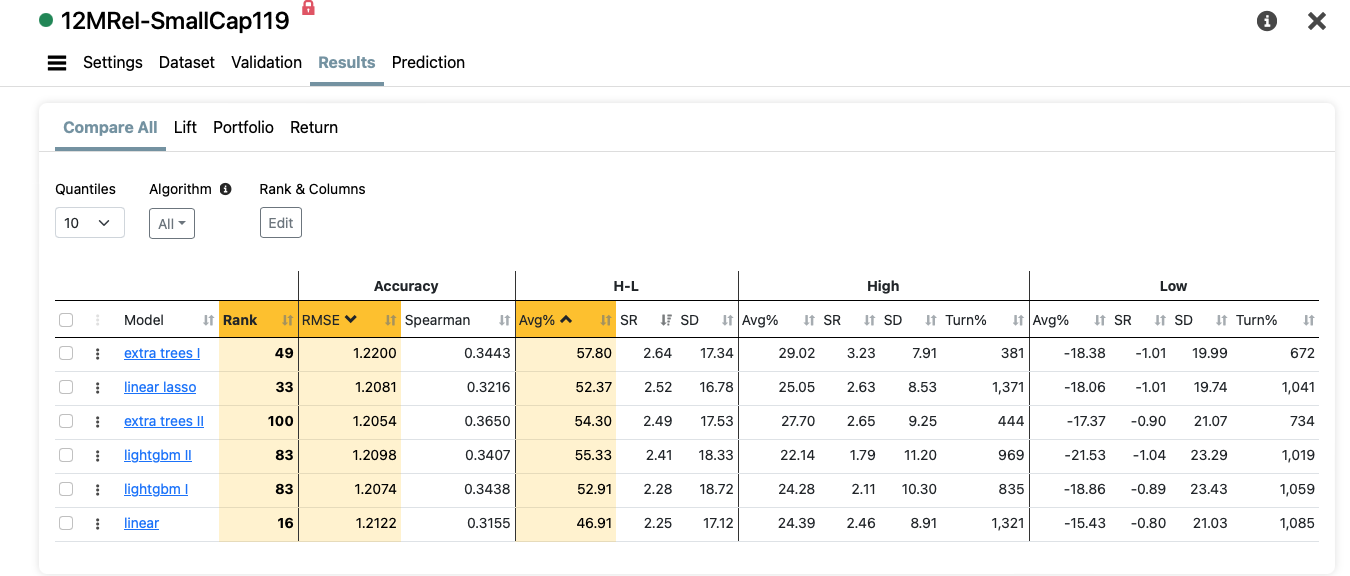

Linear models are better in large caps. Also, low RMSE is good.

I wanted to share my results with large caps(Sp 500 large caps IVV)... these results aren't bad especially with a 1 year lookback for the sim, but going back 5 years the return drops to about 25-28% / year.

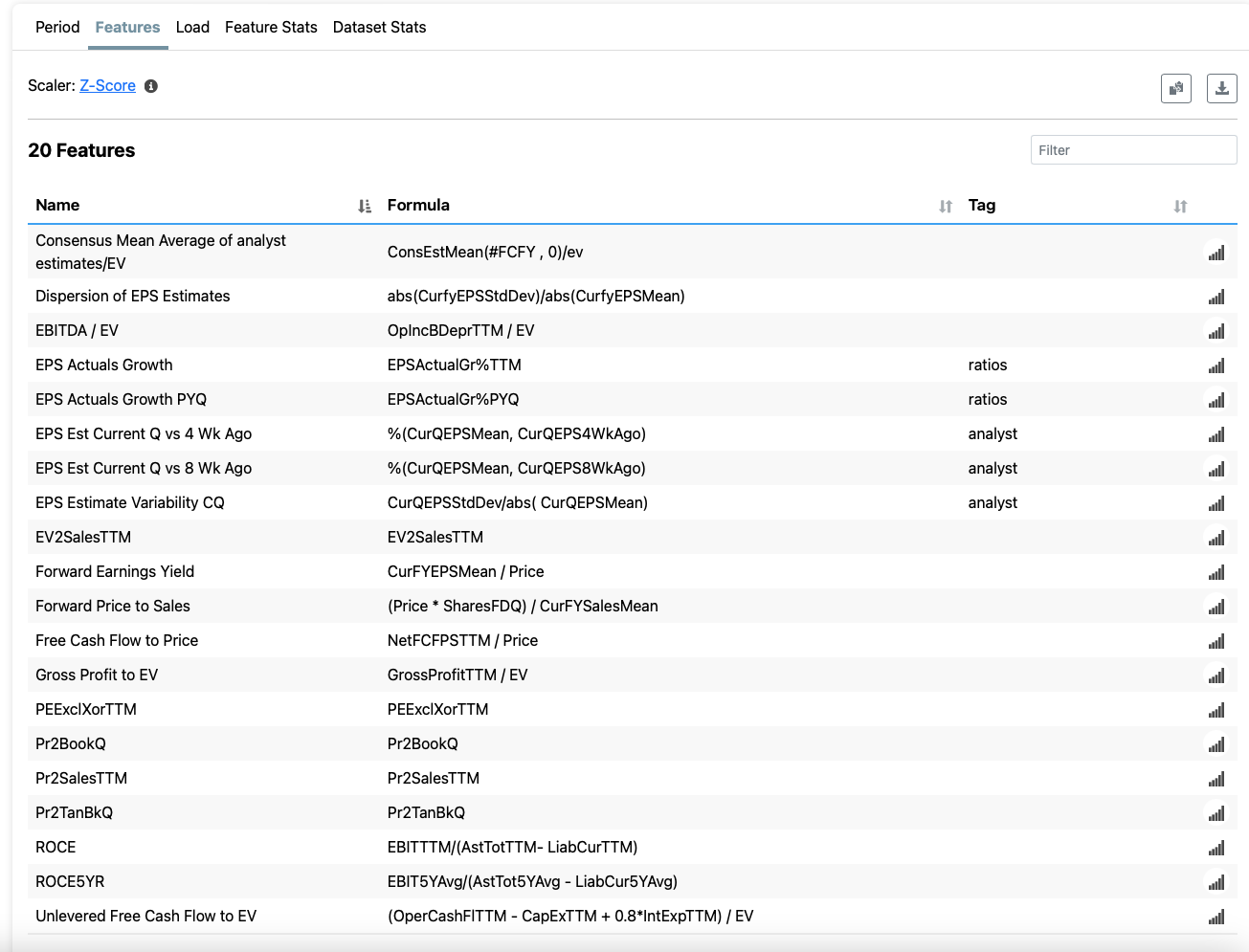

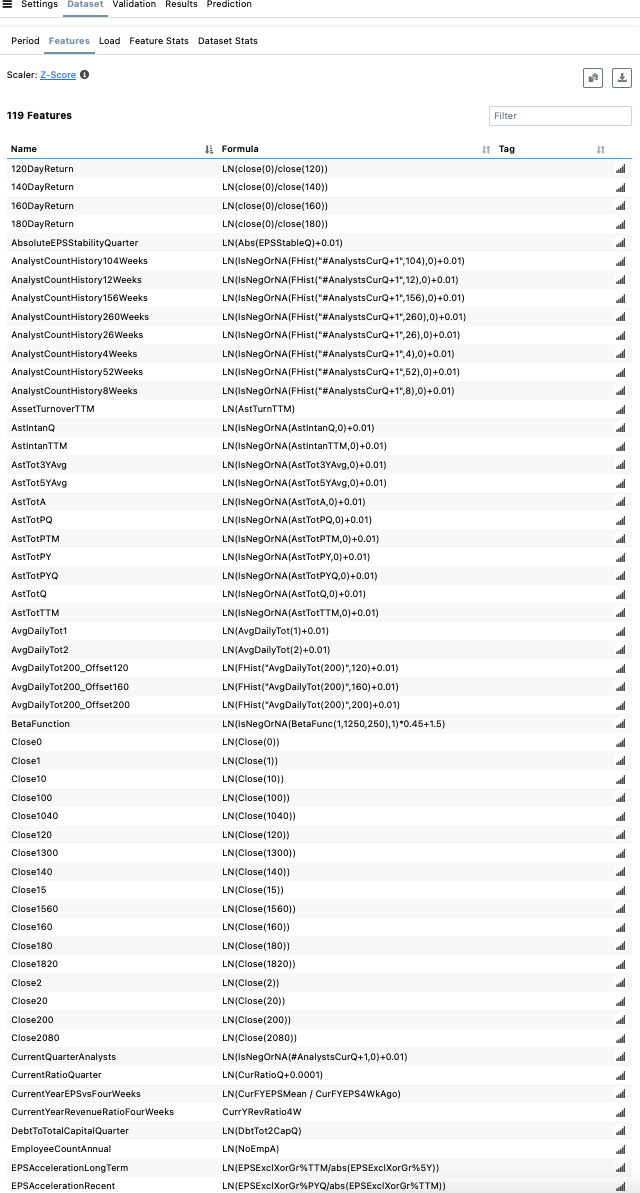

Here are the factors I used:

Then here are the settings and models I used:

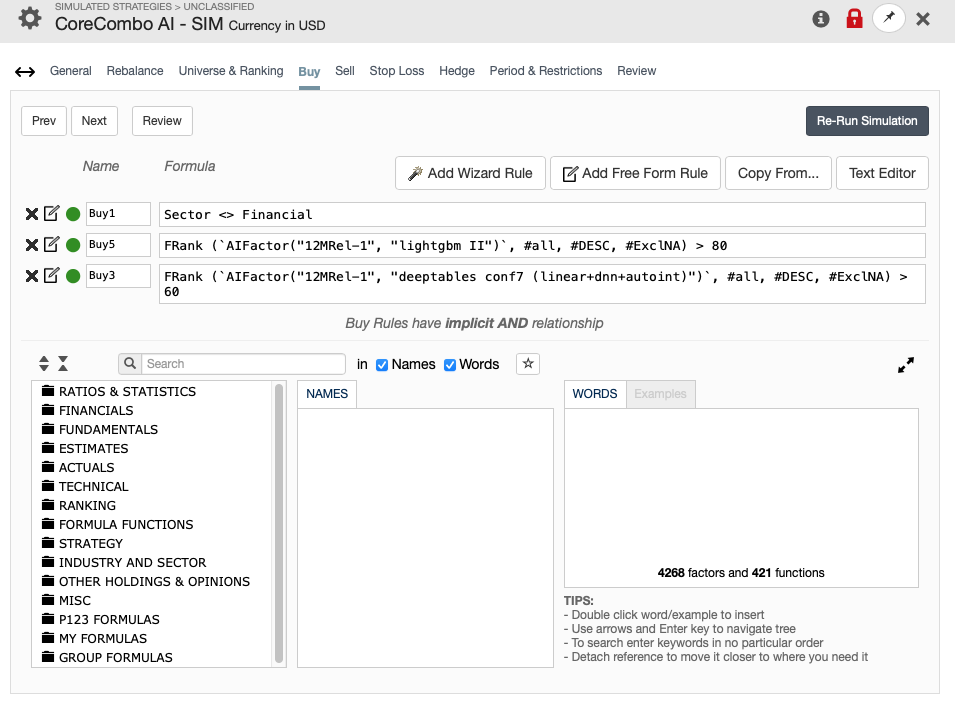

Here is the Sim/backtest sell at rank < 50... nothing fancy:

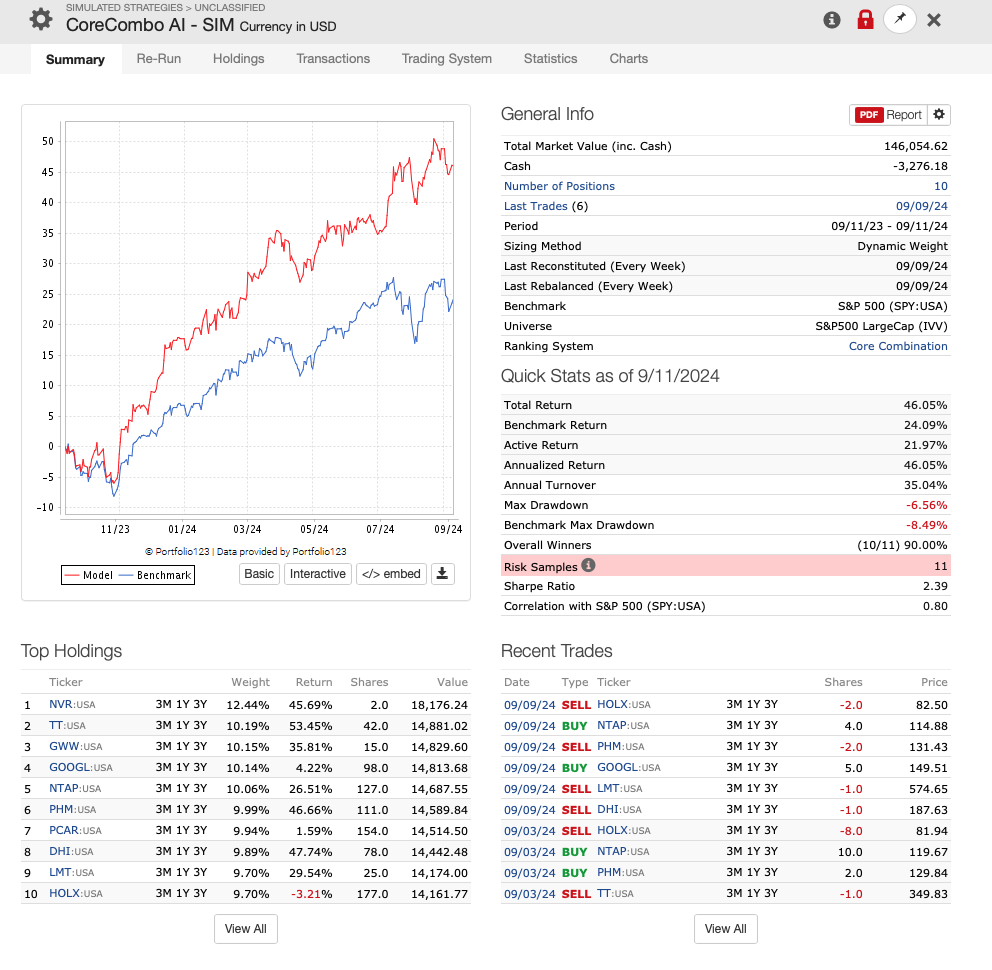

Results:

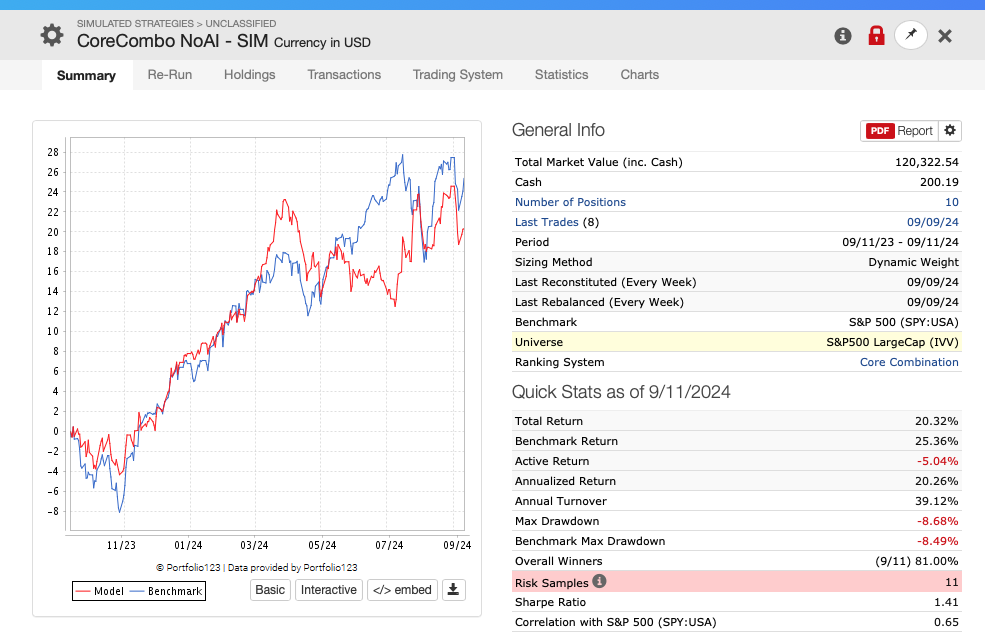

No AI version:

@ZGWZ any ideas on how to better juice these results? Like I want to see how to get over SR > 1... is it use more factors, etc? Or just be really good and pick the right ones? Or is it to try more model tuning? (i.e setting extra trees param). I could see a mix of those but just looking for ideas.

I've never gotten SR>1 in US-only largecaps universe without cheating.

I have tried a number of methods that do not improve the performance of the strategy on large cap stocks, only on small cap stocks.

Especially you have a very low turnover rate. This will either lead to overfitting or make it harder for you to achieve high returns.

If you can consider large-cap European stocks, then there is still a chance.

My advice is to invest in as small stocks as liquidity allows. For example, with average daily turnover in the millions, small caps are still much more predictable than large caps.

1 Like

Thanks, I've tried building a couple of non-AI models on Small Caps using AvgTot > X, I can revisit those. With the AI small cap models I built some with such results, but then they didn't actually perform better than the non-AI models yet. But I can try to combine with volume and see how that works out.

They theoretically should do great:

The factors used (I picked some from your list and some others I had):

I used the MicroCap universe

I think you mean something like AvgDailyTot(20) > 1000000 ?

AvgDailyTot(10) > 1000000

I would suggest that the validation period needs to include at least 2018, when volatility rises sharply, and even covid 2020 to test the robustness of the model.

I say this partly because the volatility of your High portfolio is so low, and also because your model has not been tested in the 2018-2020 Value Factor collapse.

Also, I found liquidity over 1M is okay but liquidity over 5M is too much for a good result. I would recommend 350k threshold or less.

1 Like

Is this an AI ranking model or a non-AI ranking model?

Ai ranking…. I used by deep tables and lightgbm

To me this is a sharpe ratio that is too high for the large cap universe. It is also much higher than that of your validation results. May need to be careful about the risk of overfitting on feature selection or your buy/sell conditions.

I didn’t select that many features only 20 total —- it turned over th stocks a lot about 57% winners looks good. Going to test is live see how it does out of sample

throw in the whole apartment and then some, way to go

1 Like

Good point why does my results exceed that SR of validation—- only thing is combine using a AiFactor + Ranking system so maybe that combination creates a higher SR, idk ![]()

I also always did that but that still can't exceed the validation results that much without luck.

Correct actually when I ran as AIFactor in past year with high turn-over it only barely matched performance of SP500 so yes it was a dud --- my results werent good.

BTW I do mostly just go for the small cap systems in my portfolio but I am trying to see if there is a way to beat sp500 with large caps and many are saying its very difficult.

I ran another large cap set using the Kitchen Sink approach with 404 features, it does much better... interesting is the kitchen sink method of more and more features just seem to do better than picking selective features (or at least that has been my experience)