Yes, financially, they tend to have more of a safety cushion – to a point.

Many small companies have much stronger balance sheets than many realize and actually, small size contributes to that. The smaller the company, the more concern the CFO has with such things as meeting payroll, paying utility bills, paying suppliers etc. leaving less time and energy for “balance-sheet management.” The large-company edge tends to come about in that they have more levers they can pull in the capital markets if push comes to shove. Also, larger companies are more likely to benefit from internal diversification (even within what appears to be a singular GICS classification, it’s possible for a company to have many different kinds of businesses with different profit characteristics. The only way to see that is through the 10-k business descriptions and trade sources.

So regardless of what how historical bets may tabulate over the course of any specifically chosen sample period, looking forward, when all probabilities are on the table, big companies have a leg-up in terms of risk mitigation. That can always be and sometimes is cancelled by company-specific matters, but pending further information, the default assumption is that bigger means less risky.

Likewise, although company-specific circumstances can always change things, the default assumption in that bigger companies have more stable profit streams. This is a function of operating leverage. The bigger you are, the more thoroughly fixed costs are covered. Conversely, the smaller the company, the larger fixed costs loom as a percent of total expense, thus equating to a presumptively more volatile profit stream, and that suggests a default more-volatile-stock assumption. Once again, this, not historical price-based data, is what future-oriented betas, standard deviation, etc. is likely to be about.

Continuing, we saw in the Value portions of the on-line seminar that higher quality equates, all else being equal, to higher ideal (warranted) PE, PS, PB, PCF, etc. This has implications for out-of-sample-oriented modeling.

First, we can choose to pay up for stability (i.e. higher probability that historical trends will persist). Many do just that.

Second, we can look for information arbitrage opportunities. Big-cap stocks are often seen as dull and offering little opportunity while smaller and super smaller stocks are favored for their high volatility high risk characteristics (i.e. the larger probability of positive outliers). We see that in the forums all the time, and we certainly see it all over the place in Smart Alpha, where designers and subscribers are hypnotized by the stupendous simulations that can be crafted among tiny stocks. And we’re not the only ones who think this way. But that can present opportunities. If big cap stocks are less appreciated than they should be, on objective grounds, well, you know . . .

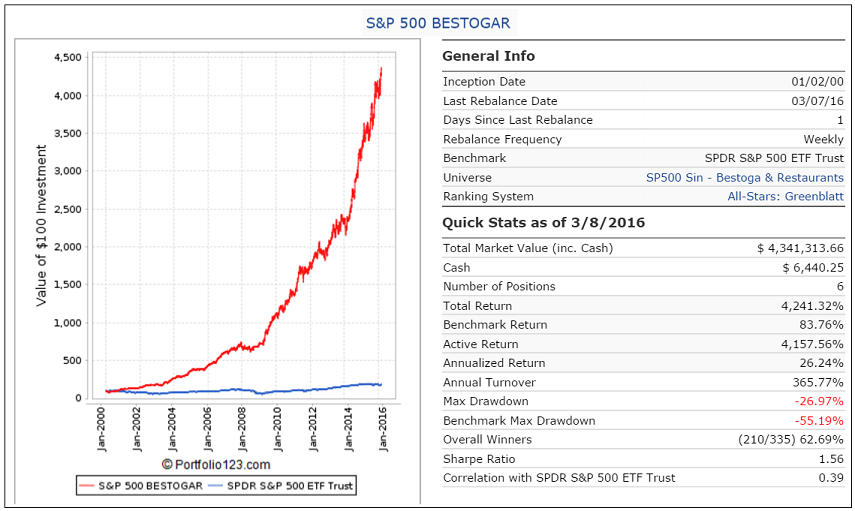

This is why the easiest way to dampen the BESTOGA sims is to aim at a broader and/or smaller universe than SP500.

And by the way, SP500 and R1000 are not always equivalent. SP500, by virtue of its “cultural” status often attracts a lot of non-fundamental park-it-naively money. This, too, plays a role in volatility.

This doesn’t mean you can’t win with a small/micro BESTOGA strategy. There are some great opportunities down there. But because you’re stripping away the benefits of SP500 membership, you’ll have to work harder in screening/ranking to uncover them.

What’s the risk to an SP500 BESTOGA strategy (aside from the obvious market risks)? One ever-present one is valuation, that too many investors identify and pursue the opportunity and bid the stocks up to levels that bring volatility onto the table. I think it’s a low probability scenario since people are in love with swinging for the fences chasing bigger upside. Probably the one that bears more watching is at the company level, i.e., whether antsy action-craving managements go nuts with unwise investments and/or financing wizardry, in other words, event risk. If you expand BESTOGA to restaurants, this may become more a concern and the presence of gaming certainly puts it on the table. Complacency is also something to watch for as brands like Budweiser and Coca Cola find themselves having to fight harder than ever for shelf space and consumer affection.

Personally, I like the BESTOGA approach and think the model has a good chance of being successful. But you no matter how much anyone loves any strategy, one should always have a doom and gloom scenario in mind, since complacency is our biggest enemy. We can’t be intimidated by baggage; 100% of companies have it. But we do have to be aware of it.

Anyway, this is a sample of how I look at strategies.