Large has been eating small for breakfast. Do you guys think small caps can outperform going forward ?

deleted

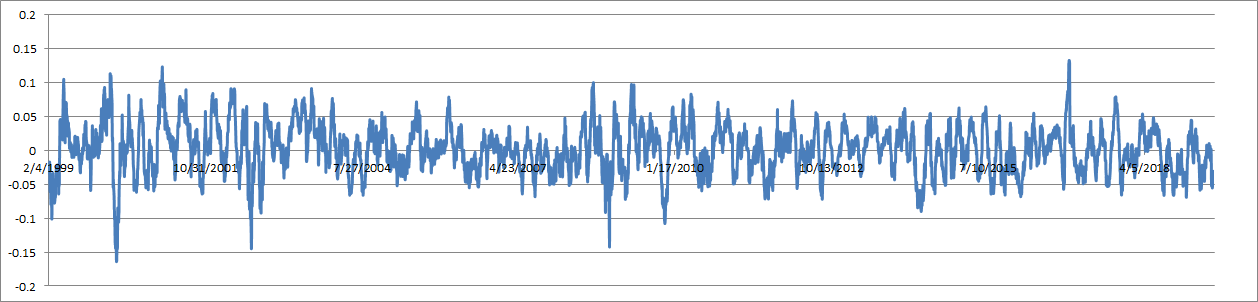

The chart below plots the monthly returns of IWC (microcaps) minus SPY (large caps). You’ll see there’s an extended period of massive underperformance from August 2018 to now. But the same thing happened in 2007-2008. And in late 2015 and early 2016. And 2004-2005. And much of 2017. Small caps will bounce back. They’re far from dead. We just don’t know when that will happen.

I recently got this email from Seeking Alpha:

Many exciting things are happening at SA these days, and to make sure you’re taking full advantage of your benefits as a contributor, we want to give you the latest and most significant updates:

…2. Undercovered stocks. We continue rewarding contributors for analyzing stocks that are widely followed but are lacking recent coverage. A dynamic list of the 250 most popular tickers that haven’t had recent coverage can be found at the bottom of the page here, and can be searched or downloaded for your convenience.

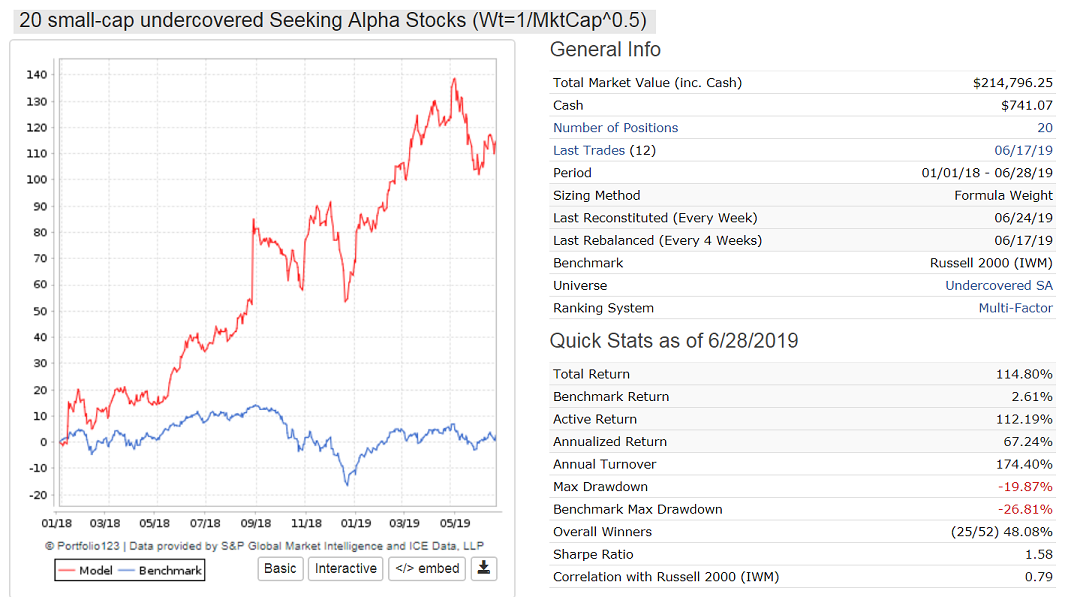

So I downloaded these stocks into an inlist and universe on P123. My assumption is that if nobody follows these stocks then there may be some hidden value here.

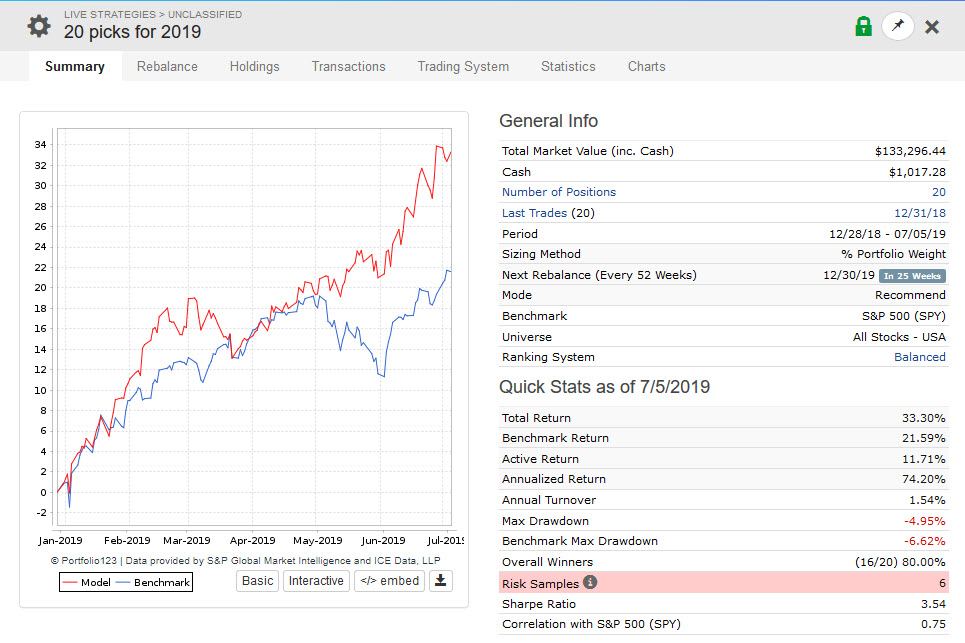

My sim selects 20 small/micro-caps with buy rules MktCap < 500 and AvgDailyTot(20) > 600000. Only sell rule is Rank<50 & NODAYS>25.

Weight is inverse of square-root of MktCap, and min weight set to 2%.

The sim from Jan 2018 shows a 67% annualized return (bench 1.8%), max D/D= -20% (better than bench) and low turnover of 175%.

Conclusion: Looks like trading undercovered stocks gives improved performance.

I don’t think it should be an argument of big versus small. Have models for both.

I also don’t think IWC is a great benchmark of microcaps. It’s cap-weighted for starters giving more importance to bigger stocks. And loaded with smallcaps and even some midcaps.

Still loads of alpha in microcaps and smallcaps. I mean, you have to wait through periods of nothing and under-performance. Like everything else. And they are not moving like the early stages of a bull market. But no complaints from me.

1 Like

Is there a better alternative? I’ve been relying pretty heavily on IWC but perhaps I shouldn’t be.

yes, I do ![]()

1 Like

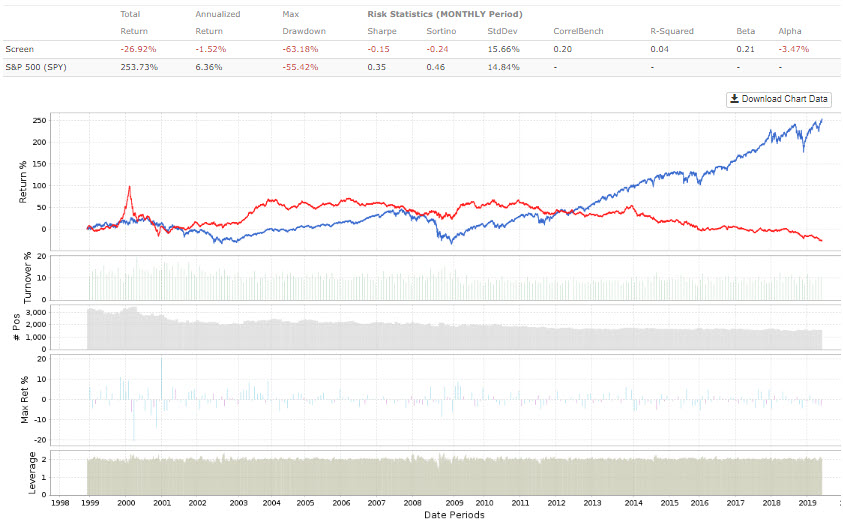

I mean, if your looking for a quick benchmark of stocks in the upper range of smallcaps to lower end of midcaps that seems to have heavier weighting towards healthcare…its not terrible. But when someone asks about microcaps I generally just perform a quick p123 backtest in the screener of everything between $50 - $350mm (or maybe up to $500mm depending) of equal-weight returns with a liquidity and price filter.

That probably has flaws as well but it is the approach I use since that universe is my benchmark as that’s I design models equal-weight in that universe of stocks.

Below is a chart of that base universe (long) versus the S&P 500 (short). As you can see, the microcap universe has under-performed since 2009.

Just for a little context, these are microcaps minus sp500 with a couple of filters I often use to weed out the higher risk names.

As you can see, over the past 12 months this universe has not kept pace with the sp 500. Largest divergence over the past 20 years.

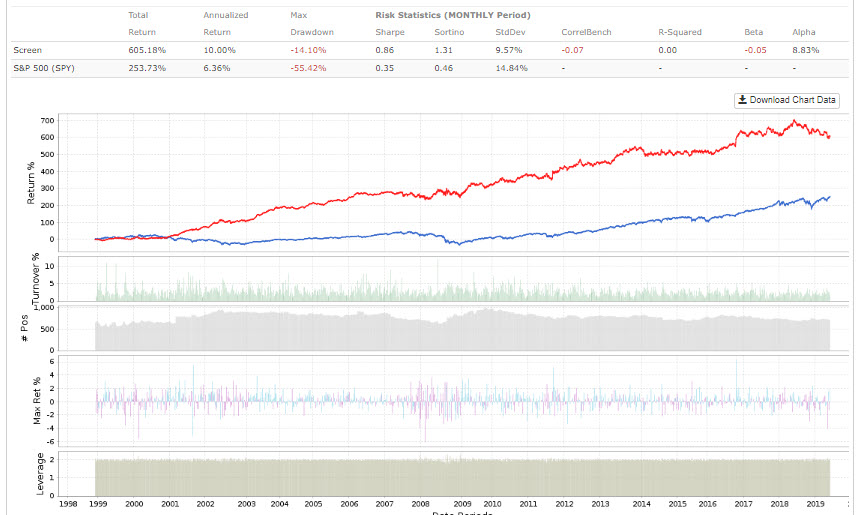

I look for positive free cash flow, increasing free cash flow and low short interest in the microcap space.

Yes. Small caps still doing well this year and you can participate…

https://www.portfolio123.com/port_summary.jsp?portid=1557492

Simple small cap screens have performed better than even the most sophisticated large cap screen over history due to information asymmetry. I think the informational gap is mostly gone. We’ll have to become more sophisticated to keep even with the power curve.

This is the same line I’ve been pulling for about three years now.

David, I think you may be right about the informational gap being narrowed but there is still the law of big numbers. If you have a billion dollar + fund you are not as likely to be looking at small caps as you just can’t put the size on you need to make it worth it. Even some individuals with larger portfolios have trouble getting past liquidity factors.

Even if the information gap were mostly gone (which I don’t believe), small caps and microcaps have many other inherent advantages for wise investors. See James O’Shaughnessy’s brief guide here: https://osam.com/pdf/Commentary_TrueMicroCapStrategy_Mar-2016.pdf

Here’s why I don’t believe that the information gap is mostly gone: I simply can’t find any good, reliable information about a lot of the stocks I invest in. There is little to no analyst coverage of many microcaps, and very little written about them on sites like Seeking Alpha. I don’t see any change in this over the past few years. Right now 45% of the stocks in the “All Fundamentals” universe have three or more analysts; three years ago it was the same percentage, and six years ago it was 46%. That leaves a LOT of stocks with very little coverage. I own a lot of shares of Volt Information Sciences (VISI; market cap: $95 million), for instance, and only one guy has written about them on Seeking Alpha over the last three years. Compare that to a smallish large cap like Alexion (ALXN; market cap: $29 billion), with about a dozen different knowledgeable folks writing articles about the company over the last year. The information gap is major.

1 Like

And that’s a great barometer, Yuval. It’d be great to see an integration between P123 and SeekingAlpha.

Been there. Tried that. Easier said than done. The closest we came was a plan to put stockscreen123 (integrated back into p123 to simplify the branding) into what was once a Seeking Alpha app store, but they required a back-end approach that would have put us in breach of our data license. I constantly tried to get them to appreciate the importance of idea generation (ways other than popular noise to help users choose to read about this stock as opposed to those others) but they didn’t get it, and most web sites (driven by ex journalists who see noise as the key to success) are in the same boat. Sigh . . .

Anyway, the information symmetry/asymmetry question is quite nuanced.

There is symmetry in terms of actual “information.” They report using the same 10-Qs and 10-Ks. They all have conference calls with transcripts readily available on company web sites and Seeking Alpha and elsewhere. They all have IR web sites and pretty much all have IR presentations which form the basis for many, if not most, seeking alpha articles.

In terms of information quality, there is an asymmetry but it goes toward more for small caps and less for larger companies. Small caps tend to have fewer businesses with more and better info on the ones they have. The larger the company, the more likely it is that you’ll get little or no digestible info on the actual business and things more along the lines of broad, bland overviews with companies that try to do better killing investors with information overload. When iI did the sub-micro low-priced stocks newsletter in 2010-15, information availability was fabulous. When I occasionally shifted gears to write up a large cap on Forbes.com, for example, I often felt stymied by my inability to get nearly as good a grasp on the companies as I had become accustomed to with the sub-micros. It’s like comparing a stock to an ETF. With the latter, you’re on the surface, or top down. That’s what it’s like to look at a large cap vs. a small cap. With the latter, you’re better able to get a serious bottom up view. The main exception are the large caps we deal with in life; , sbux, amzn, mcd, etc. But there, the extra info is of little value since everybody else also has it, and it might even be a handicap since the temptation to act on emotion or bias tends to be greater. For me, for example, I have an extremely deep knowledge of Zillow and think its the worst pile of sh** on this or any other planet, but I’m comfortable owning a housing ETF (ROOF) that has a good sized position in Zillow; I’m ok with the idea of being protected from my own bias, which may be leading me to a bad opinion on the stock.

To the extent there’s an asymmetry with more going to large, I think it’s an asymmetry of opinion. The greater number of analysts and commentators are all working with the same source material, presenting the same background info, explaining the same sets of numbers, etc. If I look at Seeking Alpha and see, for a tiny stock, no article since 2014, no problem: The IR Presentation and conf call transcript will still give me most of what would have been in an article had a newer one been available. The differences tend to be in the opinions each writer draws. In large cap, there’s more opinion because there are more people writing and talking and the reason for this, I believe, is what brett said about the law of large numbers.

There may be information asymmetry, indeed. Insiders, for example. Institutions that process data that I do not have access to: e.g., satellite images of mall parking lots. Maybe some early information from credit card companies around Christmas—I guess (maybe)—but that type of thing.

But everything I use in my port is publicly available.

I do not see how I take any advantage of information asymmetry if I use no discretion with my port. If there is asymmetry, it is information that SOMEONE ELSE POSSES (AND I DO NOT).

True, there may be some lazy retail investors. But there is no asymmetry with the institutions is there?

Am I missing something? Are there other sources of revenue: E.g., behavioral? Too much emphasis on information asymmetry?

I might use a better analysis but any information asymmetry is NOT IN MY FAVOR—at least with regard to institutions–EVER.

-Jim

So this is what asymmetric information looks like:

[quote]

…business transactions, corporate data, government agencies, etc.), and sensors (satellites, geolocation, weather, CCTV, etc.). Some popular satellite image or video feeds include monitoring of tankers, tunnel traffic activity, or parking lot occupancies…… Before Exxon Mobile reported increased earnings, before its market price shot up, before analysts wrote their commentary of their latest filings, before all of that, there were movements of tankers and drillers and pipeline traffic. They happened months before those activities were reflected in the other data types.

de Prado, Marcos López. Advances in Financial Machine Learning (Kindle Locations 1360-1366). Wiley. Kindle Edition.

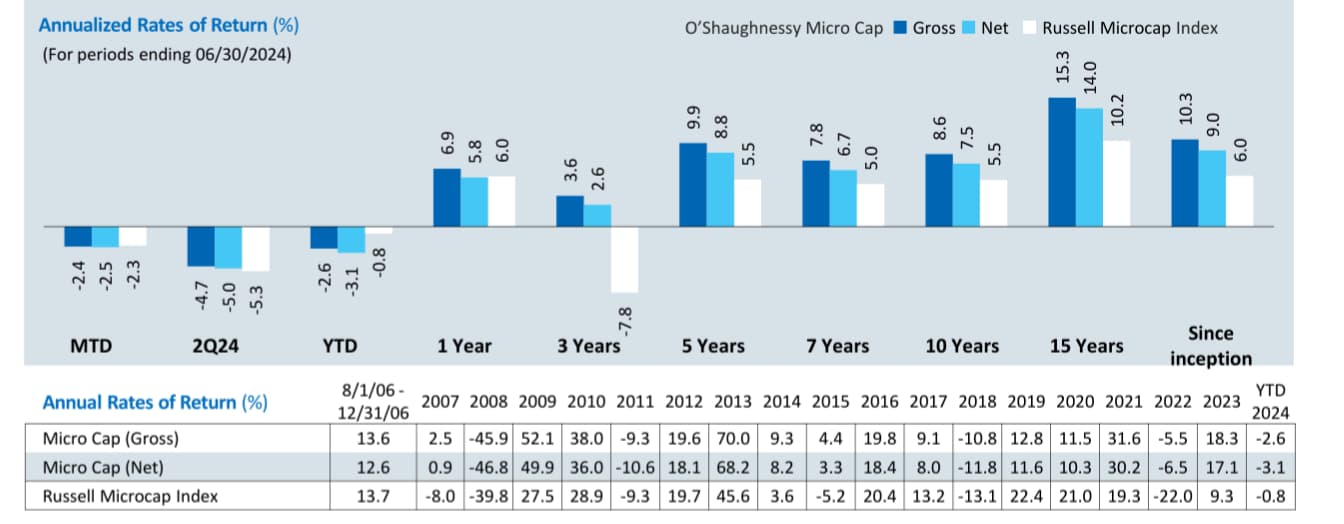

The returns of his microcap strategy:

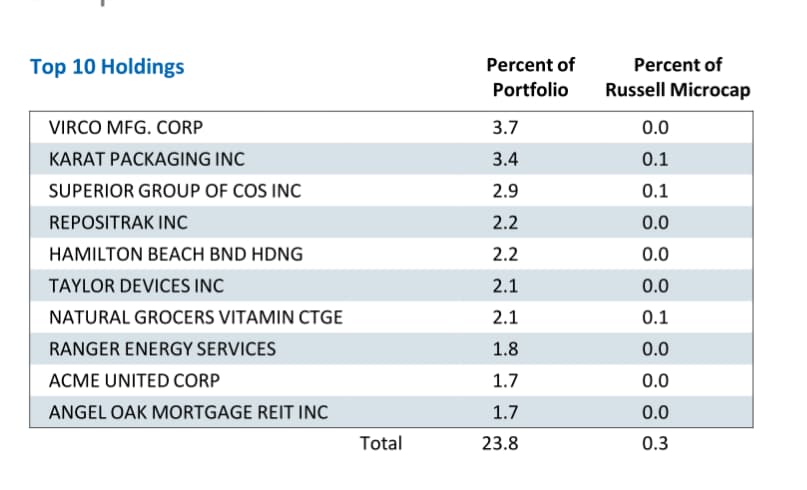

I found some familiar names in its holdings:

It heavily relies on Shareholder Yield:

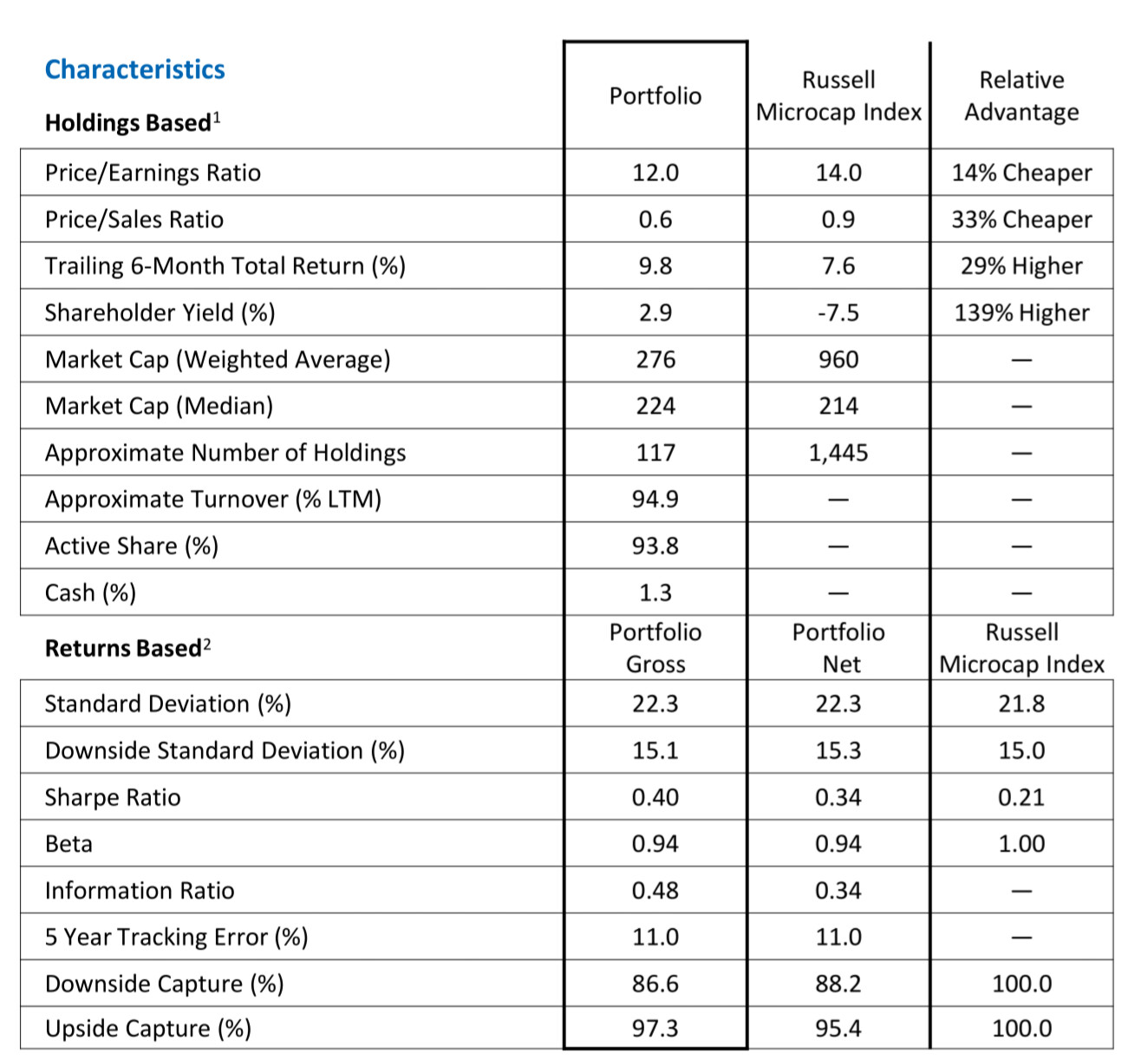

Also, you can find that the many stocks in the microcap universe are being diluted a lot.

The beta of the screen's performance is only 0.21

I think there must be something wrong

Good point, which is why I say large cap stocks are a billionaire's game.

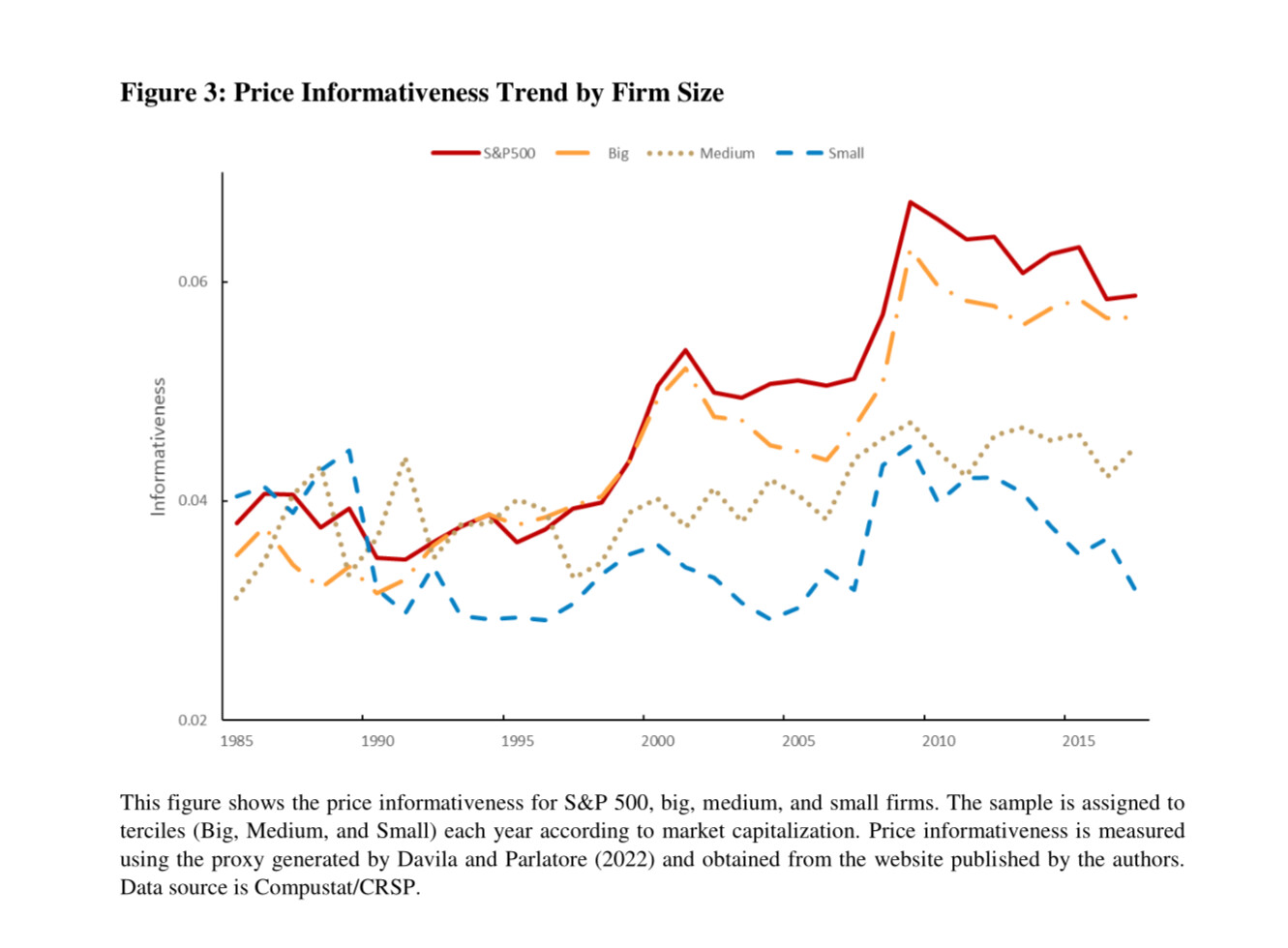

We find that as large firms gain market share, information production resources, including the attention of financial analysts and institutional investors, are shifted away from small firms, even if the size and business fundamentals of small firms remain unchanged. The loss of information production reduces stock price informativeness. The evidence points to an increasing market concentration that not only favors large firms but also leads to a skewed distribution of information production resources, thereby worsening the information environment for small firms.

2 Likes