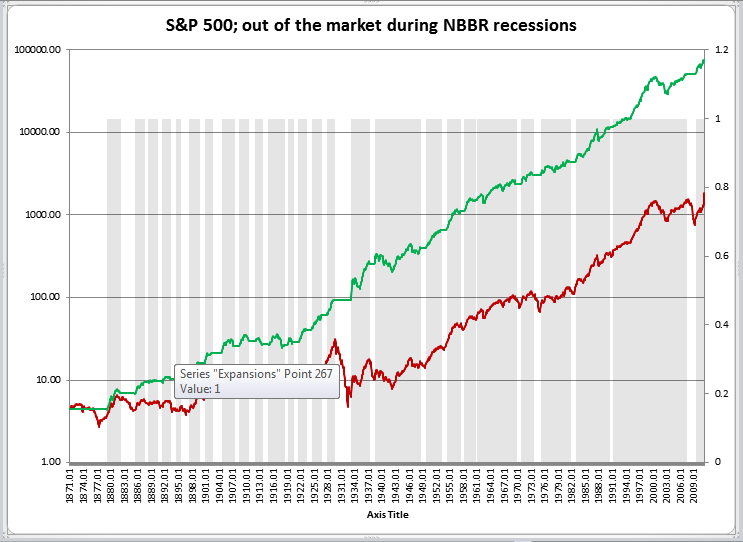

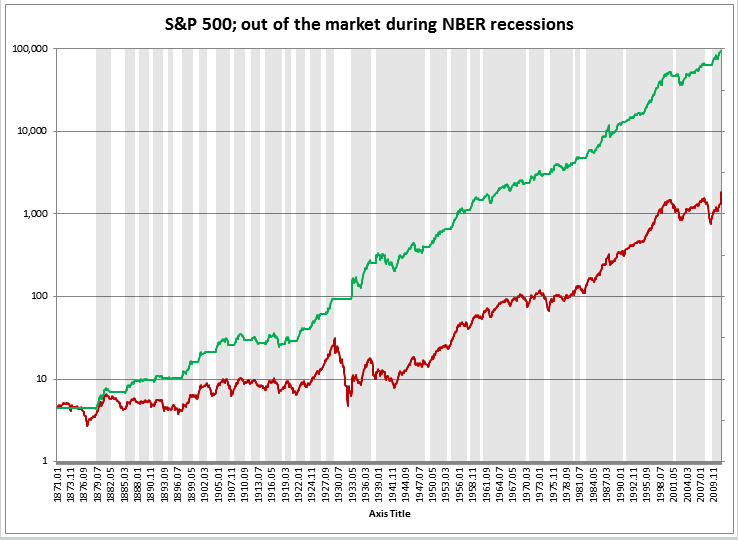

They say that a picture is worth a thousand words. The following chart shows what your returns would have looked like had you timed the market to be out during NBER official recessions. The cash was assumed to have earned 0%:

In an OOS study I drew the same conclusions:

www.portfolio123.com/mvnforum/viewthread_thread,7650#38851

The performance boost from acting right at the open was considerable for Small Gems, 1.5% /week improvement on average for trades of both types, but all ports outperformed variable slippage over the three-month period for both buys and sells. This study used (Hi + Lo)/2 +or- slippage for comparison, not (Hi + Lo + 2*Close)/4 +or- slippage.

In another study slippage degraded continuously all the way to close, on average:

www.portfolio123.com/mvnforum/viewthread_thread,7100#35263

The retail investor who trades at open and applies the stay-under-5%-of-daily-volume-average rule-of-thumb appears to have an unassailable advantage over large traders in that respect.

I do not know how this encouraging information can be accurately determined and measured for all R2G ports, then presented to subscribers, but this would help all parties if compared to the slippage associated with different trading approaches, i.e, open, mid-day, close. Many (?most) R2G ports are likely better than they appear, OOS.

My understanding is this formula is used for OOS, but (Hi + Lo)/2 is used for back-testing and/or simulation. I can’t remember where I read this. Please somebody set me straight, needless to say this would make a huge difference as (Hi + Lo + 2*Close)/4 +or- slippage appears to be the slippage benchmark most biased towards reporting lower performance, of all the ones discussed here.

too bad you only know that months after it happens. i.e. NBER declared the recession ended in june 2009, but they did not do this until September 2010, similar delays for the start of the recession in December 2007 was not confirmed until late 2008.

Ivanti,

Check out www.recessionalert.com . I forget which P123 user mentioned this site, but it seems quite useful

Hi,

There is any way to predict the market top, using market timing rules or when big guys are moving away from market ?

I am looking for swing trading strategies in P123,

- Buy stocks when dow/nasdaq is oversold,

- Sell stocks when dow/nasdaq is overbought

In, yahoo finance market news commentary,

Most of the time if market comes down, more fear in the market, they will say buying opportunity,

if market is going up they says more greed in the market,

- investors are selling short or stay in side ways without participating in the market and

- stock price rises without volume and

- stock price rises and money is flowing out of market.

There is any way to include the above strategies in P123 systems ?

I would like to stay away from market before market turn down using timing rules and come back when buying opportunities present after market oversold.

Thanks

Kumar

Chipper - It doesn’t appear that the NBBR recession graph has been of much use since 1980. The logarithmic graph shows 1987 and 2000 as wee little blips, where in fact the drawdowns were huge. So one out of the last three crashes/bear markets were picked up, but as was stated, the 2008 recession was not declared until long after the fact.

Steve

Chipper,

As others pointed out, here’s the NBER website (http://www.nber.org/cycles/recessions_faq.html):

Q: Typically, how long after the beginning of a recession does the BCDC declare that a recession has started? After the end of the recession?

A: The committee’s determination of the peak date in December 2007 occurred 11 months after that date and the committee’s action in determining the trough date of June 2009 occurred 15 months after that date. Earlier determinations took between 6 and 21 months. There is no fixed timing rule. The committee waits long enough so that the existence of a peak or trough is not in doubt, and until it can assign an accurate peak or trough date.

(In addition to the ones I mentioned above, earnings only data also misses getting you out of all the major DD’s of the 1940’s… so, it’s missed a lot more than it’s called).

You’re using an indicator that is ‘curve fit’ after the fact to determine peaks and troughs and is not point in time. The spreadsheet I sent shows raw monthly PIT earnings for SP500. Just take a look at it. SP broad earnings data typically gets you out and adds something in total, but it very often only works after most / all of the major DD has occurred. It can be used in combo with other indicators to give a more accurate picture, but it still looks like a poor standalone indicator. Curious if anyone else sees Robert Shiller’s data differently or finds interesting stuff in it they want to share?

Best,

Tom

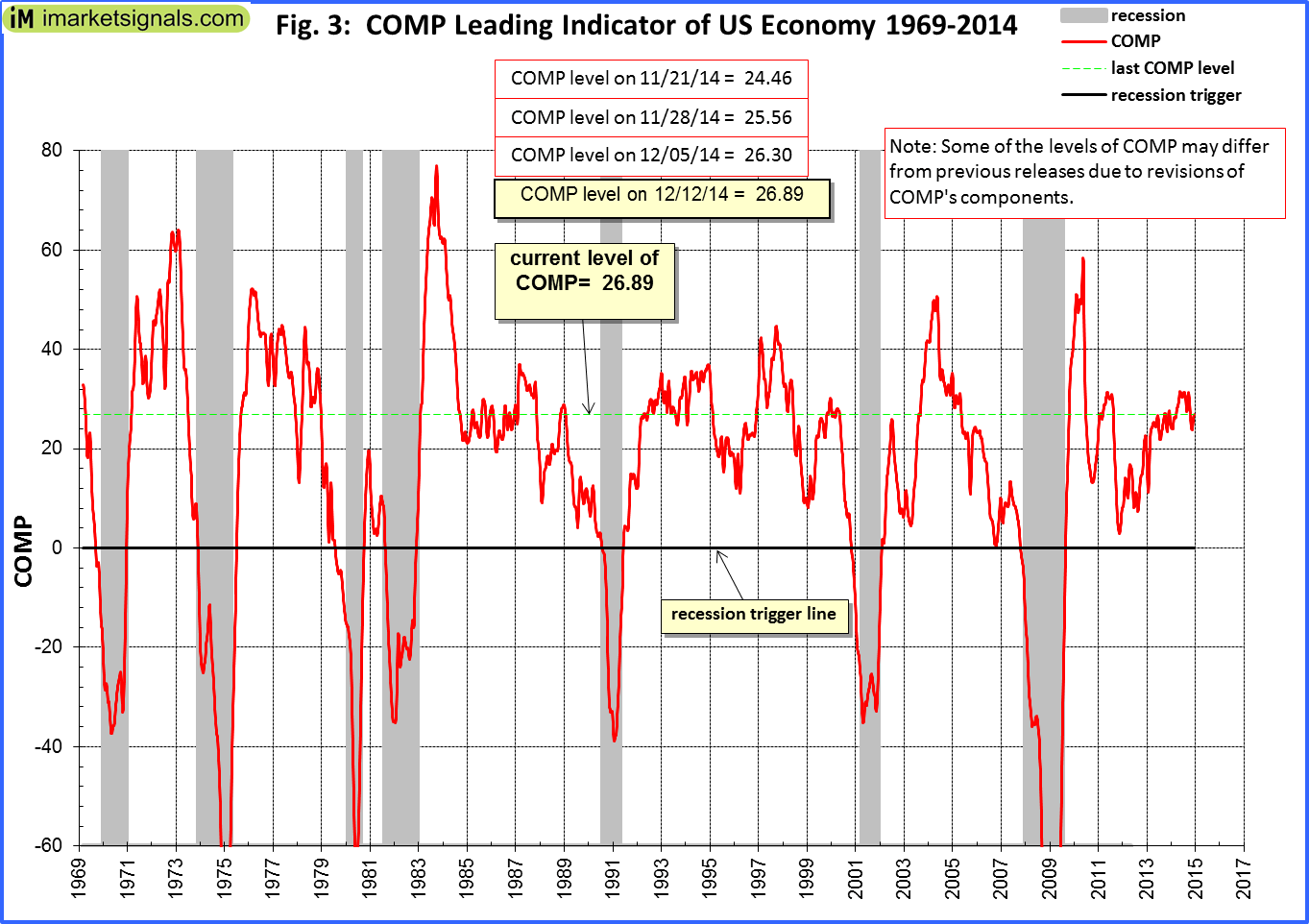

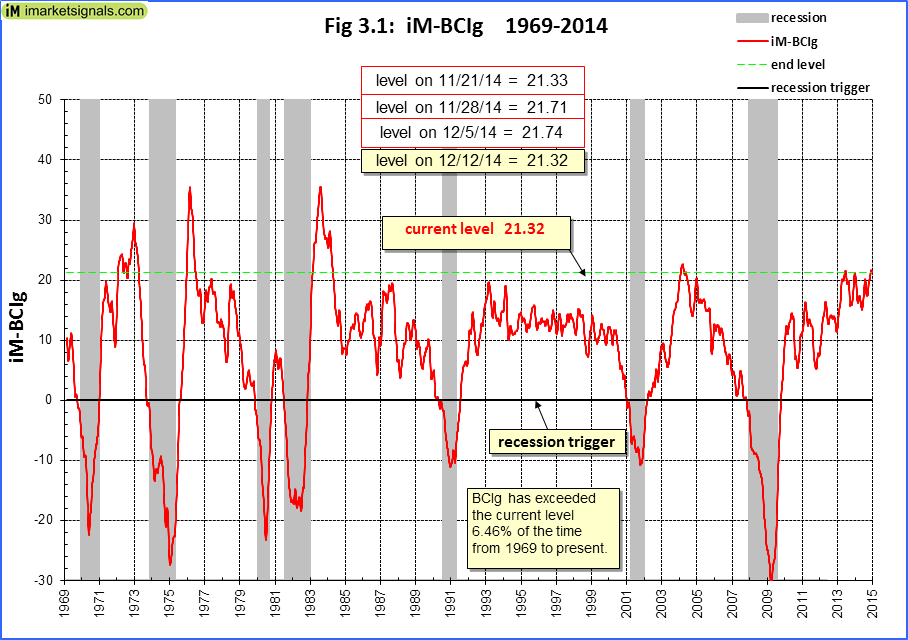

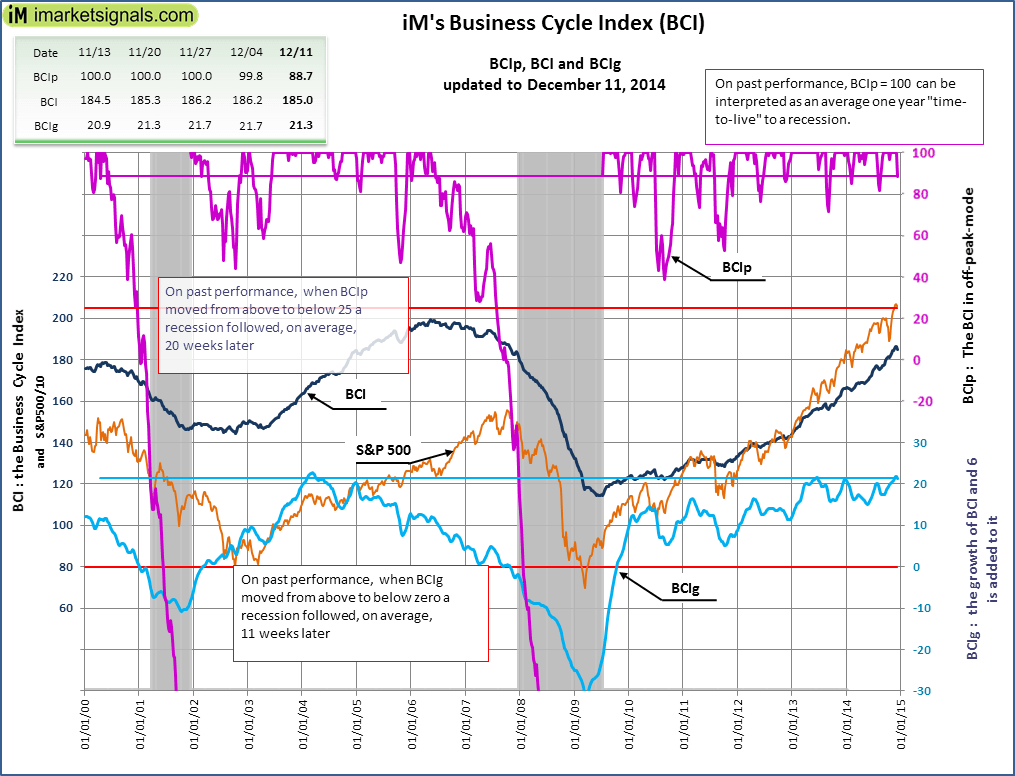

Chipper, it takes the NBER committee about 8 months to figure out the start and ends of recessions. Those dates are completely useless for market timing. We use the point-in-time COMP and BCI recession indicators which provide adequate warnings for recession starts when one should exit all long positions. Problem is that it is more difficult to pick a re-entry back into the market. Here are the most recent charts of the indicators. There is no recession in sight.

COMP: http://imarketsignals.com/wp-content/uploads/2014/12/Fig-3.-12-12-2014.png

BCIg: http://imarketsignals.com/wp-content/uploads/2014/12/Fig3.1-12-12-2014.png

BCI: http://imarketsignals.com/wp-content/uploads/2014/12/BCI-12-11-2014.png

Georg

Of course we cannot use the NBER for market timing. Sorry if I did not make that clear. And thanks guys for clearing that up.

The NBER chart is just proof of concept. Once we know what drives the stock market we can try to build a timing model to detects recessions in real time. I built one that I use for myself and in some of my R2Gs. Here is a backtest of a slightly simplified version of my recession indicator:

EDIT: Clarification - This indicator is not trying to predict the NBER but the market. Therefore there are differences in the dates between it and the NBER.

{kind=link}

{kind=link}

{kind=link}

BTW I have the NDR (Ned Davis Research) 2015 Outlook. Its not online - only available by subscription.

Email me directly and I’ll send it to you.

Brad

[quote]

Chipper - It doesn’t appear that the NBER recession graph has been of much use since 1980. The logarithmic graph shows 1987 and 2000 as wee little blips, where in fact the drawdowns were huge. So one out of the last three crashes/bear markets were picked up, but as was stated, the 2008 recession was not declared until long after the fact.

Steve

[/quote]Steve,

There are two important points that you are making and each one needs to be addressed separately. Your first point is of the three most recent crashes it only picked up the financial crisis crash but it missed the 1987 crash and it was only out of the market for a short blip in the dot-com crash. You know what? It won’t get you out every time (what will?) but it did help a lot even for these three most recent crashes!

BTW, the 1987 crash was not caused by a recession. Neither was the 1962 crash. But both of those recovered almost as fast as they went down and during those two crashes MA indicators would have gotten whipsawed too unless you were lucky. No timing system is perfect but even over the past three recessions it did seem to help! That’s why I like economic indicators better than MA indicators. I will grant you that the economic indicators would have missed 1940 while a MA indicator would probably have picked it up. That’s one time out of more than 14 crashes that a MA indicator would have worked better than economic indicators.

Your second point is that the NBER doesn’t announce recessions until long after the fact. That’s correct and therefore we need to use a different indicator that signals recessions faster. Luckily we have some good data and tools now to build economic indicators with, or you can subscribe to a service that is (hopefully) proven to be accurate.

Chipper - I agree that MAs are not the answer. I just have trouble using something that doesn’t seem to be relevant to my trading over the last 30 years. I personally experienced the 1987 crash (unlike the talking heads that seem to think the current oil situation is a crash beyond all others - what a laugh). I remember people at the time indicating that it had no tie to the economy but I can tell you it would have been one heck of a lot better sitting on the sidelines waiting to jump in rather than sitting through a 30% loss. It took over a year to recover, so a lot longer than the crash itself which was 1 1/2 days.

The blip I was referring to was the drawdowns, not the short time a recession was declared in 2001. Which leads me to something else I am having trouble with… what I am hearing about bear markets deriving from recessions. The stock market is a leading indicator. There is something called the wealth effect. When you have a bubble burst and the general population clams up (stops spending) because their investments are in decline, they no longer feel wealthy and they stop spending, resulting in a recession. So in all probability the stock market decline drove us to recession in 2001. The housing market burst probably drove down the stock market and led us into recession in 2009.

I honestly don’t believe it is as straightforward as saying there is no imminent recession thus there can be no bear market.

Steve

Well said Steve, agree completely.

Steve, I don’t know if bear markets cause recessions or if recessions cause bear markets or a little of both depending. But I do know that when earnings are shrinking it has often been prudent to hedge–if earnings are still shrinking. I also know that many economics theories would have been tossed out if we had better ones. The way the textbooks describe science, you would think that if a theory makes predictions that don’t come true then the theory would be discarded. Yet life doesn’t work that way. Many theories have predicted things that didn’t come true and yet those theories are still taught as gospel. So while I try to understand the theories when necessary, I do take all economic theories with a big grain of salt. In fact I believe that is your approach to creating trading models as well; to find what works instead of trying too hard to model the theories.

Hi Denny historically high leverage is causing whipsaws in technical-based systems. As selloffs begin they occur deeper than would otherwise be the case. This creates sell signals that often whipsaw. Keep an eye on systemic portfolio margin.

Recessions occur when an economy corrects excesses that have built up. Usually, these excesses occur somewhere in the business sector. But it’s possible they may occur in the financial sector as well, as we saw in 2008. The reason they are typically so hard to spot before the fact is that we aren’t always sure where we should be looking nor are we sure when an excess has occurred (i.e. how much inventory is too much, how much debt is too much, how high a commodity price is too high, etc.).

As to bear markets, they traditionally come ahead of recessions as markets anticipate the upcoming decline in earnings. Stock-market recoveries, too, tend to start ahead of business recoveries as markets anticipate the upturn in earnings by noticing the excesses being wrung out of the system. (If anything about a recession can be entertaining, it would be watching the gurus and talking heads; you can always spot the ones who really have no idea what they’re talking about – they’re the ones who are screaming, whining, ranting, bleating etc. because stock prices are soaring even though earnings aren’t and even though PEs, computed based on exceptionally depressed EPS, are sky high.)

One thing that makes things so tricky for market timing, even the widely used concepts that allow hindsight simulations to “avoid” the big 2008 drawdowns is the market is a discounting mechanism; it trades based on future expectations, not on what’s happening at the time. The other problem is that expectations don’t always pan out – case in point, the big 2011 drawdown that occurred in response to the Euro crisis, the Arab spring, the Washington budget mess, etc. – a collection of events that led the market to jump the gun and trade for a while based on assumptions of an upcoming recession, assumptions that turned out wrong and which caused the market to snap back later in the year.

That’s why it’s a heck of a lot easier to post a sim showing market timing success than it is to time the market ahead of the fact with real money in the real world.