Greetings all,

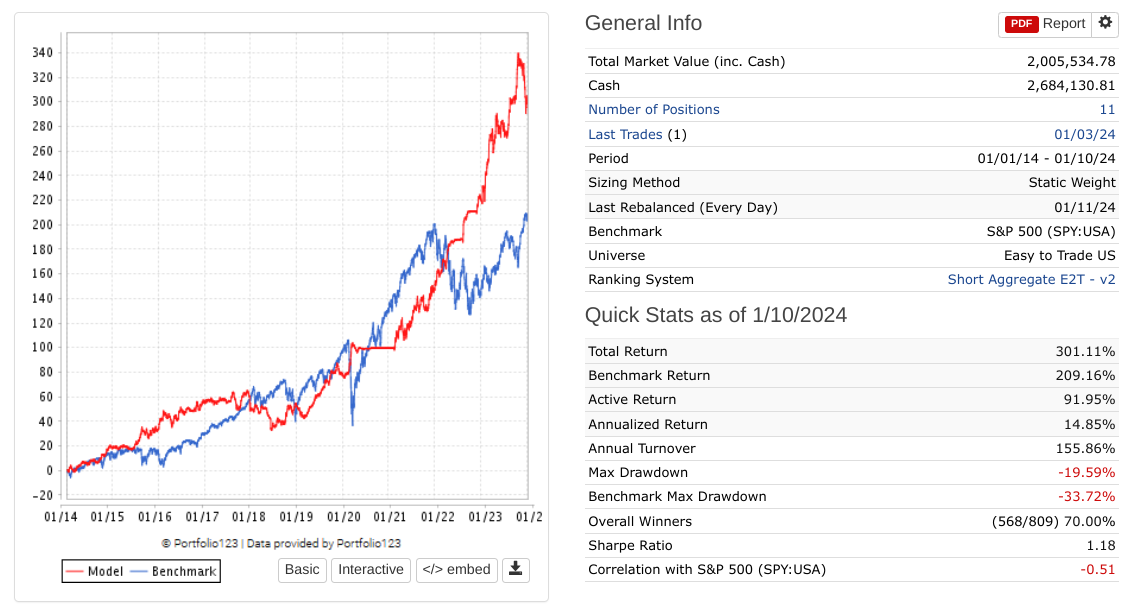

Most topics on the forum involve systems for going long. Hence, it is pretty easy to get a good idea of what returns to expect when building a ranking system or a simulation for these type of strategies.

But when it comes to to the opposite side of the spectrum, I have a harder time finding relevant information on what a realistic result would be.

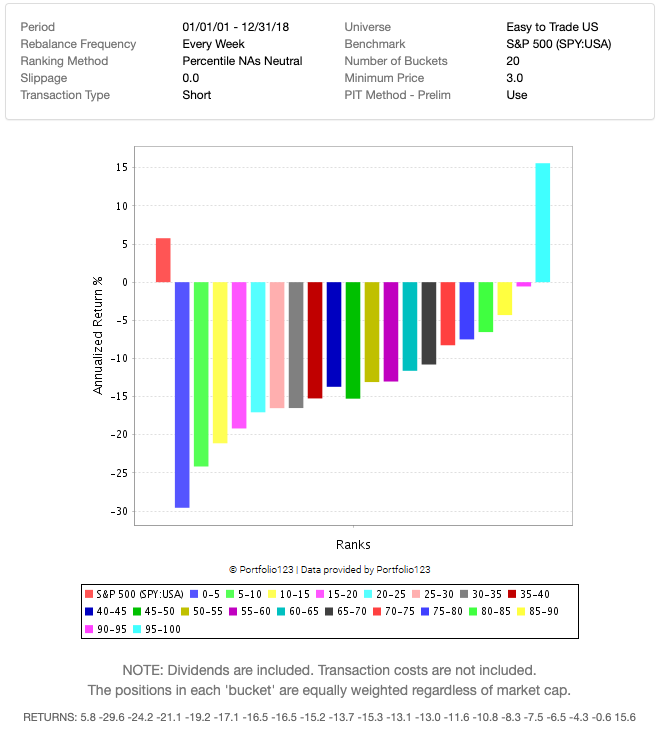

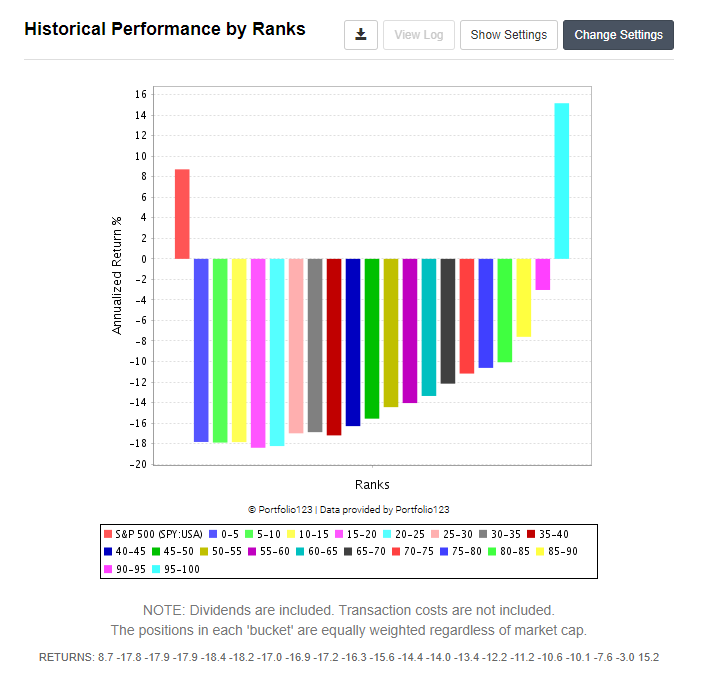

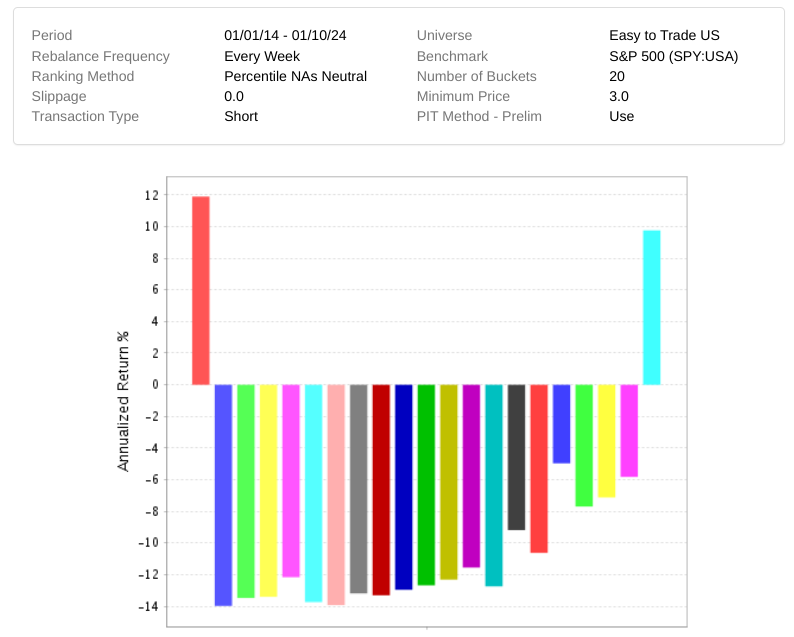

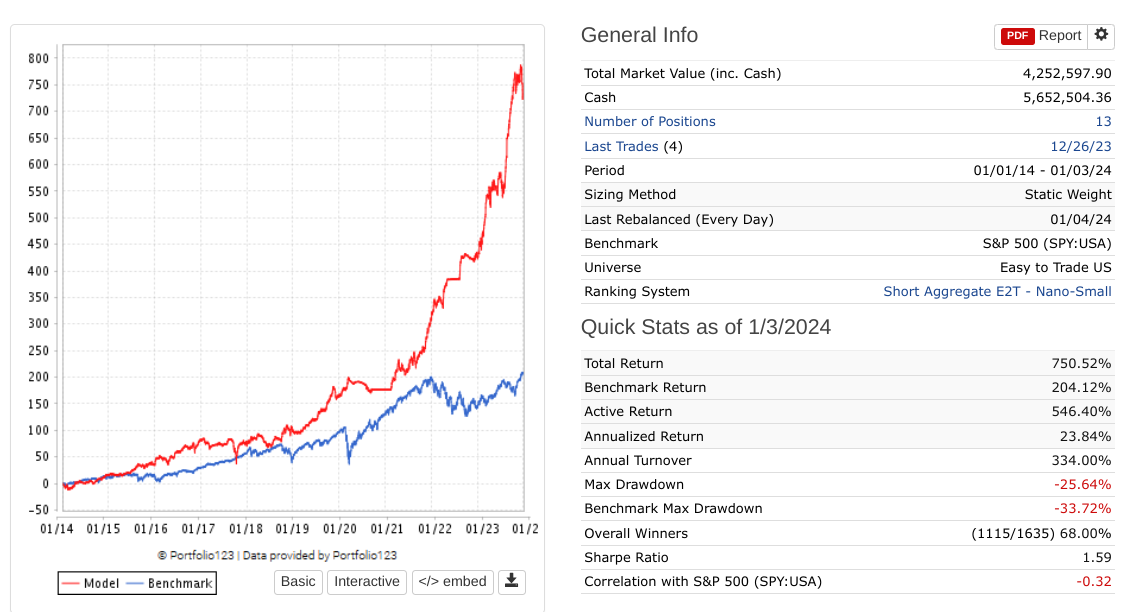

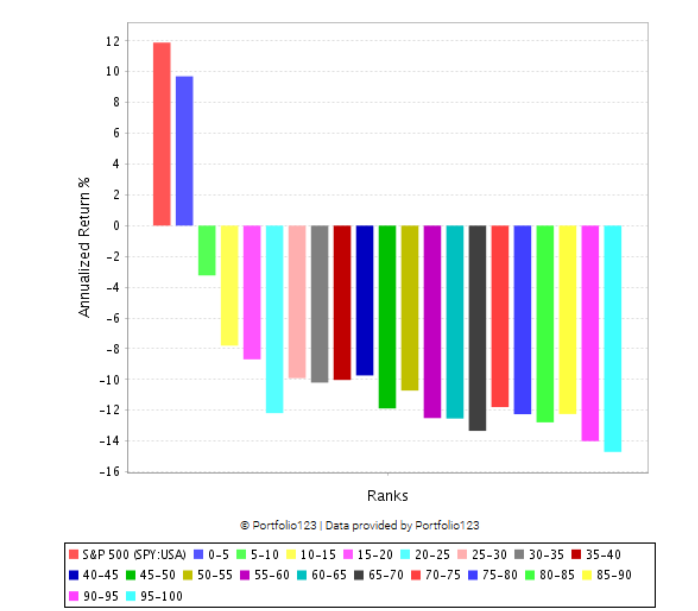

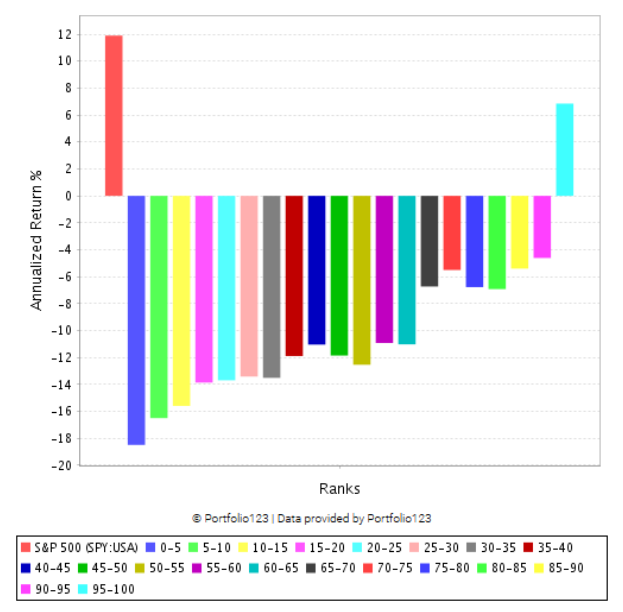

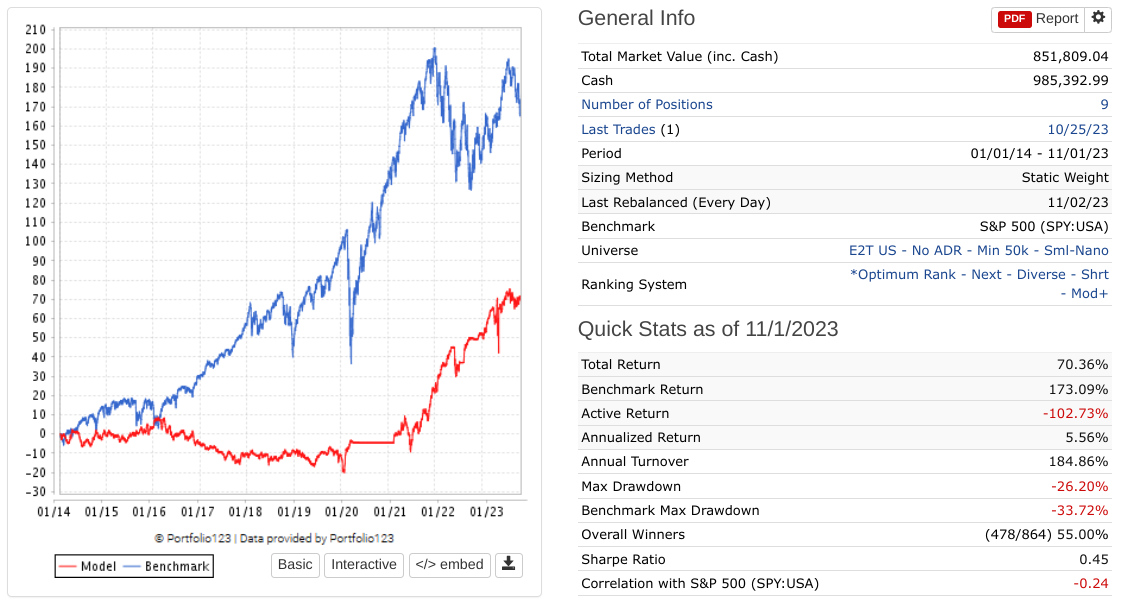

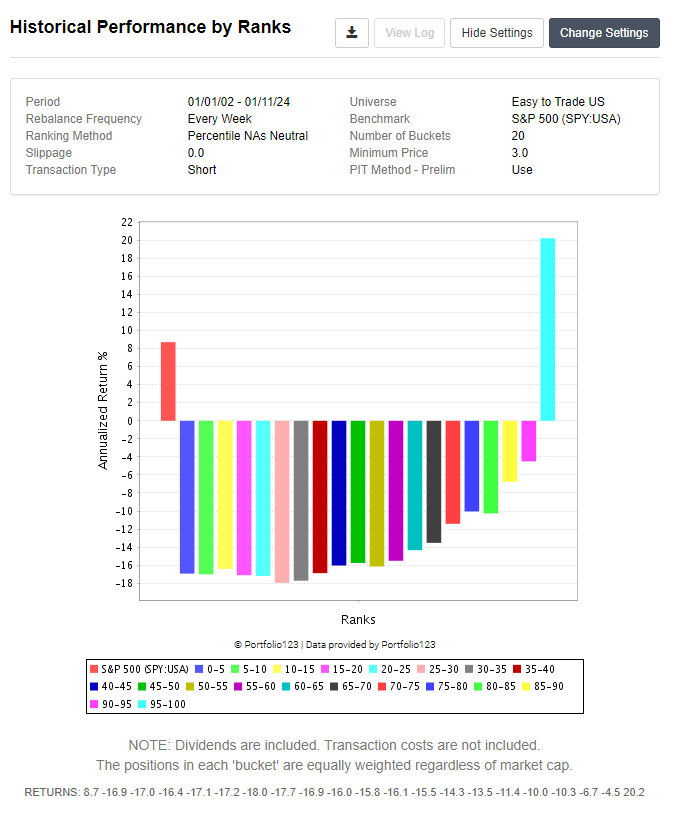

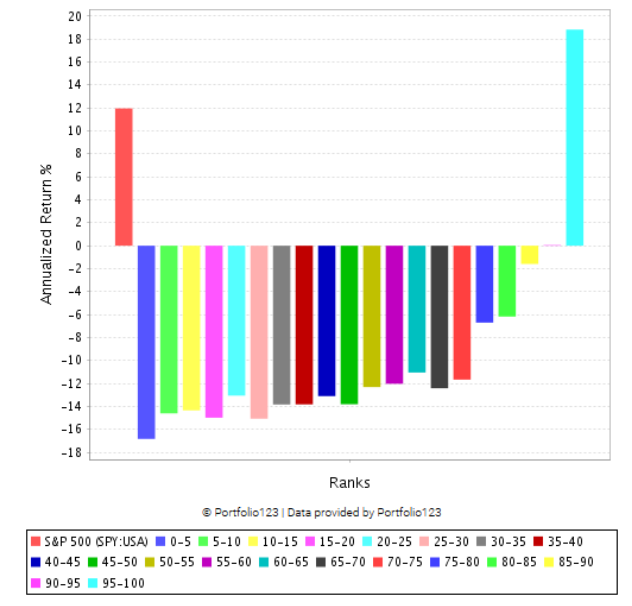

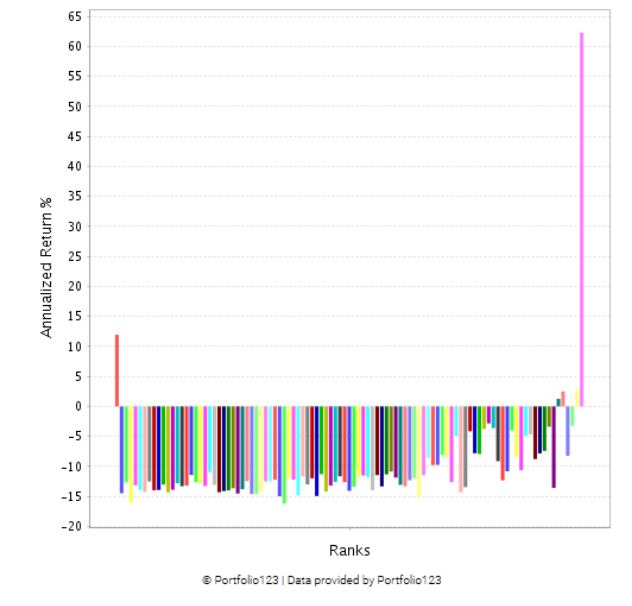

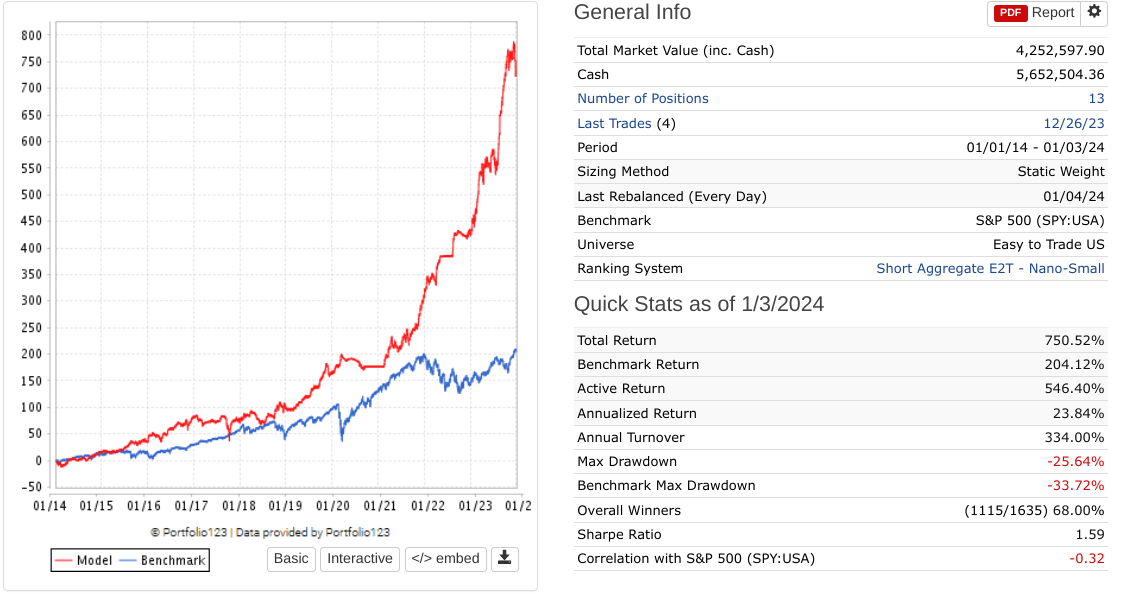

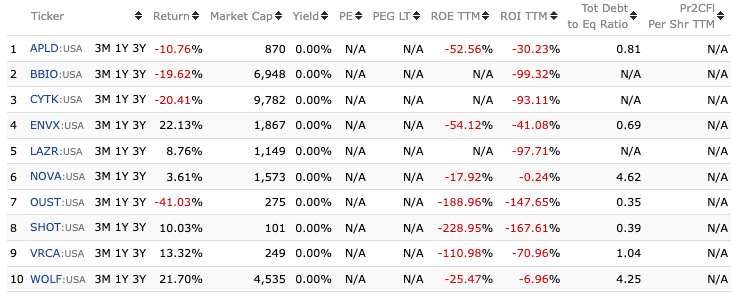

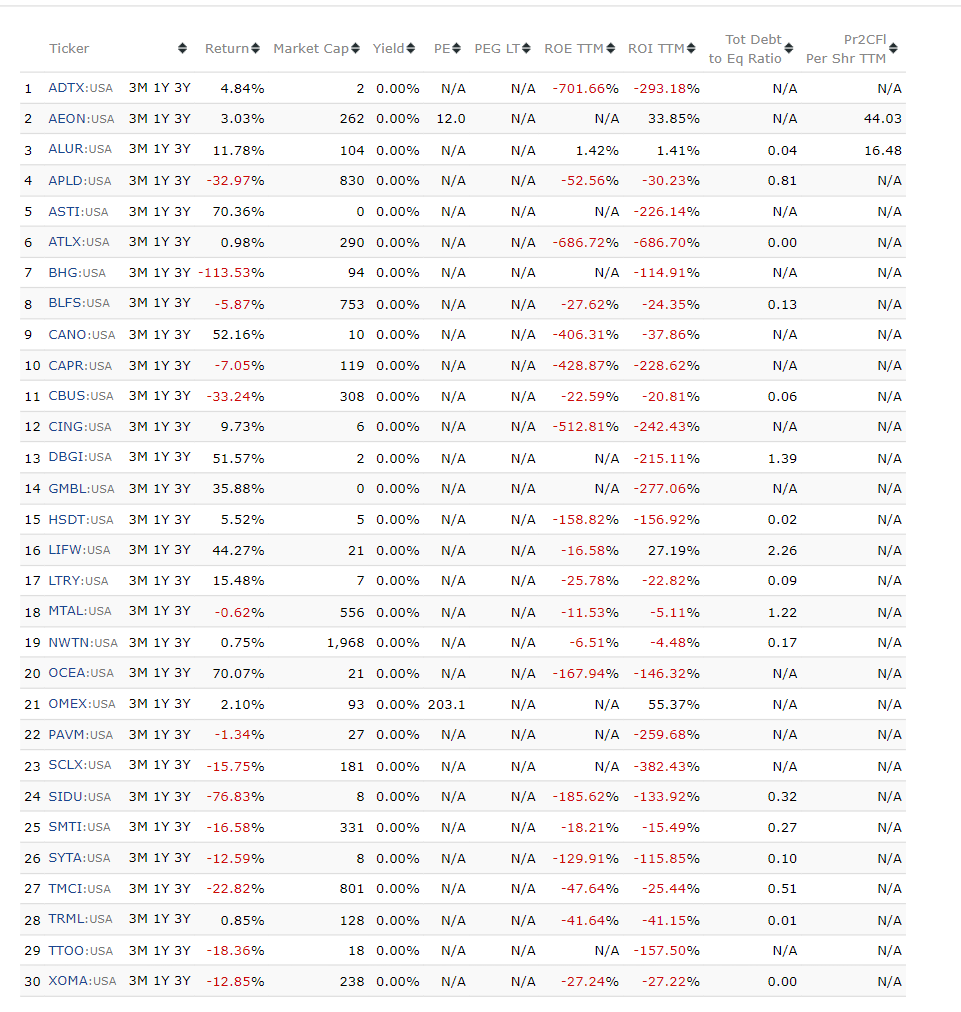

For example, let’s say you build a ranking system that has the goal of getting an as low as possible return for the top 5% bucket, would -20% be a roughly good aim (using the Easy to Trade USA Universe)?

Furthermore, In terms of the amount of factors to use, I have noticed that price volatility seems to be a factor that has a way bigger relative impact on the outcome of the ranking systems than any factor I have seen in my long only systems. Excluding it from the system drastically changes the performance of the top buckets. For any long only ranking system I would prefer to ‘diversify’ by using more factors, instead of relying so much on one.

I was wondering if someone would like to share their thoughts on their experiences with their systems for going short.

Kind regards,

Victor