Dear All,

This post is about non-financial statement data, like estimates, insider, institutional only.

As explained in this post for the upcoming Canadian data we have re-built all the USA data. This is what Compustat/CapitalIQ allows you to do and it’s what we did to populate point-in-time values back in July 2012 when we switched to Compustat. After the switch we built the historical weekend data by snapshotting current values.

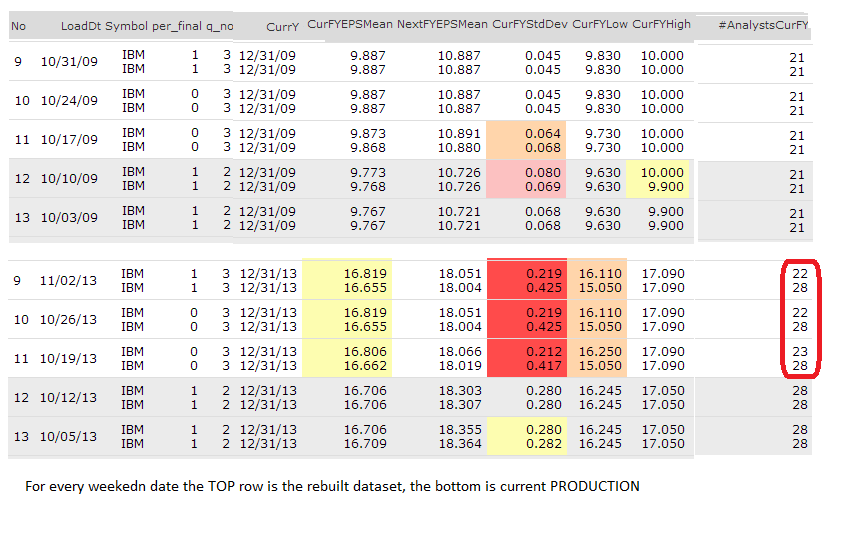

When we rebuilt USA for the Canadian project some slight differences are showing up. You can see the kind of differences in the image below that compares re-built USA values and current snap-shotted values. Here’s what we’ve found out that could be causing this:

- Starting in July 2012 we were snapshotting on Saturday. When we found out that quite a bit of updates were coming in “late” on Sunday morning we started snapshotting on Sunday.

-For certain seemingly startling differences like the # of analysts for the CurrY for IBM going from 28->23 or the CurFYEPSMean changing on 10/19/13 , we asked Compustat. Their answer was:

8 of the brokers estimates were excluded from consensus because they were on a different basis. These 8 “Include Workforce Rebalancing Charge” while the consensus excludes them. This is the reason, the analyst count decreased by 8 from the consensus. Estimate data , unlike financials, is “what the market knew” approach. Since the data comes in bits and pieces it is possible for current values to be updated.

In other words, taking a snapshot and re-building can generate different values. The # of analysts seems to have been a mistake, but it was only a Compustat mistake, not “what the market in general knew” (there are other data providers).

-

From the image below the # of differences is greater after july 2012, than prior years, like 10/10/2009. That’s because 2009 was built from scratch as I mentioned before, not snapshotted. There are still differences because we bumped up the point-in-time to Sunday 3AM when recreating data to approx. match what we do live.

-

In the rebuilt data there are also a few changes we learned in this past 2 years with Compustat. For example their point-in-time active & inactive security list can be missing some fields in the past resulting in a stock missing then re-appearing the next week. THere’s a simple screen backtest that will show this problem. It has to do mostly with companies with no fundamentals, ie penny stocks, but I’ve spotted this problem with a few reasonable stocks. The new USA data corrects this.

In conclusion, our analysis shows slight differences. There are pros & cons to keeping the current USA or replacing it with the new rebuilt one. Our minds are to replace them. Some of the values we’ve snap-shotted do not even exist in Compustat anymore since current values are adjusted as data comes in. We also would like to add data-points, like EPS Median, but in order to do that we need to rebuild the whole estimate numbers to apples & apples. We do not feel that any of these variations should invalidate any robust system. It will backtest different, but overall it should not be noticeable.

The BETA server has Canada & the new USA. Please let us know what you think. We’re planning to launch and replace the USA data early next week.

NOTE: BETA is not updated daily. It has data as of this pas Saturday. Do not use it for current screens nor rebalances.

Thank You