I just got burned with 0.6% slippage when selling 6 shares of UPRO this past Friday. I had assumed that with such high liquidity in the underlying index the spread would be very thin. Does anyone have an idea on how to improve slippage for these ETFs?

How I figure 0.6%:

My six shares got filled at 9:30:22 at 138.84, which was the first trade of the day. According to Yahoo Finance the opening NAV of UPRO (ticker ^UPRO-IV) was 139.67. The difference is about 0.6%.

Chipper - you can’t achieve the theoretical price of an index on the opening, much less leveraged index. Many of the underlying stocks haven’t even traded yet, so it is really just an estimate (guess). You can only measure slippage against a real trade - so the question is… did you get the opening price listed for UPRO? If so, then there is no slippage.

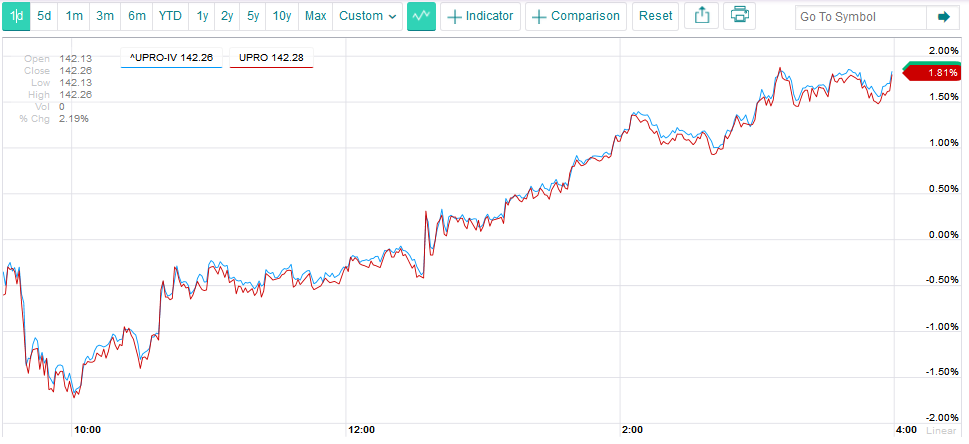

No trades were recorded at the exchange until 9:32:14 (at $139.18 according to NASDAQ.COM), which means that IB filled my order internally. Maybe “slippage” is not the correct term but they say that a picture is worth a thousand words. This chart which compares UPRO to it’s NAV throughout this past Friday may help crystallize my dilemma. Notice how UPRO almost never traded above it’s NAV throughout the day. Yet my trade got filled at 0.6% above NAV. Someone took advantage of me on that one. I would like to make sure that it doesn’t happen again. I use IB and I would like to get filled as close to the open as possible (when the signal is fresher) without moving the market.

Does anyone have experience trading ETFs that they can share?

Chipper - You traded an ‘Odd Lot’ which is handled/routed differently. An ‘Odd Lot’ does not appear in the publicly displayed quote stream, thus cannot establish the National Best Bid and Offer (NBBO) that ‘Round Lots’ get.

Thanks Hedgehog for the information. Since UPRO has a round lot size of about $14k (which is actually $43k since it is 3x leveraged) and since these trades are trimming my hedge, round lots are not an option. (BTW, I did have problems when trading round lots of ETFs at the open; apparently the underlying cannot be hedged right away at reasonable spreads but see this link for more info on ETF liquidity) I also had similar problems trading round lots of ETFs close to the open.

So let me rephrase my question: Does anyone have experience trading round lots of ETFs that they can share?

I often trade TQQQ at the open or close. Over a number of trades my round trip slippage was 0.017%. I trade at IB and generally use MOC orders at the close and market orders overnight for the open. I recently traded CURE a few times, which has much less volume. First trade had higher slippage at the close so I tried using a market order 1-2 min prior to the close and that seemed to work better. Somewhat surprising to me but using a Market order at the OPG I have not yet had any slippage from the opening price.

I recently reviewed IB order types to see if there was one that might help get better open and close prices. Of interest is Relative/Pegged to Primary. You specify an offset and on a buy order it will put in a bid for you at the NBB + offset with a limit as well. So if the market moves up your order follows it. If it moves down they say in an orderly market you should be filled. Haven’t tried it because I am getting fair enough results with the other orders but it gives you control of your slippage vs. the current price.

[quote]

I recently traded CURE a few times, which has much less volume. First trade had higher slippage at the close

[/quote]This is puzzling. Are you defining slippage as compared to the closing price? All MOC orders are guaranteed to get the same closing price.

I spent quite a bit of time studying the various IB algos and trying to use them a little. Slippage on their relative orders are usually greater than their limit orders.

BTW, I measure ETF slippage relative to NAV (the value of the underlying index) and not relative to trading prices. That’s because the ETF specialists can create ETF units by buying the underlying stocks. It only costs them the bid/ask spread on the underlying holdings. In theory ETF slippage should a bit more than that spread to give the market makers some risk free profit.

IBs website is known to have misleading and/or incomplete information–especially when it comes to the nitty gritty details. All orders must be routed somewhere. Market on close orders are generally routed to the primary exchange (such as NYSE NASDAQ or AMEX) of that security. All orders sent to an exchange get executed at the same price over there.

You can study this on the Nasdaq.com site. The Nasdaq.com website has an accurate list of trades. If you look at a high volume stock such as AAPL (after the close when the info will be posted) you should be able to see that all trades including round lots and mixed lots executed at the close at the same price.

Are you measuring closing prices using data imported into Excel? I would guess that the discrepancy that you noted between the reported closing price at the actual execution of your market on close order was due to inaccurate closing price data. Imported data taken off Yahoo Fiance does not always have accurate opening and closing prices. To verify it you can check P123s closing price for that security on that day. I have found P123s prices to be accurate.

This is not about slippage, which with your UPRO trade was likely zero or close to it.

Assuming Yahoo’s number is reasonable (Yahoo is an ad-supported consumer web site; don;'t over-assume anything about data quality there; they license from good sources, but since I started using Yahoo in the -90s, I and other old-timers can’t help but notice the deterioration in their attention to “product”), it would be about “tracking error,” the difference between NAV and market price. With closed-end funds, where there is no mechanism other than supply and demand, to keep prices within hailing distance of NAV, the tracking error can become noteworthy. That’s why a significant part of an investment case for/against a CEF can have a lot to do with tracking error, more affectionately referred to as premium or discount.

This is also likely why ETFs were invented. Essentially, an ETF is nothing ore than a modern CEF, a CEF that comes with an institutional arbitrage feature designed to make supply/demand efficient enough to keep tracking error much closer to zero. (This refers to the right institutions have to create new ETF shares by assembling a basket of securities that matches the ETF portfolio and tendering them to the fund in exchange for newly issued shares, and the corresponding institutional right to destroy ETF shares by tendering them to the fund in return for receipt of equivalent portfolio securities.)

And speaking of tracking error, I wouldn’t complain so much about the difference between

ETFs like UPRO are part of a newer breed even in the context of the ETF world. They don’t hold stocks. Instead, they hold derivatives structured to relate to a collection of stocks (e.g. an index) in a contracted way. Normally, these indexes are well-known entities (although that’s getting increasingly less so as more of these come out). So in the normal workaday world, these derivative-based ETFs tend to also have minimal tracking error. But still, there is an extra layer of transaction/potential transaction between the “underlying” securities and the ETF market price. So you can occasionally get instances of bigger-than-usual tracking error.

And speaking of tracking error, I wouldn’t complain about the difference between an execution price of 138.84 and a Yahoo indicated open of 139.67 (wherever/however they got that number). If you’re trading in souped-up derivative-based ETFs, accept it and move on. (When crises occur, instances of tracking error can get a lot larger.) If your model depends on nit-picky things like that, then it’s inherently flawed (it may be expecting things of derivative-based ETFs that are inconsistent with what these securities actually are) and needs to be revised or discontinued.

I use IB Relative/Pegged orders every day at the open (including odd lots), and am very happy with the fills, especially on something like UPRO where the bid/ask spread can be a few cents sometimes (as opposed to SPY where it is usually one cent).

This is tracking error, not slippage as commonly discussed on P123.

Unless you are replicating this ETF by modelling the derivatives, trading and funding costs, as an individual I don’t know how you might be able to trade to minimize tracking error. The best I could suggest is to download a lot of data and find the time and/or market conditions when observed tracking error has been minimal and go with that.

The creation unit size for this ETF is 50,000, or $7.1mm with a $1250 creation fee. The managers of this ETF are not altering share count for small trades and small NAV premium/discounts. The trading pressures will move the discount/premium around during the day. There are lots of costs in trying to arbitrage premium/discounts, namely margin/funding costs and bid/offer, documentation, operations, with likely a significant threshold for it to be worth it to them to alter derivatives exposure.

To your issue, from Feb 12 to 2012-02-23 12:01, the UPRO price less the UPRO index had the following stats, as a percentage of the UPRO price, on a tick basis:

Min: -120 bps

Mean: -95 bps

Max: 133 bps

StDev: 15 bps

Your difference from NAV was way into the 99% tail of observations, possibly due to odd-lot and trading at the open. Most of the time you would expect to be within 20bps of the NAV based on the dataset I used. (That being said, a few traders happened to get discounts of over 60bps on the other side of the distribution.)

To Marc’s point, 3X levered ETFs will likely have the largest variation in tracking error on an intraday basis.

[quote]

Your difference from NAV was way into the 99% tail of observations, possibly due to odd-lot and trading at the open.

[/quote]That’s what I figured. I don’t like being burnt and will look to modify my trading strategy.

Marc, I short UPRO as a hedge when economic fundamentals are deteriorating. One of my ports is signaling to hedge probably because of the hit to GDP caused by reduction in drilling as predicted by Ray Dalio of Bridgewater. The hedge is adjusted every couple of days as the relative sizes of the hedge and my portfolio diverge. The strategy works fine without frequent re-balancing of the hedge but re-balancing it does add a small but noticeable amount to the returns because it takes advantage of mean reversion in the index.

[quote]

I use IB Relative/Pegged orders every day at the open (including odd lots), and am very happy with the fills, especially on something like UPRO where the bid/ask spread can be a few cents sometimes (as opposed to SPY where it is usually one cent).

[/quote]Tom C., what do you like about your fills? Are you measuring slippage vs. the quoted open or the bid/ask spread?

I am looking to improve against the bid/ask spread. There’s no practical way to avoid tracking error in these products, these tend to cancel each other out over time. But I can certainly avoid in many cases not hitting the ask on a buy, or hitting the bid on a sell. Not to mention the rebates you can get on IB commissions by providing liquidity instead of taking it away

If that’s what you’re doing, you should be able to cope with tracking error – even for a triple leveraged vehicle. The make or break will be in your timing model.

But one thing did catch my attention: You do need a lot of re-balancing. Leveraged (double or triple) ETFs were designed for day-at-a-time holding periods and when they came out, there was a lot of screaming and hand wringing about the horrifying things that happened to people who pursued even moderate buy-and-hold strategies with these things. I got into the controversy back in the day and came to the conclusion that although they were designed for 1-day holding periods, you could get by with more, but you did still need to keep the periods under control, if not with quick exists then at least by rebalancing often enough to be constantly be averaging up/down and adjusting your cost basis. Can’t go into much detail now – memory not what it used to be – but if you search for me on seeking Alpha, you’ll find some work I did in the area back in the mid- to late-2000s. Just make sure you understand the decay issues often built in to these (especially on the short side) and you’re rebalancing often enough to properly address them.

[quote]

Just make sure you understand the decay issues often built in to these (especially on the short side) and you’re rebalancing often enough to properly address them.

[/quote]I’m actually shorting a 3x long ETF, so I am short the decay. The rebalancing issue worried me because 0.6% slippage negates at least some of the benefits of frequent rebalancing. In other words, I was concerned that trading odd lots near the open would always cause tracking error. But see my next post.

Thanks to Shaun for giving me quality bid ask data from Bloomberg (in a PM), I now know that you guys were right; there was almost no slippage but there was tracking error.

The bid ask for UPRO at 9:30:21 EST was about 138.82 / 138.88. Since my fill was at 138.84 there was little if any slippage even though it was a “Relative” order. As Marc Gerstein pointed out in his series of SA articles tracking error is greater at the open. Backtests include tracking error starting from the actual inception of the ETF.

I have looked into shorting long leveraged ETF’s in the past for the exact same reasons but did not find it attractive:

Short availability tends to be very low and borrowing rates sky-high when in a bear market, especially for leveraged ETF’s. (rationale: short demand far exceeds long supply when sh*t hits the fan)

Borrowing rates for leveraged ETF’s tend to be higher then for non-leveraged ETF’s. (rationale: free lunch for decay is arbitraged away)

Due to the reasons above I have not yet found any opportunity to generate alpha from these products. The only reasonable market hedge I have found is bonds, particularly long-term bonds with high, e.g. AAA, ratings nominated in a major currency (e.g. dollar, euro, yen).

Anyway, if you or other members have found a real good use for these products I am all ears…

Thanks for the warning. I am shorting it now while the market is complacent. If the market goes haywire I can switch to a 1x ETF if necessary. IBs short availability tool is listing 200,000 shares available at ~4.3% borrow cost for the 3x levered which is equivalent to ~1.4% unlevered. The expense ratio is 0.95% which means a net fee of about 0.5%. A forced buy in should not cause a price spike because of the vast underlying liquidity. I am monitoring it daily.

For comparison SPY has a 10,000,000 shares available to borrow at a cost of ~0.14% with an annual expense of 0.09% = 0.05% net but it does not decay.

Re ‘shorting the decay’. Whilst there is a (well trailed) decay in sideways and falling markets, I might be being stupid or obvious but I believe there are less well known compounding benefits in upward trending markets.