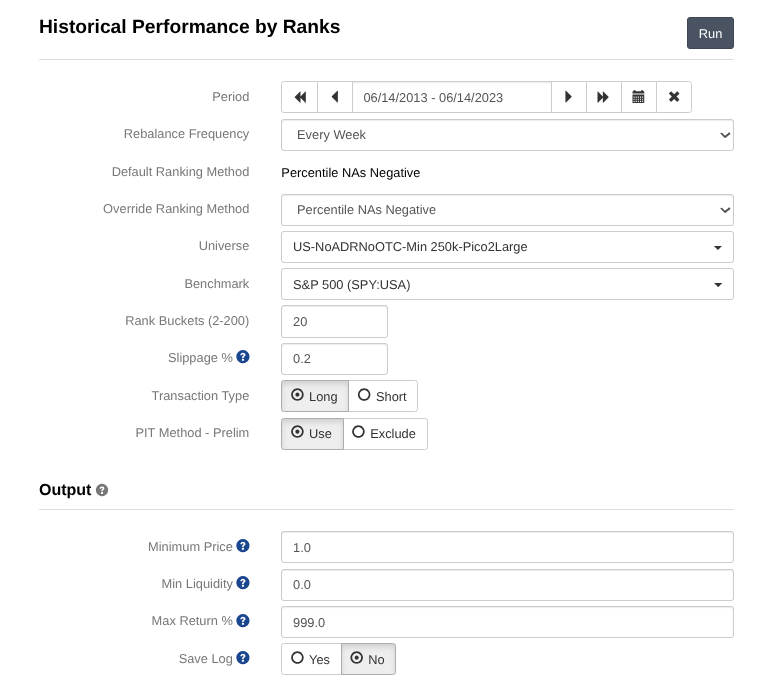

I'm using 15 based upon this post: How to Manage Your Portfolio to Maximize Your Returns - Portfolio123 Blog though I've also looked at 20, 25 which still deliver similar results. I have less success in sample with 50 which may be due to all kinds of reasons, but its still Sharpe of ~1.3-1.7. I've done my best to exclude the universe to only stocks I would be interesting in buying see my other post below which includes min liquidity etc.

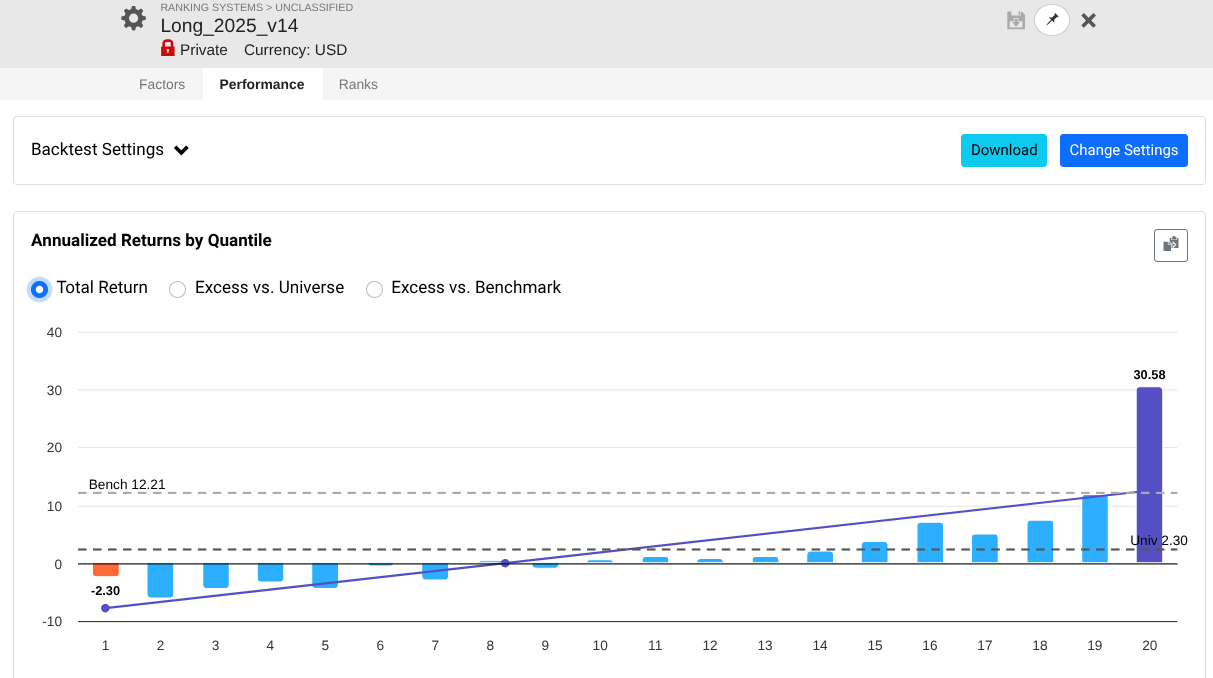

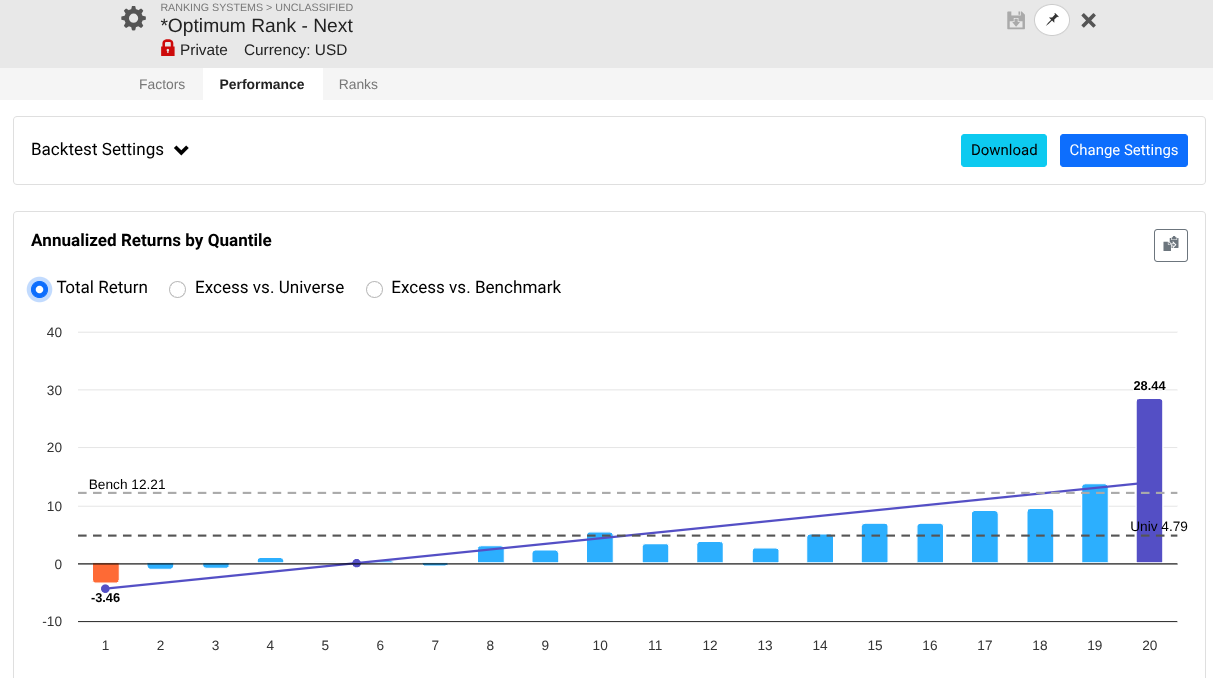

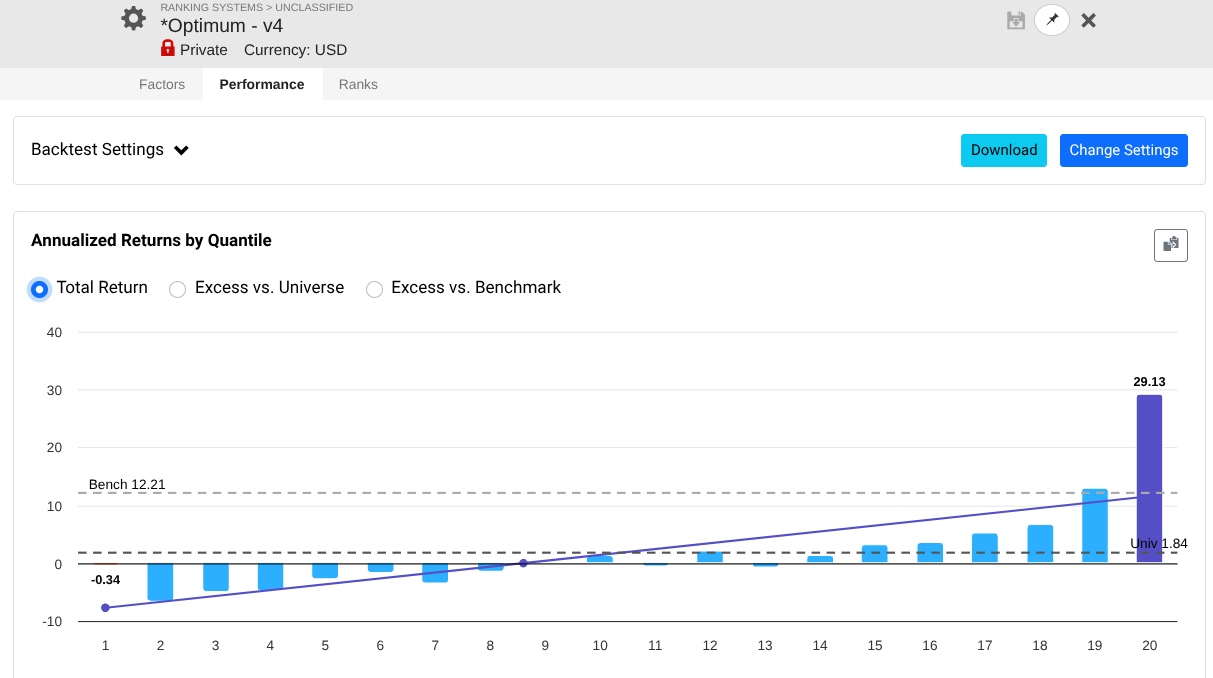

My generated rank lists for some of the above strategies are the following:

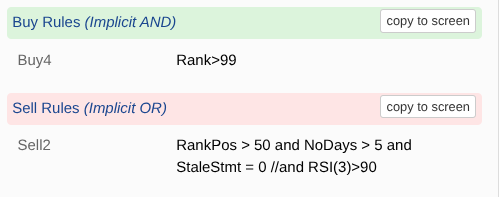

My multifactor equal weight ranking systems are what I use to avoid bad picks. And I use the following buy/sell rules:

I have also run Mod(StockID, 5) = 0...4) against the universes as described by Victor here: Reasons for 'Big Gap' in results between a ranking system and a simulated strategy my results are not as consistent as Victors with a range of 5% which is more than I'd like but still reasonable e.g. between 30% and 25% for bin 20, but still performs well as a RS.

Thoughts?