From reading the current thread and this thread from July, it seems like The Tale of Two Cities. Then was the worst of times; now is the best of times. An interesting dichotomy for sure.

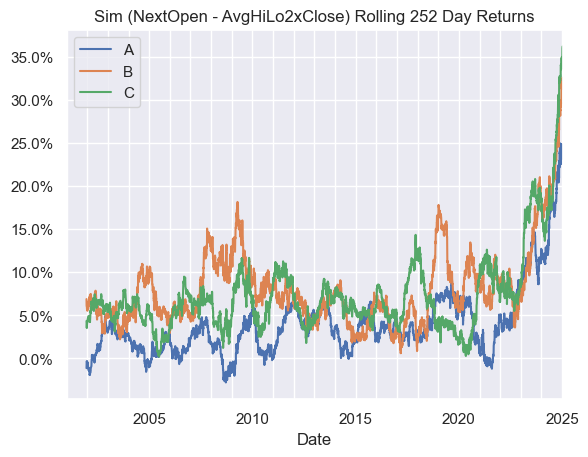

Personally, I have noticed one emerging area of concern with some of my strategies over the past year for which I'd like to raise awareness. For each of three strategies, I run two sims, one that fills at "Next Open" and one at "Average of Next High, Low, and 2X Close" and compare the difference of the 1-year rolling returns. Over the past 18-24 months, the delta in performance has skyrocketed to never before seen levels, meaning the Avg Hi/Low/2xClose sims are badly underforming their Next Open counterparts. The Next Open minus Next Close rolling returns are even bleaker, lagging by up to 45 percentage points last year.

My current hypothesis is that some of the shorter term factors in the ranking systems are now realizing faster than before, within one day. I first considered market impact as one hypothesis but 1) I'm not trading one of these sims and 2) I don't see any reversion, at least over a 5-day horizon. I need to do a further study to see if there is some impact occuring over a longer horizon though.

In response, I've already rolled out new version of these systems that tilt away from shorter term factors, but I have several other takeaways even while I still continue to investigate.

- Next Open sims are far too optimistic except for strategies focused on LOO/MOO orders. Though the longer term your strategy is, the less effect you should see from changing this reference fill price anyway.

- Even Average Next High/Low/2xClose sims are not necessarily realistic proxies for expected filll prices as they just represent the extrema in price and time space. I believe P123 should be integrating VWAP price series (which FactSet provides) as an option to allow simulations at potentially even more realistic fill prices. I've requested this feature before, but I feel the need is even stronger now. Besides, VWAP prices could be useful in factor creation which is an added bonus.

- To the same end of more accurate sims, it would be helpful to support formulas for the fill price. This would be especially helpful for strategies with less liquid names and bonus points if the formula could also reference the order size and expected daily volume. For example, to simulate a multi-day execution trajectory:

Price for Transactions = VWAP(-1)/2 + VWAP(-2)/3 + VWAP(-3)/6

- The rank performance tool can be blind to some of the term structure of your factors. A factor showing strong excess returns for weekly rebalancing will do you no good if the bulk of those excess returns are happening within the first day before you can execute into that position. You may want to consider improvements down the road to measure how those excess returns realize over the course of the rebalance period.

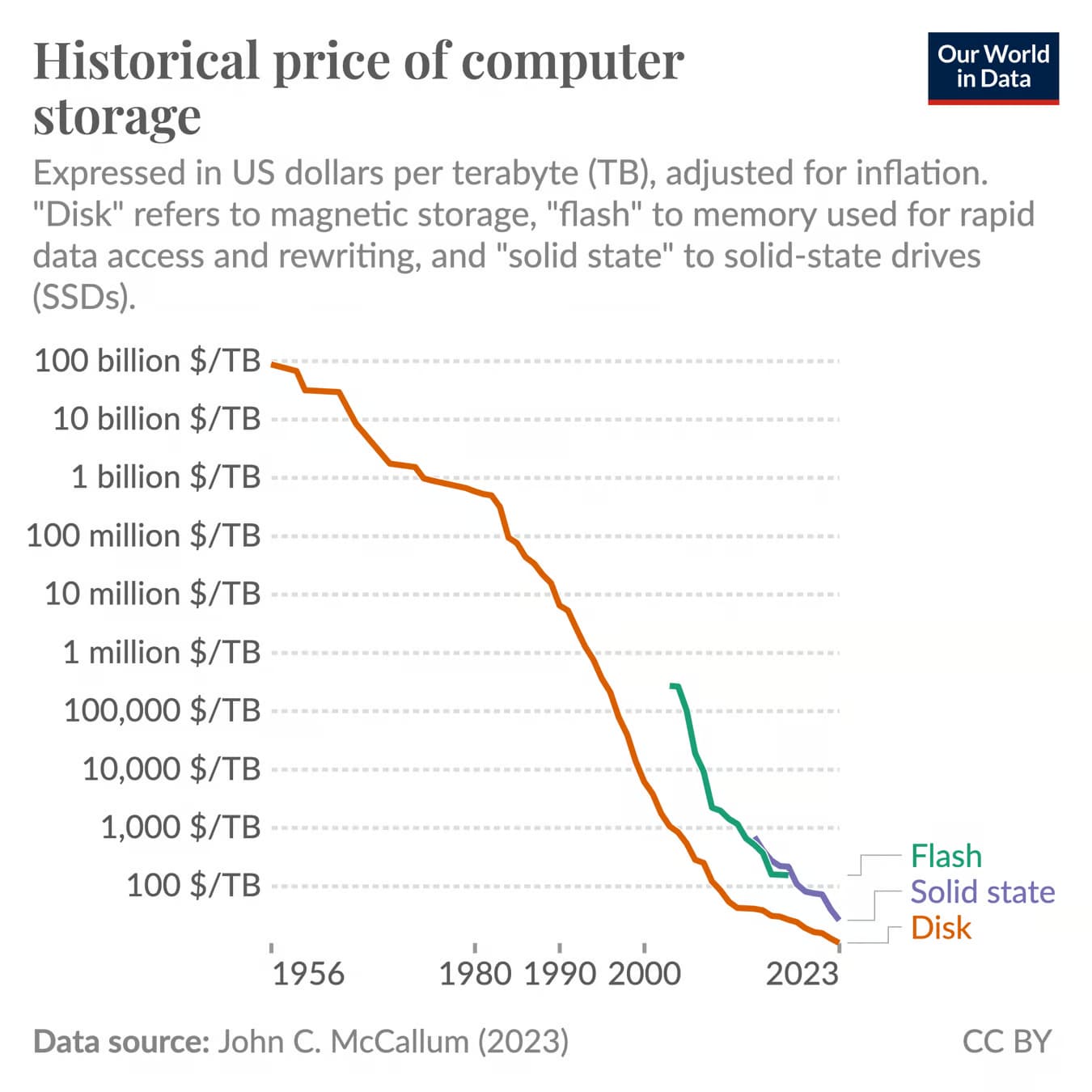

- Over time, the markets are getting faster and more efficient while we (p123) are staying the same with weekly ranking and rebalancing. Since 2000, the cost of storage has dropped by a factor of 500x:

Supporting daily ranking should only incur a ~5x increase in storage and compute, and would help us all better capture some of this lost alpha. Furthermore, even "slower" factors will likely only realize faster over time, so even if you're not impacted yet, you may eventually be. I think we likely need to evolve lest we eventually go the way of the dinosaur.

I don't want to shout fire in a crowded theater prematurely here, but I do sense some smoke in the air and at least want to proceed cautiously and better understand what's occuring.