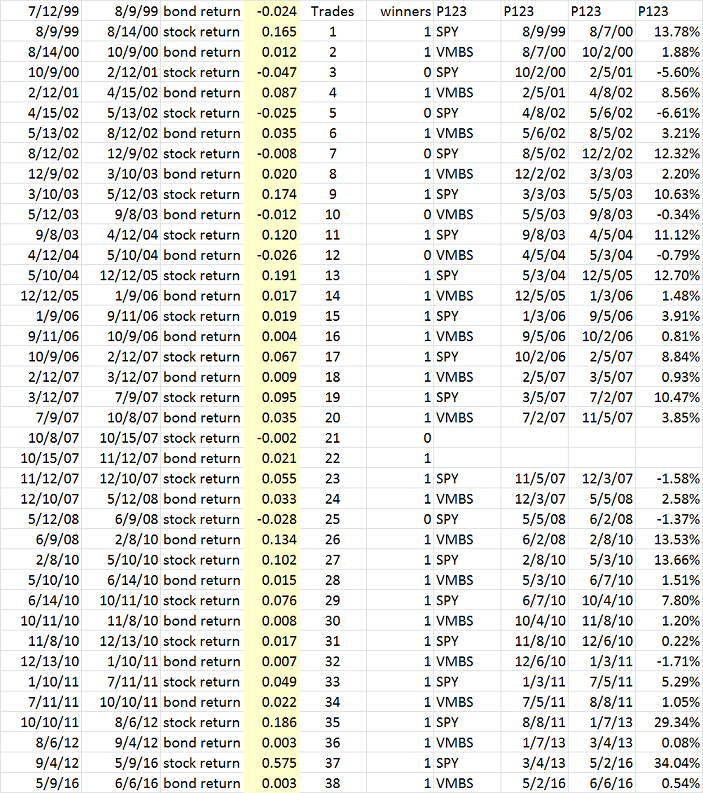

Debbie - P123 list the UER number on the last day of the month to which it refers. That is actually too early in time. The UER is usally reported on Friday following the last day of the months. Today 9/2/2016 the UER was reported by the BLS for August. However this number will be listed at P123 for 8/31/2016. So we have some discrepancies here.

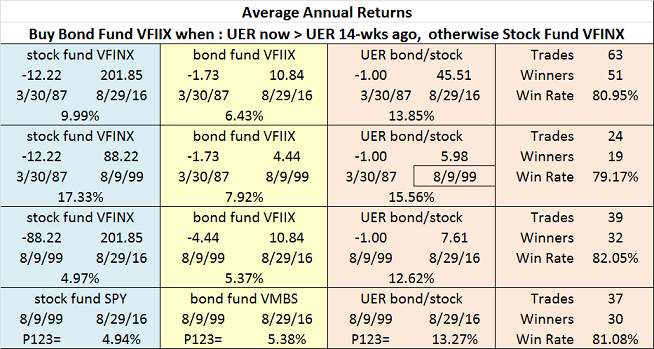

I have a PIT spreadsheet on a weekly basis for the UER to cope with this discrepancy. In my excel spreadsheet my test is: UERnow > UER-14wks ago.

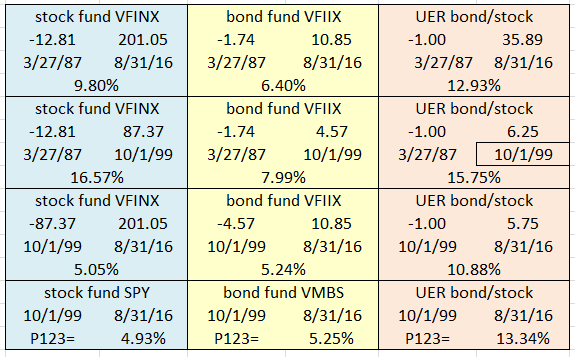

My test shows that for the period 1987 to 1999 the UER model switching between bonds and stocks was not a great timer. However it only marginally under-performed a buy-hold for stocks. From 3/27/87 to 10/1/99 VFINX (stocks) produced an average annual return of 16.57%. That’s tough to beat when one switches to VFIIX (bonds) which “only” produced an average annual return of 7.99% over the same period.

The bond/stock UER model produced 15.75%, marginally less than buy-hold stocks.

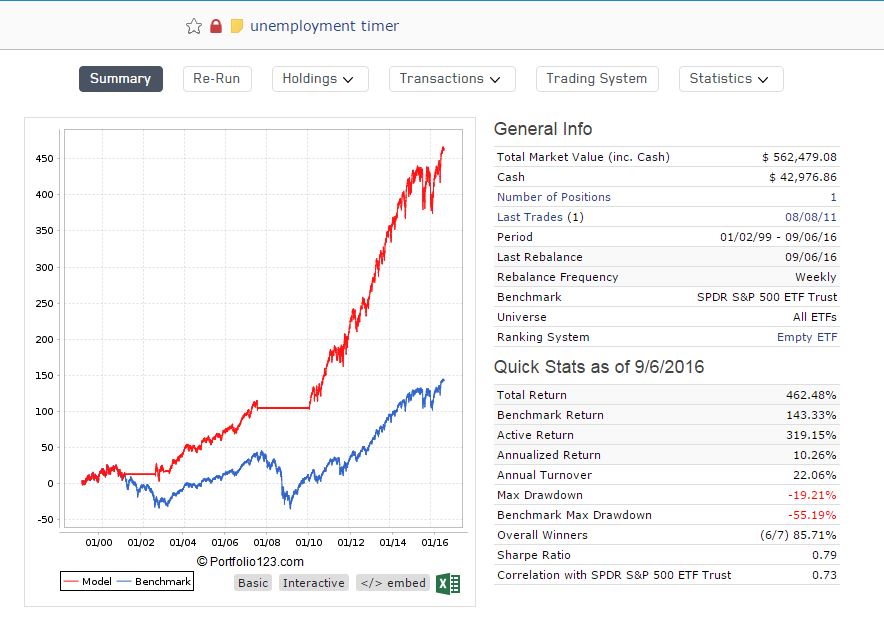

But over the 29.5 year period 3/27/87 to 8/31/2016 the model’s return was 12.93%, much higher than the 9.8% return for buy-hold stocks, or the 6.4% return for buy-hold bonds.

Of course, after 1999 the UER model convincingly out-performed stocks and bonds, showing a 10.88% return to end of August 2016, whereas SPY only returned 4.93%, and VMBS only 5.25%. The 13.34% for the UER model running in P123 is a bit suspect, due to data discrepancies mentioned earlier.

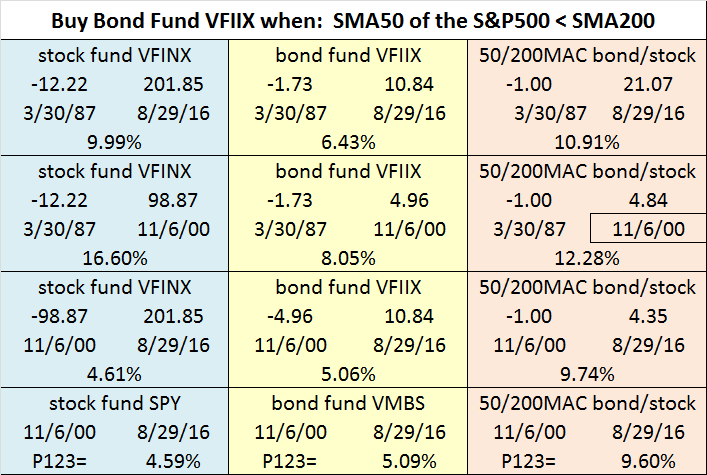

This shows that the UER model should be quite reliable. I have data back to 1948 for the UER, stock market and bond market, and I will test this again for this 68 year period.

Georg - there is no doubt that UER has value, but your last post just reinforces my beliefs. You are using a very raw form of indicator without smoothing, then relying on any revisions being small so as to not affect the results. Also the one week delay is problematic for Portfolio123 and is likely why UER is listed as deprecated.

All (most) of the stats you are showing are hindsight. The only real interest I have is in OOS results i.e. post-introduction performance of this indicator. I’m pretty sure it was prior to 2015 so can we see the OOS results only instead of the marketing spiel?

Georg – Thanks for sharing the details of your calculation. I think unemployment makes sense for inclusion in a market timer –I’m not sure about having it as the sole factor, but your data does support it. If you learn anything from your add’l calculations, please let us know.

I was just reading a post by Aswath Damodaran and he felt that interest rates could follow more from GDP growth and inflation (not the Fed so much). (He cautioned that both could actually drive stocks higher in the short term, though.)

"I believe that today’s low rates across developed markets is not a passing phase or a central bank set anomaly but more a reflection of a low inflation (perhaps even deflation) and low real growth. "

I have redone the excel MAC timer and excel UER timer, so that trading is only done on the first trading day of the week. The correlation with the P123 sim is pretty good, especially for the MAC.

GDP is quarterly and heavily revised so does not meet my requirements for an indicator.

When I reflect on what Damodaran says, I hear “expect lower returns”. With generally lower growth there is less potential for US companies to gather share of global growth. This could imply that demand for unique growth stories is high, such as Uber or other new tech plays. At the same time continuing demand for yield or stable income as capital gains slow. The equity valuations have been heavily driven by credit expansion in the US since 1983 which coincided with the boomers. Governments and central banks are trying to prevent deleveraging of financial system collateral as consumers have retrenched. The BoJ and ECB have picked up where the Fed left off and I would expect this to continue until it can’t, which may be 5-10 years.

I am going to work more on timing around volatility in the Financial sector, which will be the canary in the coal mine when financial assets pass their Minsky Moment.

As I see it, the Fed Reserve no longer has control over interest rates. The long term rates won’t budge if they increase Fed Funds Rate and they are starting to realize that. Their best bet is to leave rates where they are or set them to zero and let the government(s) focus on fiscal policy. I see the problem arising that in order for central banks to remain relevant they need to be in charge of fiscal policy and everything will get as screwed up as monetary policy.

One thing they might try is to stop the currency wars and have all central banks raise interest rates at the same time, including the US. This would mean that the currency exchanges would be unaffected but will make people happier i.e. higher interest for retirement accounts, room to lower rates when next recession arrives, etc. The problem is that this is not particularly feasible when one considers the massive global debt.

As for GDP and inflation, they are both contrived numbers. It just means fed reserve manipulation, more fiction, less fact.

Georg - With globalization and the internet revolution, US employment is becoming less and less relevant to Wall Street profits.

I used this rule:

Eval(Close(0,getseries(“#UNEMP”))/Close(3,getseries(“#UNEMP”))>1,ticker(“shy”),ticker(“rsp”))

Close(0,getseries(“#UNEMP”))/Close(3,getseries(“#UNEMP”))>1

is the same as:

Close(0,getseries(“#UNEMP”)) >1*Close(3,getseries(“#UNEMP”))

which is the same as your formula.

This should give the same result.

I used next close and no slippage.

Steve, there is no way one can do this. I checked the UER model in excel with UER real time and weekly data, trading on the first trading day of the week. I almost got identical trades and dates as in P123. So I think it is ok to use data as is.

I don’t know why P123 wants to deprecate #UNEMP. I have lots of custom formulas using it, and it is also used in my SA model Best4 MC-Score ETFs. Perhaps the P123 team can enlighten us of what they have in mind.

Yes, I also like to know why UNEMP is deprecated. It is a very useful parameter and it has improved 2 of my ports considerably. Maybe a wrong announcement?