I think I’m done reading about covid-19 (other than safety informational stuff). The same things are being rehashed and we can’t forget that nobody actually knows what they’re talking about. I’m also bored hearing about how the market sucks; it’s the worst kept secret this side of Hillary Clinton’s email server.

So I figure it’s time to think ahead, to what the world, or at least the investment world, will look like when all this is behind us. Bear markets aren’t just corrections, valuation adjustments, etc. They often relate to structural excesses and shocks that, even when aggregate numbers get better later on, ultimately change the world. So what might a post covid-19 recovery and/or bull market look like?

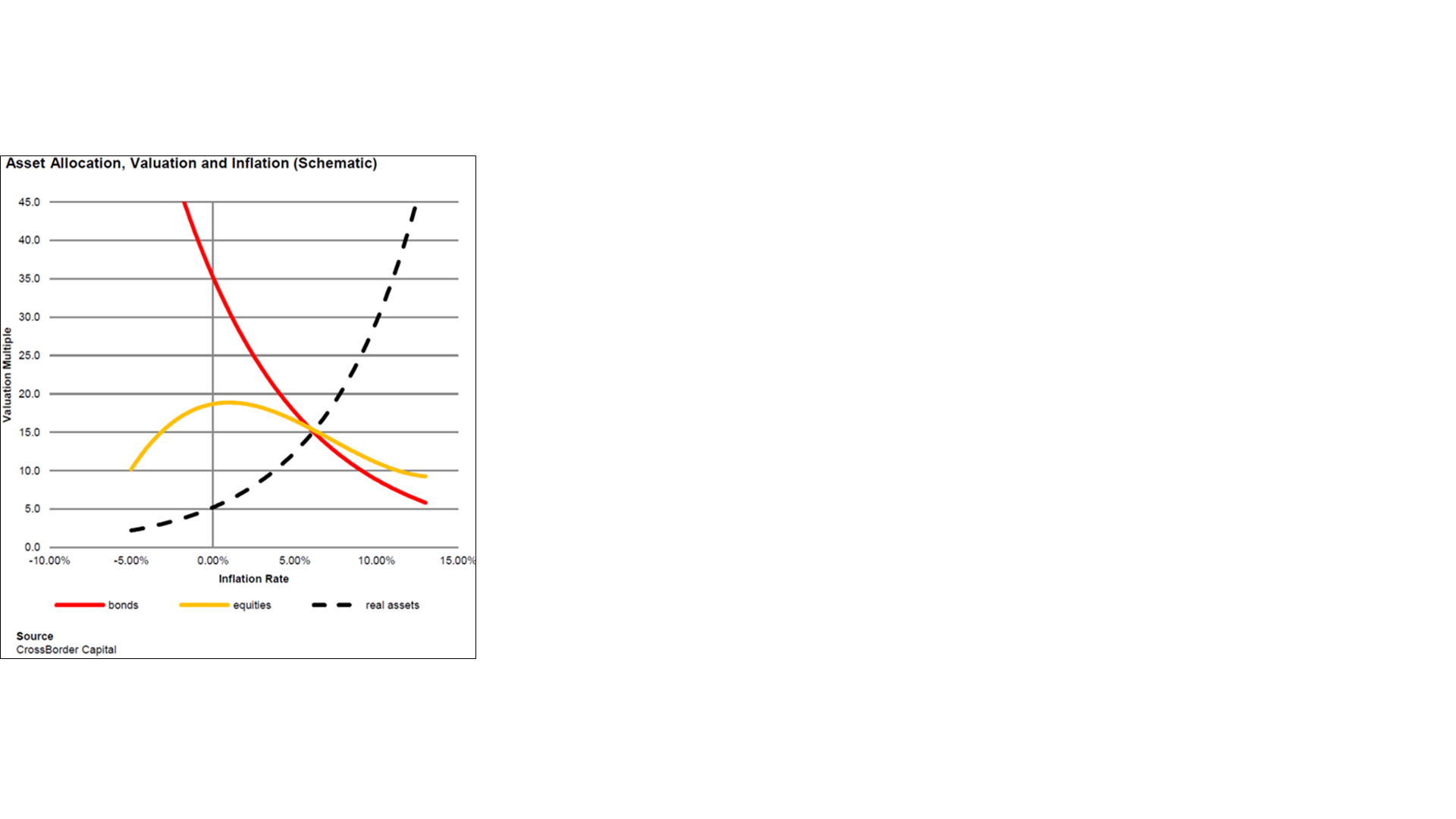

Disinflation, such a pronounced feature of the economy since 1982 that people hardly even talk about it, may be dead for a generation or so. We see the pathetic efforts top prod the Fed into acting and finally, the realization, that the Fed is done. It has no ammo. No more weapons. The accelerator has been floored and the engine is flooded. We’re going to have to pull our old Keynesian books out of storage and possibly even digitize them (Not sure anyone read any since digitization was invented) and apply heavy fiscal stimulus. Just look at all the commerce that’s vaporizing, paychecks that will be missed, rent bills that can’t be paid, etc., etc., etc., etc. Nobody impacted gives a sh** about the discount rate. The economy needs cash and the govt printing presses will need to be cranked up. The only mystery is how much economic pain we’ll need to feel before the geniuses who hog the public pulpits figure that out.

This will be inflationary . . . Any nobody will care, or if anyone complains, expect the 21st century equivalent of tarring and feathering. That means we’re REALLY REALLY REALLY not going to get to meaningfully negative interest rates (aside from those fees with fancy labels) and that the 35-year downtrend in interest rats now looks much more likely to convert to an uptrend rather than stay flat (the best case scenario until recently).

When I started in this business, a P/E of 8 or so was considered pretty respectable and 12-15 was nosebleed territory. Expect valuations to eventually start a long multi-year and possibly multi-decade march back in that direction.

That may get to 180-degrees opposite of the world that p123 has lived in since its existence, and more importantly, the world depicted in p123’s backtest database. Sop take a look at your best sims. Are you itching for the market to recover so you could crank those models up again? Be careful. Understand WHY you got those 45-degree plus up-trending 1999-2020 equity curves and inquire into how much the model benefitted from the 35-year bull market in interest rates and P/Es.

You can still use backtesting, but you really need to restructure your understanding of how to interpret the results you see. Test showing positive alpha may signify models that may now need to be abandoned. Maybe you want to see negative backtested alpha for a while (until enough time passes for a new regime’s worth of data to get into the backtest database). I’m not saying it will turn out quite this simplistically. But that possibility is a much higher-probability scenario than is the one where the super 1999-2020 equity curve actually reflects what you’re likely to see (this latter scenario is a zero probability scenario). Oh . . . And please abandon that stupid R-word (robustness). That’s just a bunch of ego-crazed folks who thought the results they showed came from their modeling genius and didn’t realize that it due to Uncle Fed flooring it for nearly 40 years — anyone can show the apperance of robustness when the world goes that long without seeing a change in relevant conditions.)

You’ll need to be owning shares of companies that can grow earnings (and not just wait for the Fed to pump P/Es on earnings streams that go nowhere), and that grow earnings by growing sales (and not simply by laying people off, a 35-year long management tool that unless abandoned will most likely lead to President Oscanio-Cortez (who will be old enough to run starting in 2024).

This is why I’ve been telling people to learn about companies. Fk Python and all the other bullsh features people have been clamoring for. That crap is not going to make a nickel for you going forward. Learn how to critically read 10-Ks and 10-Qs, IR presentations and conference call transcripts well enough to be able to articulate in p123 syntax, the kinds of companies you want to be owning. It your new models test with good alpha from 1999 to 2000, you may have screwed up and ,may need to go back to the drawing board. Some thoughts: sales growth strong enough to produce enough growth in pretax to offset possible corporate tax increases (the Trump cut will likely be remembered as a landmark that helped mark the end of the old regime), sales growth strong enough to offset potentially diminishing margins. Strong balance sheets . . . Enough cash flow to support de-leveraging could become a plus. (Stock buybacks, long loved, may turn toxic not by act of congress but by mandate of new-regime equity investors — even Cliff Asness may decide he wants to see secondary equity offerings.) Obviously, you’ll have to watch the business world and stay alert to new products, services and business models that cater to the way society is evolving — this sort of thing always needs to be done. You may also want to think in terms of real estate (REITs — so long as you stick with the right sectors; I favor residential and healthcare for starters), and still-relevant commodities (old energy likely being kicked to the curb permanently. Even gold — I actually picked up a smidgen of GLD (an entry level dabble), not as a market hedge but thinking ahead to possible future inflation. Obviously, demographics being what they are And us getting caught with our patriotic pants down in terms of medical preparedness, I gotta figure healthcare needs to be owned. Tech goes without saying, but make sure your focused on new tech — don’t keep obsessing on the same old stuff.

I should mention that this isn’t deep analysis; its just thinking aloud while while whiling away the pandemic . . . Kinda like the pilgrims who gathered while seeking shelter back in the black death era (hint: another thing you could do if you get sick of talking about the bear market, read Cantebury Tales, hilarious stuff, but get a modern translation that accompanies the original).

Thinking about the market’s future is not an event; it’s a process, and for me, this is early-stage process. I don’t care if you agree or disagree. Nobody knows and eventually, Father Time will reveal the answers. What I do care about is that you start your own process. Pull your minds out of the 1982-2020 regime and work your way to how you’ll do things in 2020-whenever. Don’t expect new models/strategies overnight. This is a process.