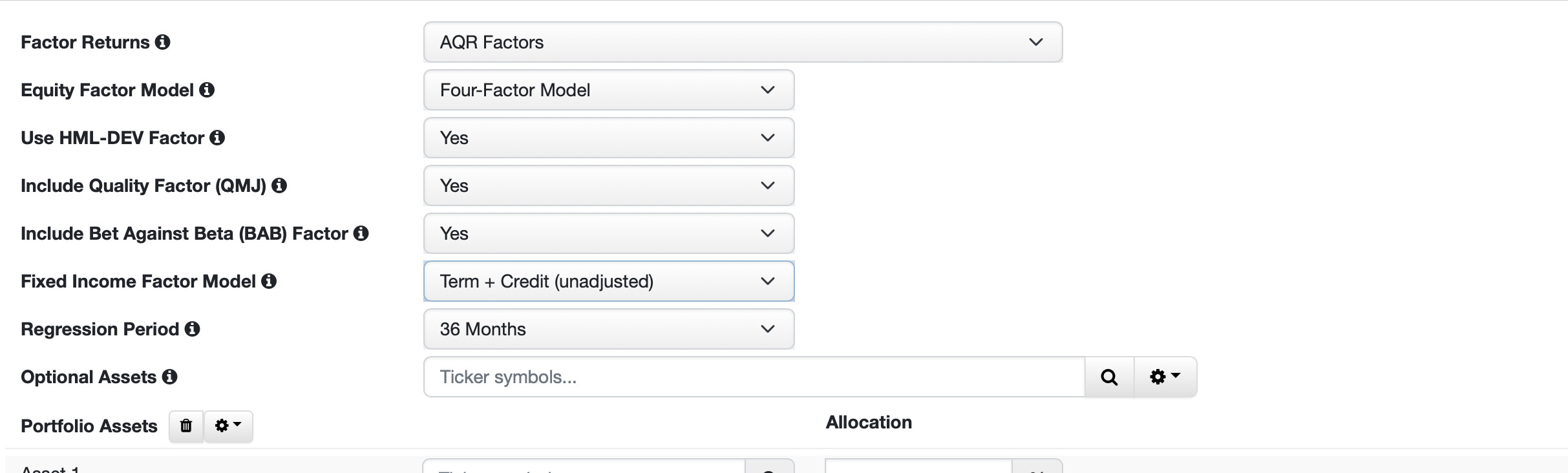

Yuval, I don't think P123 wants to lease one - though it'd great if it would. But perhaps the community could build one with help? I think creating betas for the many factors people unknowingly invest in here would go a long way to producing alpha and recreating trust in the simulations.

Once we have this, the ranking engine would provide returns not for stocks relative to each other, but relative to each other taking into consideration risk factors. Like, the ranking system now rewards beta depending on your time frame, as an example. I think it's reasonable to think approximate coefficients are better than nothing.

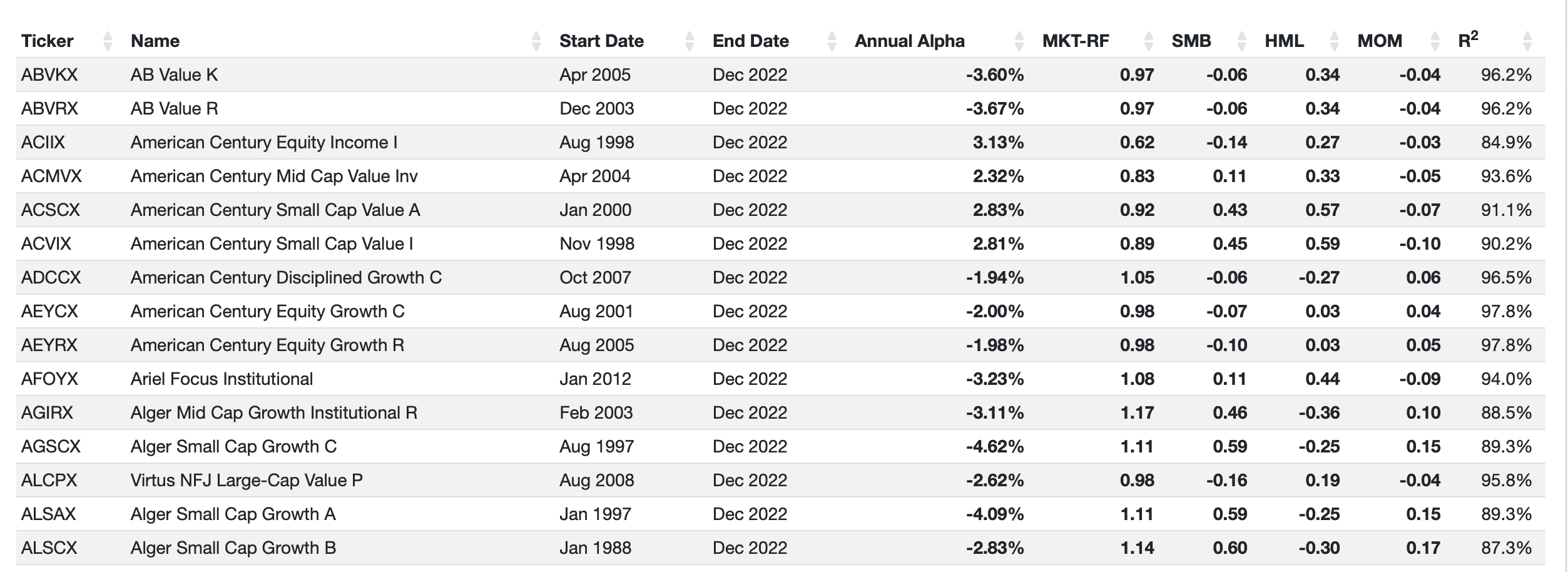

My thinking is we create generic factors and use the linest or similar coefficient (now there are more functions) to see how sensitive each security is to that factor. Then we can choose which risk factor we want exposure to (or optimize so that we don't have any). It would also allow us to study factor which have true alpha.

From goog top link on Barra (for those unaware).

The multi-factor risk model uses a number of key fundamental factors that represent the features of an investment. Some of these factors include yield, earnings growth, volatility, liquidity, momentum, size, price-earnings ratio, leverage, and growth; factors which are used to describe the risk or returns of a portfolio or asset by moving from quantitative, but unspecified, factors to readily identifiable fundamental characteristics.

I do not believe an answer saying we want to ignore this request in an effort to earn factor risk premia is a genuine. That is because you must measure that risk premia first and one cannot do that without a risk model.

Thoughts?