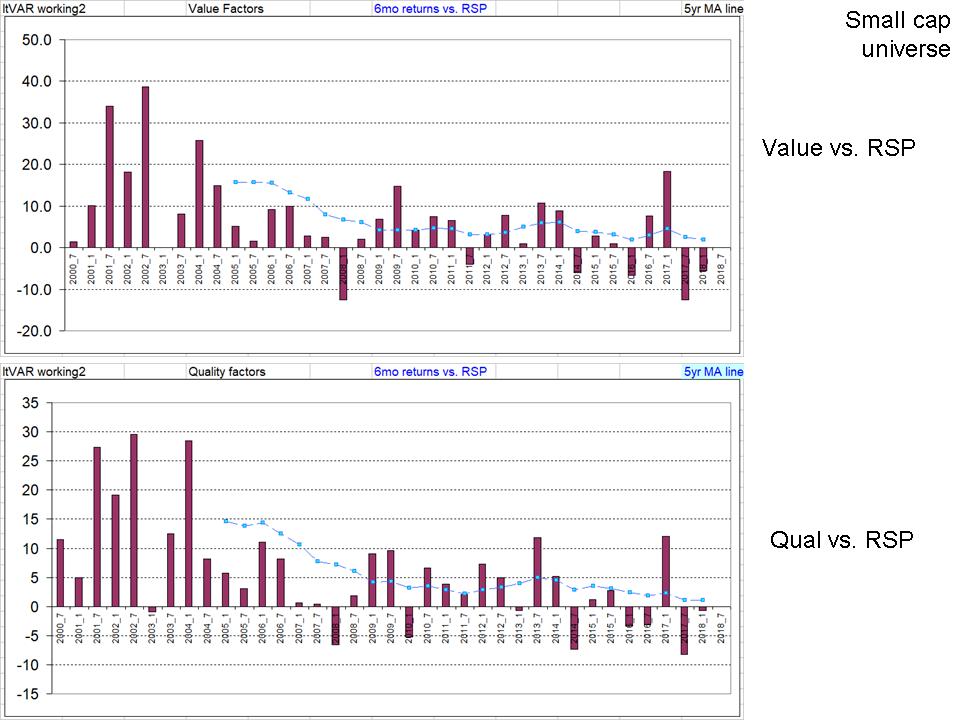

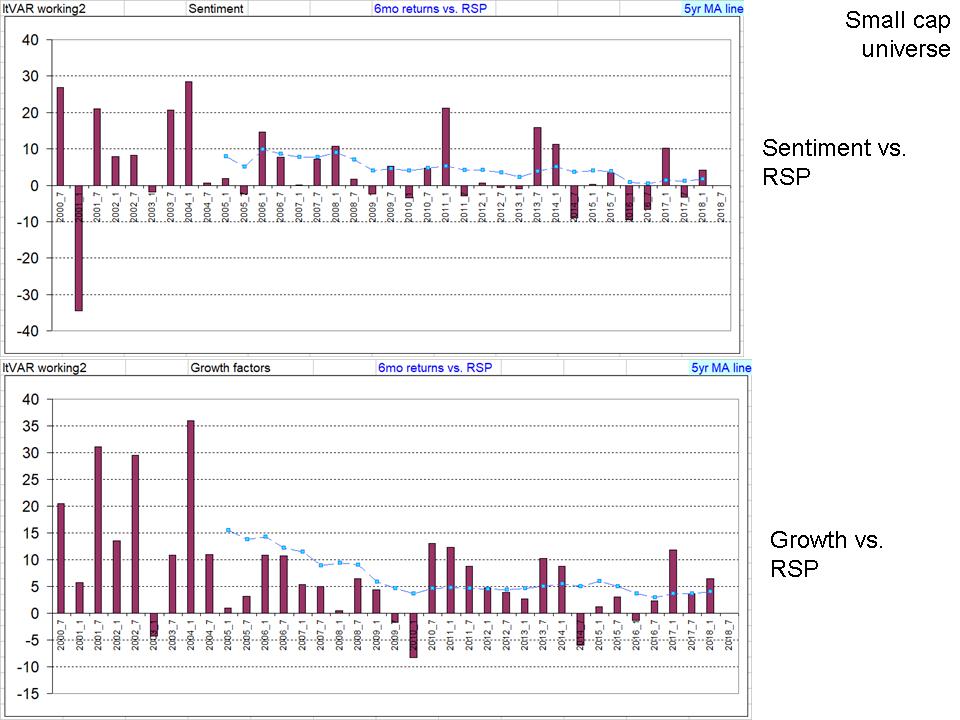

Decay is real, but it is also definitely related to size.

Marc’s article motivated me to respond to questions regarding the decline and invertibility of factors. For these questions, I used the Fama-French datasets.

l found that value, profitability, and investment anomalies have decayed to essentially zero over the past 55 years, judging from the linear trendlines. While this decay has not occurred as rapidly as would appear based on the 20 years charts, it has resulted in the complete decay of the HML (i.e., 2 sized-ranked portfolios sorted by book-to-market) anomaly, which is often used a proxy for “value”. For example, the alpha on the 3-Factor equal-weighted HML declined by about 13 basis points per year since 1963. But 13 basis points times 55 years is about equal to its expected return intercept. Moreover, the rate of the decreasing appears to be increasing (from 1926 to 1963, there was essentially no decay in HML).

In addition, the trendline on the alphas of the return-based anomalies (i.e., momentum and reversion) portfolios have also declined to essentially zero, and much more rapidly so.

If current trends persists (and are assumed to be linear), it is conceivable that factors could indeed invert. I suspect, however, that the trends are not linear, but rather exhibit a power/exponential declines curves which are over the long term drawn to zero. While factor inversion could come about as a result of demand over-crowding, I doubt there is a reason why relatively low-priced stocks and outperforming companies would persistently underperform.

My intent is not to sow despair, but rather to set my own realistic expectations regarding just how difficult it is to generate alpha. Excess returns come only to those who either have some sort of arbitrage or other competitive advantage. For retail investors, since small cap stocks are more resilient to decay, one advantage might that our own small sizes allow us to gobble up pricing inefficiencies that institutions ignore.

FWIW:

I believe that factor decay is attributable to the leveling of the information battlefield (i.e., the transience of informational asymmetry). The data and my beliefs are consistent with the weak and semi-strong forms of the EMH.