The TED Spread indicates the perceived risk of inter-bank loan defaults. Can the TED Spread be used as a general market timing indicator? Some basic backtests give us the answer.

Cool.

SPY / SHY not so good. You are picking up the better performance of RSP.

Georg - it is s (credit) risk-on/risk-off switch. You let it loose when risk is on and you be careful when risk is off. In order to turn it into a long/short model, you would need to include other indicators.

Steve

OK, then let’s remove RSP and compare IEF to BIL.

Eval(EMA(50,0,##TEDSPREAD)/EMA(200,0,##TEDSPREAD)>1,ticker(“ief”),ticker(“bil”))

I don’t understand what point you are trying to make. Most of the stock market problems in the last 10 years have been related to credit-crisis. I expect more of the same in the near future at least.

Steve

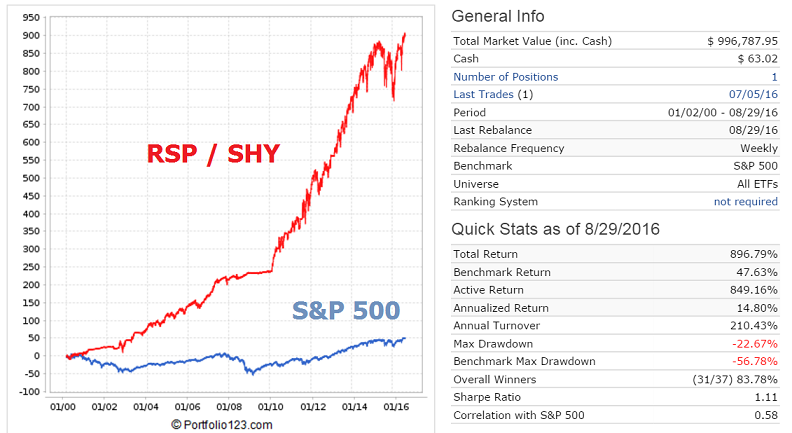

If credit risk is off then surely it is advisable to go long bond funds. If you want a better timer for equities then use the unemployment rate. This provides 3-times the return than the TEADSPREAD for the same two ETFs, RSP and SHY. Annualized return 14.8% with a max D/D of -22.7%. This is a hell of a lot better than many R2G models.

Eval(Close(0,getseries(“#UNEMP”))>Close(3,getseries(“#UNEMP”)),ticker(“shy”),ticker(“rsp”))

Yes - that is what I’m doing, either SHY, IEF, or TLT. You might be confused because I have credit off before credit on in the Eval.

So I looked at the UNEMPL some time ago and actually have used it before. BUT I am not that confident in the bogus figures dished out by the government and the fact that there are revisions to the UI figure bothers me (a lot). I may use it again but if I do I will go with a bank of indicators.

The other thing is that I’m developing forward looking models now, not impressive backtests. What happened in 2000-2002 wasn’t a credit crisis, at least as far as I am aware, and other indicators can take out that type of crash. Going forward, credit markets are one of the major issues we will have to deal with.

AND, the backtest results you are showing aren’t looking good for late 2015, early 2016, just an observation ![]()

Steve

Steve thanks for the post it’s incredible how accurate the one little formula is. Has anyone done any work with the other potential market timers and how do you combine them all to give accurate signals? Trying to figure out how they work together with what formulas is hard. The following visually look like they have potential and they have already been used in SIMS:

VIX

EARNINGS

TED

Unemployment

Short interest

Bench close

How would you figure out from the visuals the best way to use them all together or use some for the buy signal and others for the sell signal.

Regards,

Mark V.

I will be building a combined indicator but haven’t started work on it yet.

Steve

It does not matter if the UNEMPL rate are bogus government figures, as long as the BLS keeps the system of measurement the same. Also the revisions are minute, and there are many years when there are no changes.

In any case, it would be useful if we didn’t all employ the same market timing logic. Diversity makes for better all around.

Steve

Both UNempl and Tedspread work well funny they don’t work so well together is it possible to come up with a ratio that enters and exits the market?

Georg, would you kindly show me how you implemented that timing rule? Thank you.

Steve and Shaun,

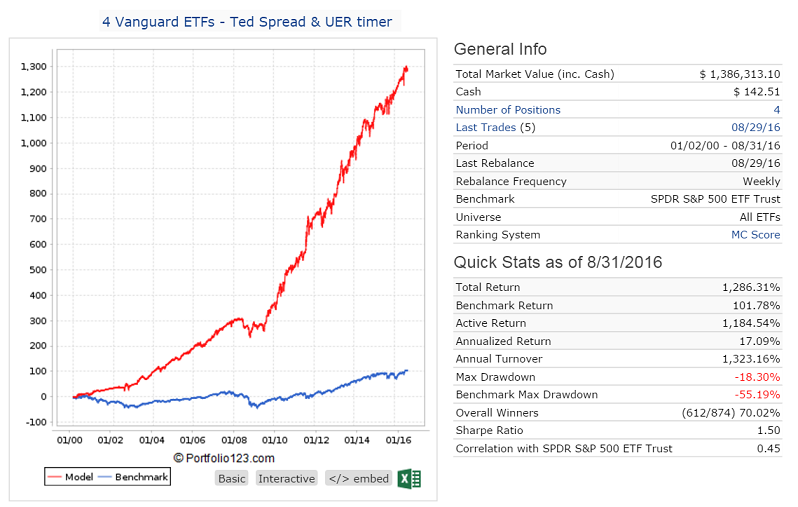

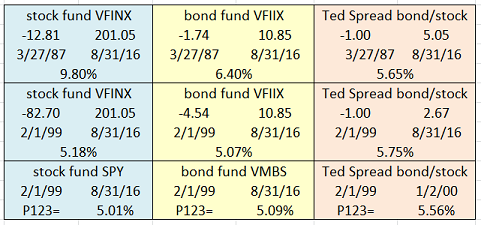

I have now tested Seve’s Ted Spread model in excel from 1987 to 2016, and from 1999 to 2016.

One can see that the 1999-2016 P123 return of 5.56% is very similar to the 5.75% obtained from excel. However, over the longer period 1987-2016 the Ted Spread model produced only an average annual return of 5.65% much lower returns than the 6.40% for mortgage backed bond fund VFIIX (ETF VMBS) or the 9.80% for S&P500 stock index fund VFINX (ETF SPY).

This shows that reliable timing models should be tested in P123 and also in excel for much longer data periods.

Next I will test the Unemployment Rate timing model over the longer period.

Georg - I’ll have a look at it in greater detail and provide some comments. But in the meantime, a worthwhile exercise for you is to identify when you first started using UNEMP, then separately determine the in-sample backtest stats and out-of-sample performance. Then compare the two. Your glasses may be a bit rosier than mine.

Steve

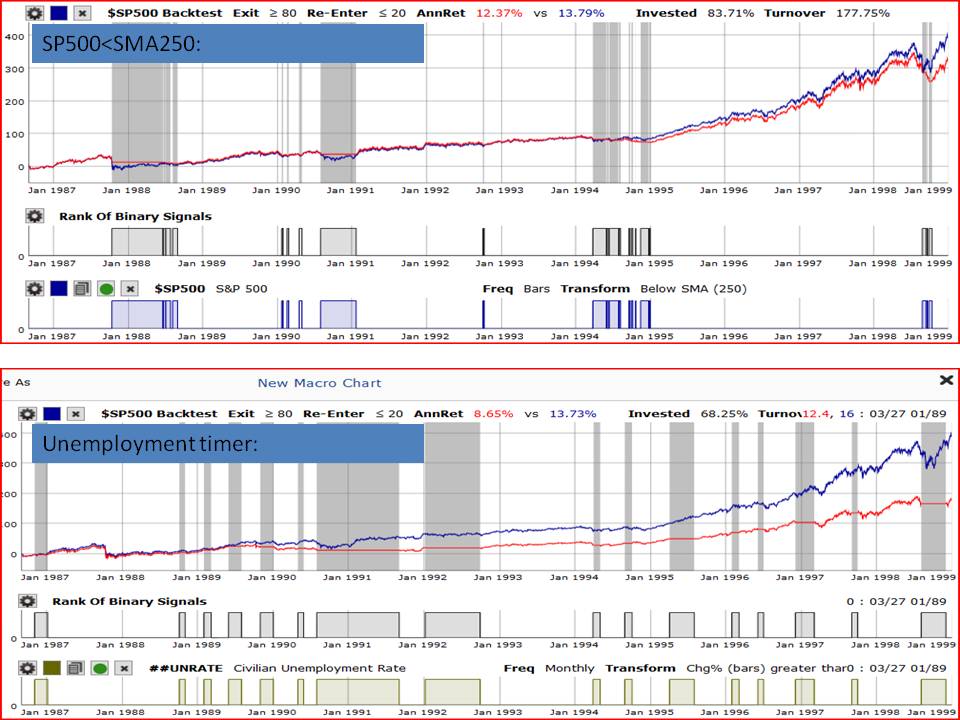

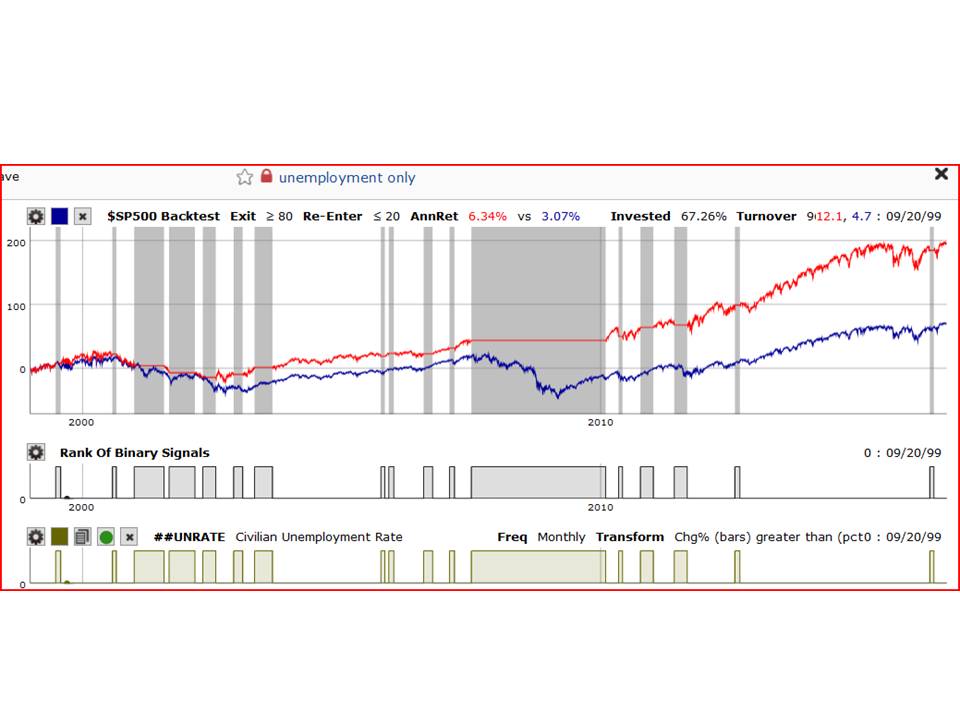

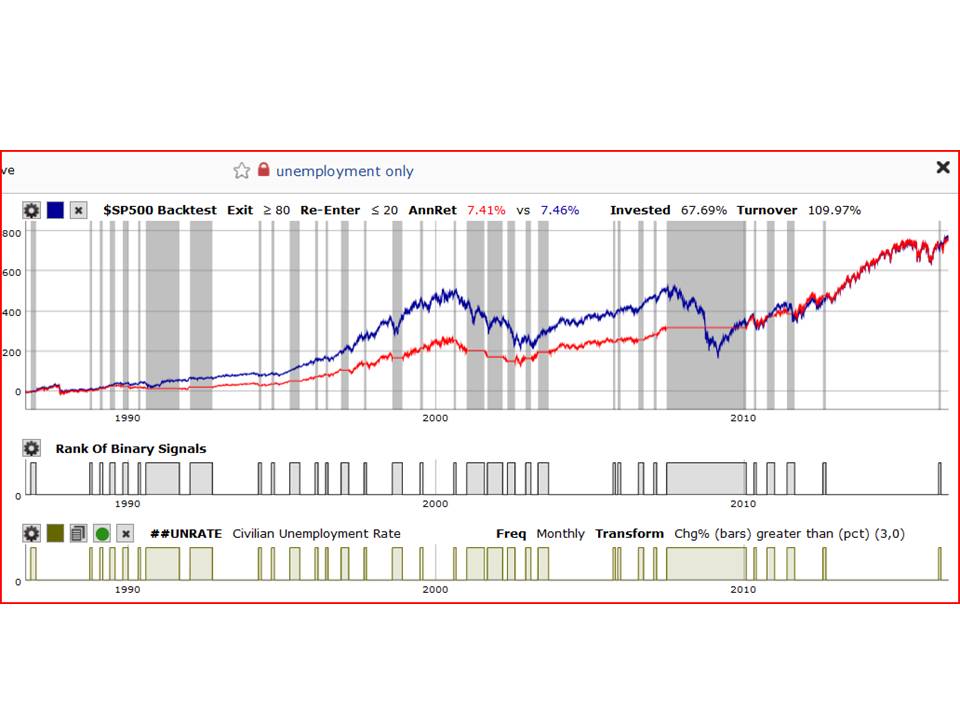

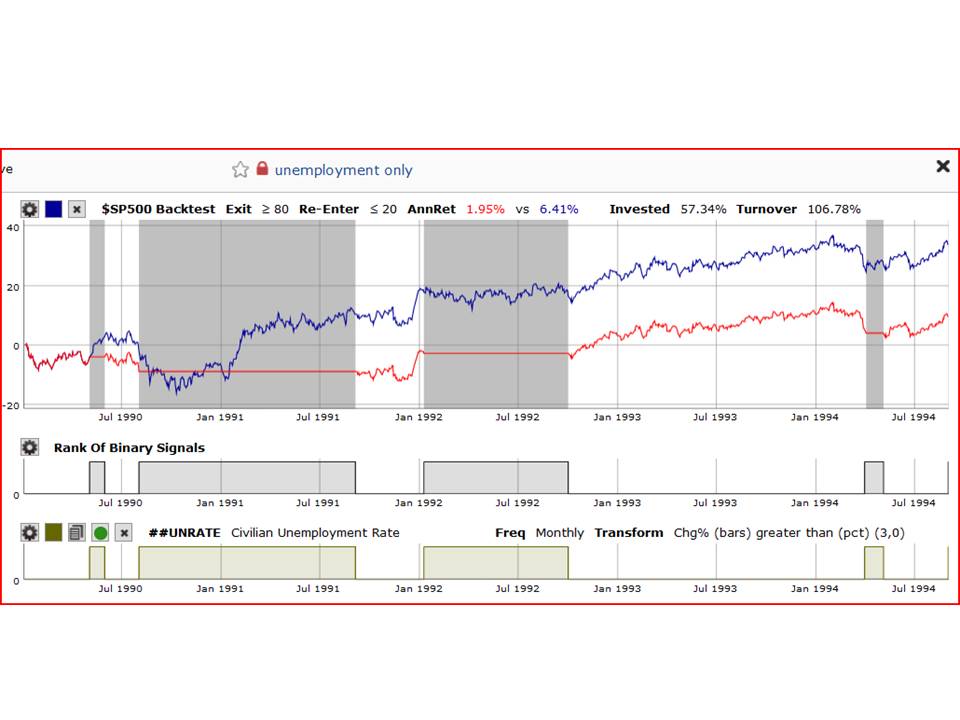

Below are screenshots of a macro built using Georg’s timer (unemployment > 3 months ago). First screen is last 17 years – not bad. Second screen is last 30 years… not so good. Third screen is early 1990s where you can see unemployment continued to grow long after a brief recession.

-Debbie

Debbie - Now you have to add the performance of bonds during the periods when not in stock market. Then the UER timer comfortably out-performs buy-and-hold stocks also over longer period.