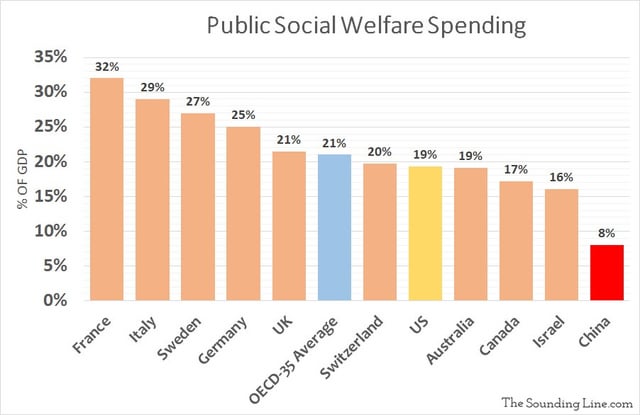

Well the issue with China as an example is China (as a one party state) does not let you vote against mines, oil, development, etc. That would help explain a lot of the difference. Both have land controlled by the state but the state is very different. China is a “small” government, low tax, low welfare state industrializing quickly.

Trump ‘immediately’ imposes 25% tariffs on countries that do business with Iran. China’s on the list

1 Like

Yes industrialized nations (not just western but all/most of them actually. Japan, Russia, China, etc) do tend to like extracting resources from wherever available which does incentivize such clashes historically

1 Like

SZ,

I don’t think that China maintains a “small government” policy.

China maintains tight control over all aspects of society and the economy. The CCP maintains monopoly on political power and assert the power of the state to direct economic activity.

While China operates a market-based economy, the Chinese government deeply impacts economic activity. State-owned firms still account for a significant portion of industrial output, and local governments often heavily influence economic development.

Just look at how China currently bans the import/usage of Nvidia’s latest H200 chips and how they decide where to purchase soy beans for the country.

Regards

James

I think there are several things at play here. The Greenland situation is uncomfortable and poorly approached. But we also shouldn’t take our eye off Japanese yields. That dynamic may represent an equal—or even greater—market risk now and going forward.

The deeper problem with the way Trump is acting is that by continually weaponizing the dollar, he’s actively incentivizing even reluctant participants to de-dollarize as quickly and decisively as they can. Once that process gains real momentum, it feels to me like much of the game is effectively over.

That, in turn, forces a harder question: where do dollars go when they’re meant to be risk-off? I’m confident they don’t belong in long-duration bonds. The recent “permanent portfolio” discussions are interesting in this respect—particularly where people talk about modifying the framework to divest the most recent underperformer, without fully acknowledging that such behavior undermines the very premise of a permanent portfolio.

For a long time, cash has served as a reasonable short-term risk-off placeholder. But it’s no longer inconceivable that even cash could become an uncomfortable place to hide during risk-off.

1 Like

As I was reading your post I got a notification that one of Sweden larger pensions funds has started to sell off US government bonds.

Alecta Offloads Billions in US Treasuries Due to Political Risk

Alecta has offloaded a significant portion of its holdings in US government bonds, the pension giant confirmed to the Swedish financial newspaper Dagens Industri (DI).

According to the newspaper's reports, the sale amounts to approximately 70–80 billion SEK (approx. $6.5–7.5 billion), which was sold in stages over the past year.

Reasons for the Sell-off

The primary driver behind the move is the perceived increase in risk associated with more unpredictable US politics under Trump’s leadership, according to Head of Asset Management Pablo Bernengo.

Alecta assesses that the risks surrounding both US government bonds and the dollar have intensified, particularly as the country grapples with:

• Large budget deficits.

• A rapidly growing national debt.

*Gemini translation

2 Likes

Algoman,

They are following the move made by Danish Pension Fund yesterday.

Here is the update from Reuters 24 hours ago.

Regards

James

Danish pension fund to divest its U.S. Treasuries

By Reuters

January 20, 202610:48 PM GMT+8Updated 21 hours ago

COPENHAGEN, Jan 20 (Reuters) - Danish pension fund AkademikerPension said on Tuesday it would sell off its holding of U.S. Treasuries, worth some $100 million, by the end of this month, blaming weak U.S. government finances.

AkademikerPension said the decision was not intended as a political statement linked to the rift between Denmark and the United States over Greenland.

"The decision is rooted in the poor U.S. government finances, which make us think that we need to make an effort to find an alternative way of conducting our liquidity and risk management," Investment Director Anders Schelde said in a written statement.

"Thus, it is not directly related to the ongoing rift between the U.S. and Europe, but of course that didn't make it more difficult to take the decision," he added.

AkademikerPension has in total 164 billion Danish crowns ($25.74 billion) under management, it said on its website.

($1 = 6.3711 Danish crowns)

Reporting by Soren Jeppesen, editing by Anna Ringstrom and Terje Solsvik

2 Likes

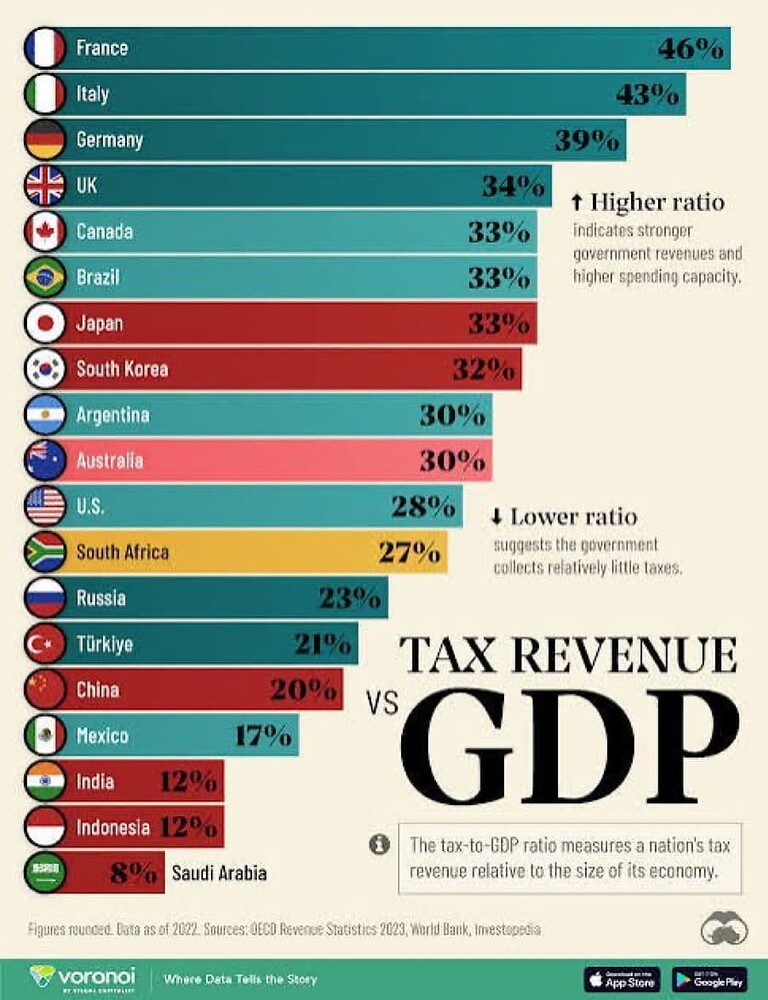

That is why it put it in quotations. But basically they are “small” because they don’t spend as much as other nations and tax to GDP is smaller along with welfare. Nations with low tax burdens tend to grow much faster than nations with high tax burdens on the private sector as it allows for faster capital buildup in the long term. In the short term more government spending can juice GDP but if its spent on non-productive items it may not translate to future GDP the same way capital investments do

1 Like

But not for the next 3 years.

1 Like

If it is like 2011 they have more runway yes but who knows! Leaning towards it going longer for now as well but it is clear excesses and emotional decisions are taking place

1 Like

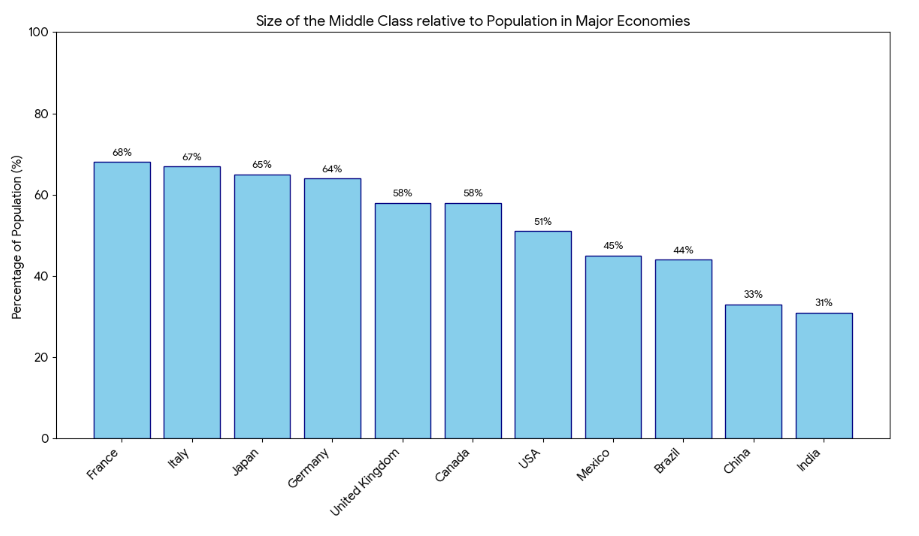

The tax chart is highly correlated to the size of the middle class in nations. Nation with an already large middle class has been through the growth phase already.

2 Likes

Growth helps create prosperity, yes. It is also true that countries with a smaller capital base or lower starting technological adoption can grow significantly faster. It is a good addition to the above. Also, different tax policy and investment choices will lead to different outcomes for nations that start at similar points. Growth is a continuum dependent on a nation’s choices. The obvious examples would of course be North Korea vs South Korea or Singapore vs Cuba or Chile vs Venezuela

1 Like

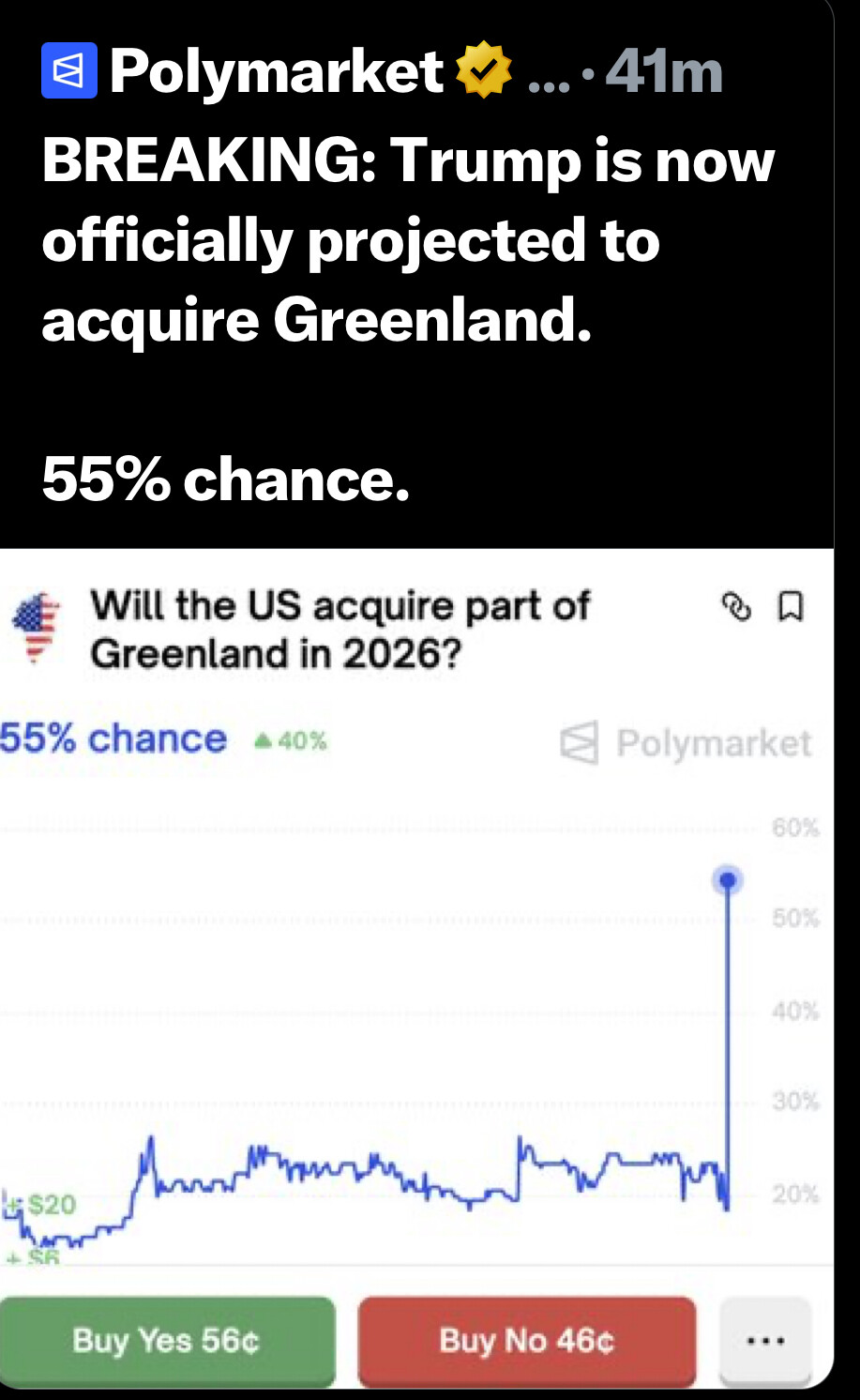

It gets worse and worse, this just came in from New York Times,

Trump Appears to Confuse Iceland and Greenland

“Our stock market took the first dip yesterday because of Iceland,” the president said, referring to market shifts related to his repeated threats to seize Greenland. “So Iceland’s already cost us a lot of money.”

Jan. 21, 2026, 12:01 p.m. ET

President Trump on Wednesday seemed to confuse Iceland — a Nordic nation of around 400,000 people known for volcanoes and glaciers — and Greenland, the semiautonomous Danish territory on which he has set his sights for reasons that he and his advisers say include U.S. security, access to minerals and “psychological” necessity.

In his closely watched speech at the World Economic Forum in Davos, Switzerland, Mr. Trump criticized Europe and cast the world as almost entirely reliant on the United States for peace and prosperity.

“I’m helping Europe, I am helping NATO, and until the last few days when I told them about Iceland, they loved me,” he said. However, it is Greenland that is at the center of the trans-Atlantic tensions over Mr. Trump’s repeated threats to seize the territory. .

“The problem with NATO is that we’ll be there for them, 100 percent, but I’m not sure that they’ll be there for us,” the president continued. “They’re not there for us on Iceland, that I can tell you. Our stock market took the first dip yesterday because of Iceland. So Iceland’s already cost us a lot of money.” The markets dipped on Tuesday over the tensions on Greenland.

Mr. Trump also mistook the two countries a day earlier, while speaking to reporters at the White House for 90 minutes to mark the anniversary of his return office. Mr. Trump has threatened hefty tariffs on European countries standing between him and his quest for control of Greenland. “As an example,” he told reporters before traveling to Switzerland, “Iceland, without tariffs, they wouldn’t even be talking to us about it.”

Claire Moses is a Times reporter in London, focused on coverage of breaking and trending news.

1 Like

Exactly. China and the larger European countries hold vast amounts of US currency and treasury bonds. If Trump pisses them off too much, they could flood the market.

1 Like

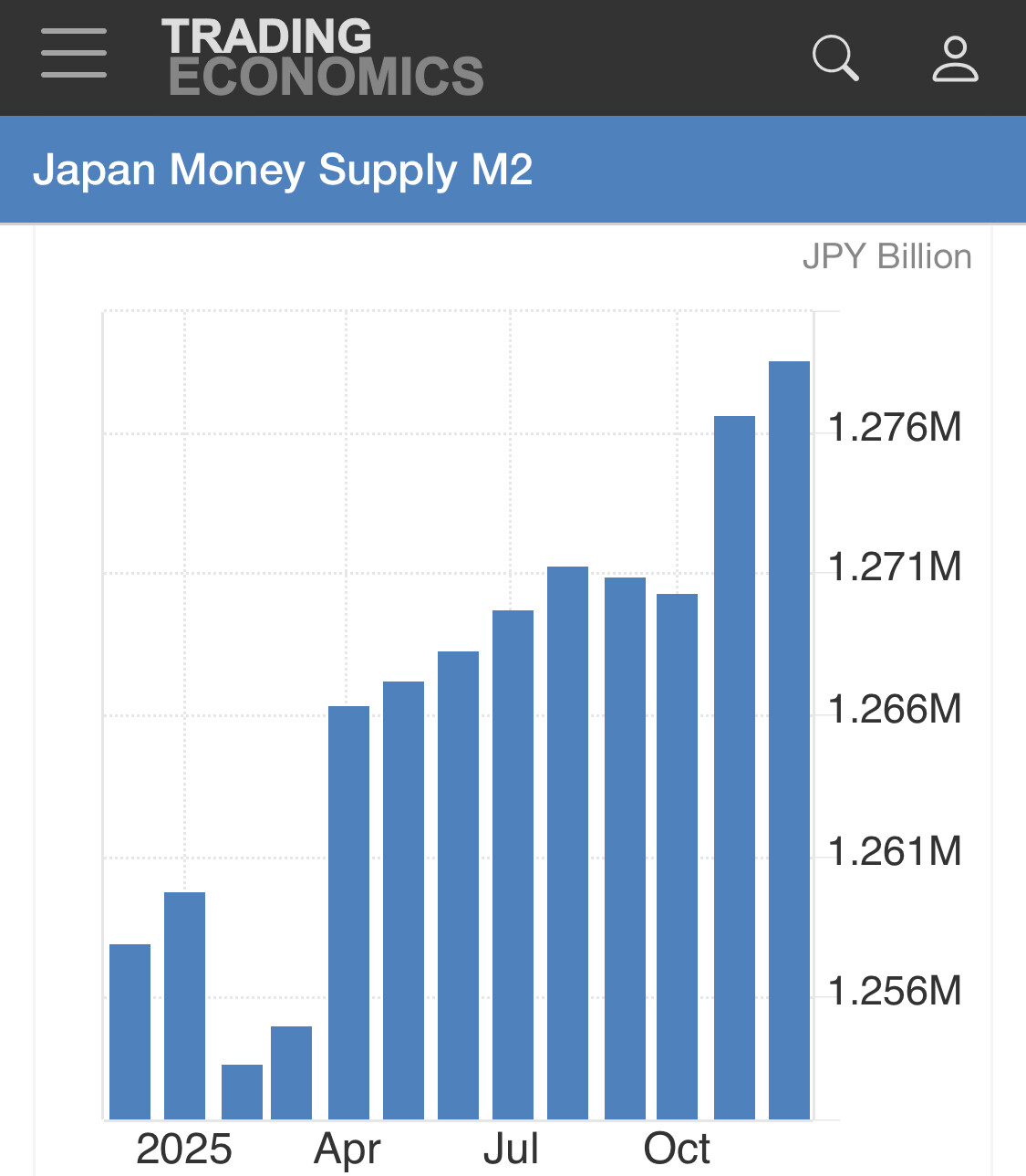

Yes, and perhaps more importantly, Japan is the largest foreign holder of U.S. Treasuries, and recent shifts in Japanese yields and hedging costs create incentives for Japanese institutions to reduce Treasury exposure and repatriate dollars—reasons largely unrelated to the political noise the rest of the world is reacting to. In many ways, decades of cheap Japanese funding have underwritten global risk-taking, so even a partial unwind carries meaningful risk. It will be interesting to see how this plays out.

1 Like

A lot of weaponry is being moved into near-Iran areas. Greenland is also potentially a diversion

1 Like

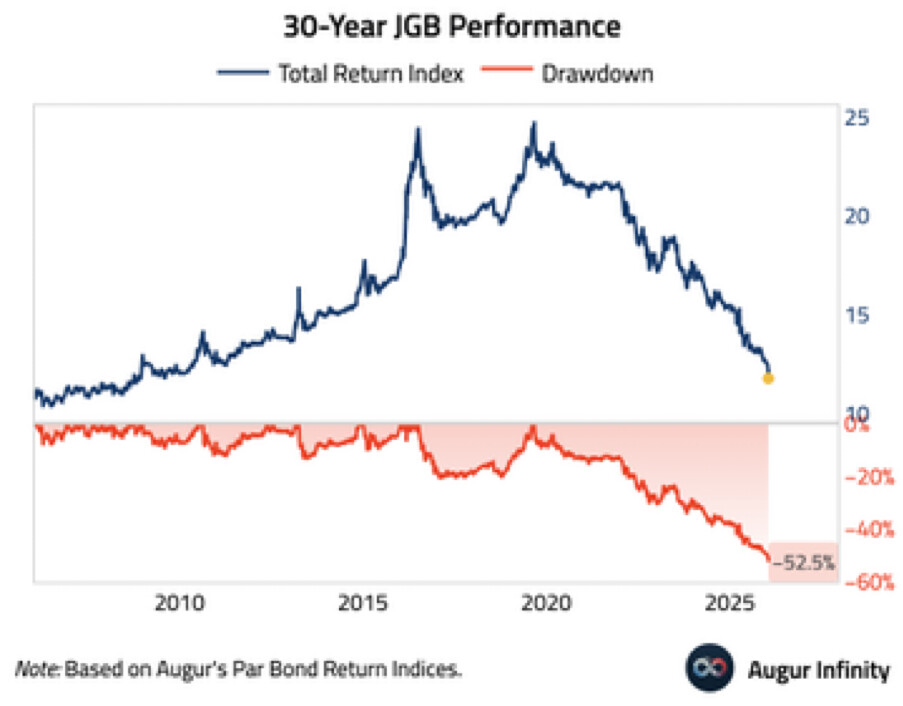

I think Japanese bonds recently had a 50% drawdown so many are still wary of holding them. The short term bonds and medium term bonds are still yielding less than inflation, but the very long term ones are now starting to have real yields

The large difference between long term and short term rates and the negative real yields are creating strong credit expansion and keeping inflation alive. My guess/ base outlook is short term JPY yields keep increasing. I am still keeping my Yen loans though

1 Like

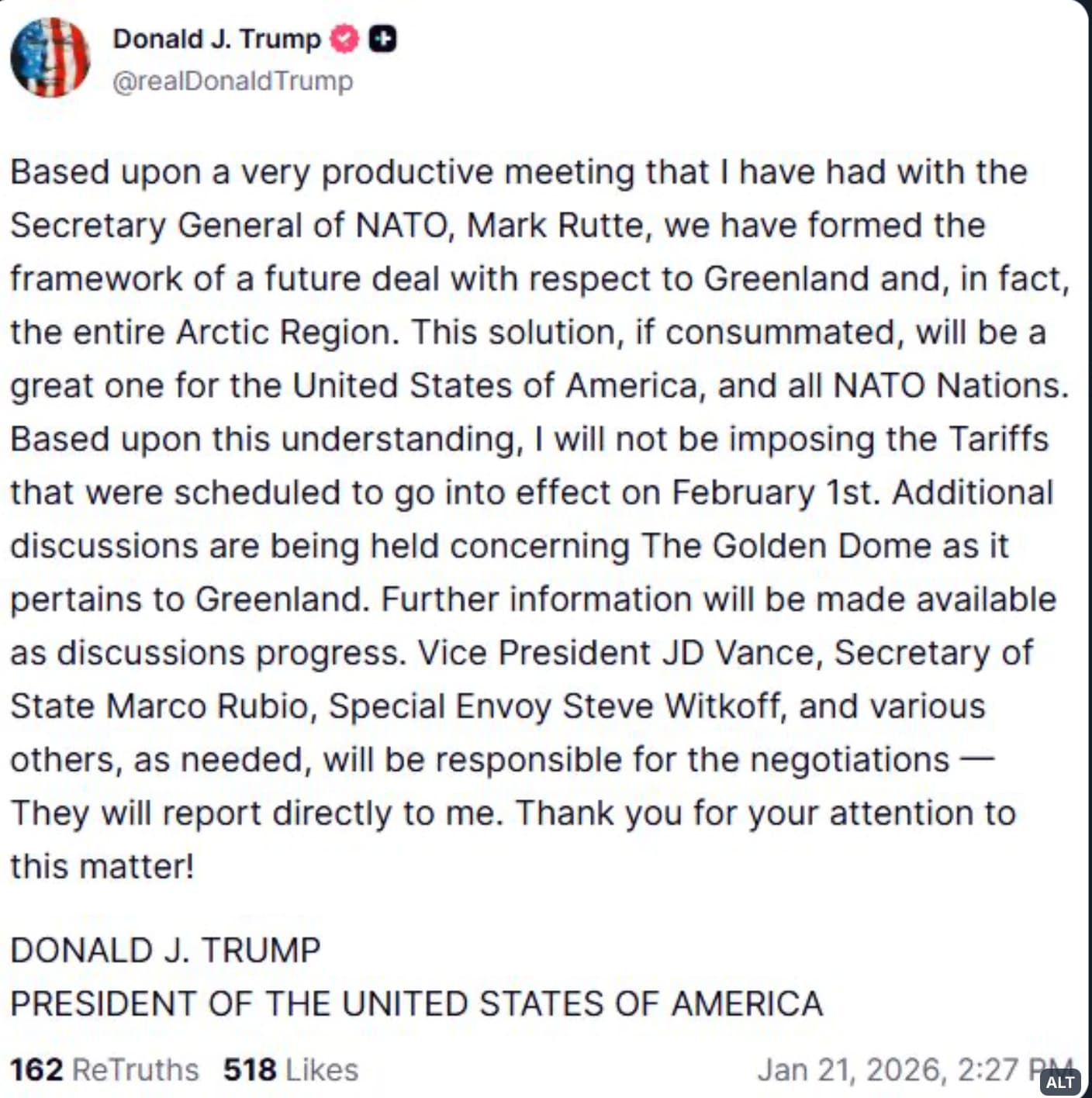

You are right test_user, this is the end of the discussion for now since Trump say a framework deal has been reached with NATO for Greenland.

No comments from Denmark or Greenland so far.

Therefore, I am not going to update this thread any more.

1 Like