Hi Jerome, I don’t want to speak for Andreas, but just throw out what I can share on this. I’m pretty sure that image is from Hedgeye and is part of their rate of change process. (I followed them for a while after Andreas’s suggestion and learned from it.) Eric Basmajian on seeking alpha I think has a process that uses similar rate-of-change analysis for for looking at macro and I think his articles are very good.

I did a bit of math on it over last 20 years as well as since 1968, and if I did my numbers right (not a given as I’m not sure I’m using “right” rate of change in all cases), while returns coming out of quads 3/4 have been bad over the past 20 yrs, returns subsequent to quad 4 (slowing gdp growth and falling inflation) weren’t as bad over long term - perhaps due to sometimes getting big rallies coming out of cyclical bottoms, and perhaps due to more rapid historic cyclicality than we see presently. (I’m not sure about this. The latter is just speculation, just musing out loud.) Subsequent returns to the quad 4s in the 80s and 90s seem to do pretty well - such that quad 4 seemed like a signal to get positioned into equities over that time frame. Figuring out and positioning for the coming “quad” is a big part of what hedgeye seems to do though.

While I do appreciate your answer, I am not completely sure what to make of it.

It looks to me that these 4 quads are broadly similar to the kind of economic cycles one can find in the literature - but nicely summarizing together the “better / worst” asset class, the “better / worst” sector etc for each Quad.

As you imply (I think), the key is to know in which Quad you are at time T and therefore it is a question of the indicators used and how reliable they are.

If I got this right, Quad4 is the typical recession / depression and indeed if you have a high degree of confidence you are near the bottom, it makes sense to start going heavy in equities. But I do not get the feeling from your backtest results that you do have such a high degree of confidence in the indicator. Or did I misunderstand?

ist not on the Picture, your are Right, I pickt it up from there Videos.

Explanation: When Inflation goes down and GDP goes up at the same time Cyclical Rally, e.g. a lot of value stuff…

My take: I would Have been dead in the water the last years, if I would not Have combined value with Momentum, value has ist

Merits, but it is not for me to wait years until it is in favour again…

I have recently been researching the hedgeye quads. I was able to create the historical quads using data from FRED for inflation and GDP and Excel for backtesting. It’s basically looking at the change in the growth rate for inflation and GDP. I compared three years with hedgeye and only one quarter was different, but I think that is because the data changed.

What hedgeye does is predict the current and next 2 quads. And they have a playbook based on the quads for sectors and style. But they also apparently have a large analysts team that provides additional validation before making investment calls. I don’t have a lot of experience, but I like their approach and subscribed. I also recently subscribed to EPB Macro. Its playbook is based on changes in the growth rate, so one dimension instead of two.

My assumption is that since hedgeye predicts the future quad, that it’s possible to backtest using the historical quads. On a go-forward basis, the newly predicted hedgeye quad would then be updated manually in the formula for the current quarter.

Yuval described in a post a strategy for ranking sectors based on historical performance such that those sectors that outperform for a given ranking system are ranked higher, as one of many factors. My thought was that perhaps this could be enhanced by overlaying the quads such that the sector ranking may change depending on the quad. Yuval also described a substitute for sectors called clusters in a post that might be used instead.

Using the quads, I assume other factors could also be weighted differently such as value. Currently, I don’t have any performance results.

Jerome and Andreas, I did this a long while back, but I’ve attached a spreadsheet that shows the calcs and what I was doing. I updated recent quarters so data should be fairly fresh. Columns bg and bh are 2 variations of quad calcs I used, and down at the bottom of the columns are the column sum and average forward return calcs for the quads. Hope it may be useful to you. Beyond just being familiar with the economic cycle, I don’t really utilize any of this for timing. It did lead me to a likely different view of quad 4 already mentioned.

Again, I’m not sure of the proper way to calc because I wasn’t always matching quad determination (and sometimes quads change with data change), but I think the calc variations used are getting the spirit. I make no effort to predict future quad - just looking at things like "if current or most recent quad is X, what is forward 3m, 6m, and 9m returns in columns out to the right.

There’s other stuff in the spreadsheet that I don’t recall much of what I was doing, looks like making rank percentiles of growth and or inflation, but I’m not sure of my thinking here other than growth used to be a lot stronger than it is currently, so maybe slowing down from 5% growth isn’t as big of a deal of slowing down from 2% growth. But again - I’m not sure what I was doing.

The worksheet initially had a lot of links to other spreadsheet tabs. I’ve tried to remove all of those links so everything will calc, but if I missed something let me know and I’ll try to fix it.

I have made public a custom formula called $quad_2000_2019 which will return the quad for a given date between 1/1/2000 and Q3 2019. The values for the quads were calculated in Excel; all the formula does is check the date range and return the precalculated quad number. The formula actually calls another set of formulas, because of P123 formula length limitations.

SpacemanJones and I have the same calculation for GDP but different calculations for Inflation, so sometimes I have a quad 1 where he has a 2 or vice versa, and sometimes he has a 3 where I have a 4, or vice versa. I used GDPC1 from FRED for GDP as did SpacemanJones. I used CPIAUCSL from FRED for Inflation using the “Aggregation Method: Sum” on FRED to convert from monthly to quarterly whereas I believe SpacemanJones may have used PCE directly from BEA for Inflation.

Hi Greg, thanks for the posts. If you don’t mind me asking, have you used the quad information in p123 models?

I ultimately moved on to a different type of macro tracking, but have not utilized macro in my p123 models. I presently have the p123 models pick stocks, and if I need to adjust allocations for defensiveness it happens as an external decision. I know this isn’t ideal, but it’s what feels right to me and something I can more easily understand.

Thank you all - it will take me some time to review comments, formulas and spreadsheets and try to see if it can help me - but I wanted to thank you now.

My first test will be to use Gregg’s formula in an ETF system 1999-2019 and use for each each Quads a handful of ETFs representing the “right” styles & sectors (per hedgeye). Then compare that to SPY and R2000

NB: I would avoid doing pure binary shifts between ETFs but rather overweight / underweight. I have learnt that market timing systems perform better when viewed as helpful but imperfect rather than perfect 0 or 1.

Attached are some excel results that might provide additional guidance on sector selection. I have not used the quads for p123 yet. I was thinking to run a test like Jerome has proposed. I think some more work though could be done on quad definition as the range of results for a given sector for a given quad seems to vary a lot.

Sorry for the late response. I don’t have any specific evidence, only what I’m seeing in some of the models that I follow regularly. Attached are two models that have languished for a couple of years but are now showing signs of life.

It could be that it is the time of year, but “feels” more like an awakening than a seasonal thing.

Why put yourself through this? Instead of chasing Value which is a nebulous and fashionable thing, start with macro trends and you will have a much more pleasant investing experience.

These highly tradable (liquidity, low turnover) models are near the top of the heap for 1Yr % gain with gain > 30%. I have other macro trend models but I’m not posting them as Designer Models because the DM business model is busted. It needs to change.

Thanks. I am definitely looking into ideas where the port weights are adjusted automatically. And to be clear, I am open to the idea that some of my models will come back. I too see some early evidence that this could happen. Also, I do not claim to understand the macroeconomics of what is happening. That has not stopped me from posting multiple conflicting theories, as you know;-)

If you find anyone that claims to understand macroeconomics, then I suggest running for the hills because he is trying to get his hands in your pockets.

Macrotrends, what I am promoting is something different. It is pretty easy to identify massive growth areas such as the cloud, cybersecurity, healthcare, etc. They are no brainers. It’s a great place to put optimization and ML to work.

Hi Greg, Really nice study! Thanks for sharing this. I just glanced at it so far, but seems to advocate strongly for defensive sectors in the “slowing growth” quads 3/4 if we have confidence in our present macro diagnosis.

Again, really nice study - thank you for sharing. I’m actually going to have to learn some of your calcs. I didn’t know you could do conditional median and averages the way you’ve done. I’m still using Excel 2003, but seems like the way you’ve setup the calc works when I convert and open the file. That’s very useful.

Glad the spreadsheet was helpful. I don’t use the array function that often in Excel, so be sure to check the numbers; always nice to have another set of eyes. Note that the range for the “Industrial” formulas is shorter because there are fewer rows of data. Other than adjusting the range, it should be easy to add in other data series such as DWAQ for momentum by exporting from PortfolioVisualizer.

It would be nice if P123 provided the monthly returns for the SIMS, beyond just the latest year, as that would make it easy to analyze a SIM by quad (or other metrics). I couldn’t find this data. If someone knows how that would be great, otherwise it seems like that would be an easier P123 feature to add if there aren’t licensing restrictions and if others are interested.

Greg, I’ve learned much from this, including the non-market performance tips like the excellent excel tips and learning about the portfolio visualizer website for monthly data. The array formulas are new to me and something I’ve not worked with much, but very useful in this context. I have to be careful use them because of how it seems like I have to remember to enter the formula boxes and manually recalculate them if I change any data that precedes them - but very useful.

The worksheet has also been excellent to work with the data.

I think one thing that may be important with quads is the importance of being able to get the determination right in advance of it occurring, or as early as possible. I’m not sure I can do that with high confidence, so I did a few calcs where I lagged the quad determination by 3, 2, and 1 month, and that distinction seems to make a big difference. (When a transition to Quad 3 or 4 hit I’m doubt I’ll realize it on day 1, or even day 45). Most of the economic data is lagged and there’s often directional uncertainty as the time periods develop even after the data is released. I guess I feel like unexpected negative or positive “surprises” in the data might be behind return variances. For example: October new home sales just released today 11-26, so my data is quite a bit behind on that datapoint and I would not be able to make October or November allocation decisions based on it.

But anyhow, with that thought in mind I added some calcs to your excellent workbook and share it (attached below). I added SPY as well as doing quad lags for 3, 2, and 1 month to represent not catching the cyclical turns in real-time, but with a lag. My excel is old, so it wouldn’t calculate a few of calculations that you had, but I wanted to share what I had as I think it might be relevant in practical usage, especially if we have concerns about correctly calling quads in advance.

Again, thanks so much for sharing the data, and your calcs, and all that. I think I entered the array calcs properly, but please check if relying on. This was fun to work though and you set up an excellent template with great data to work with.

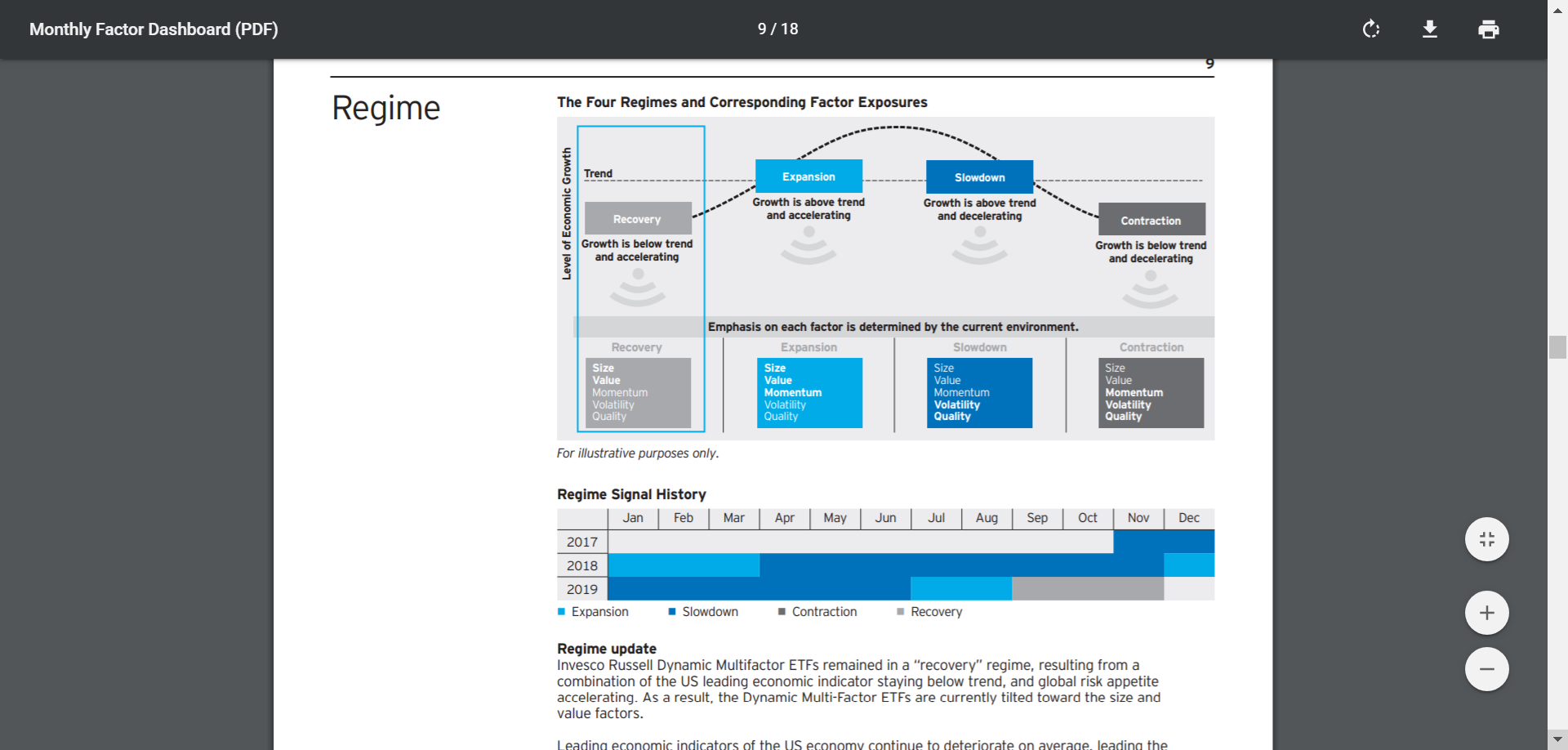

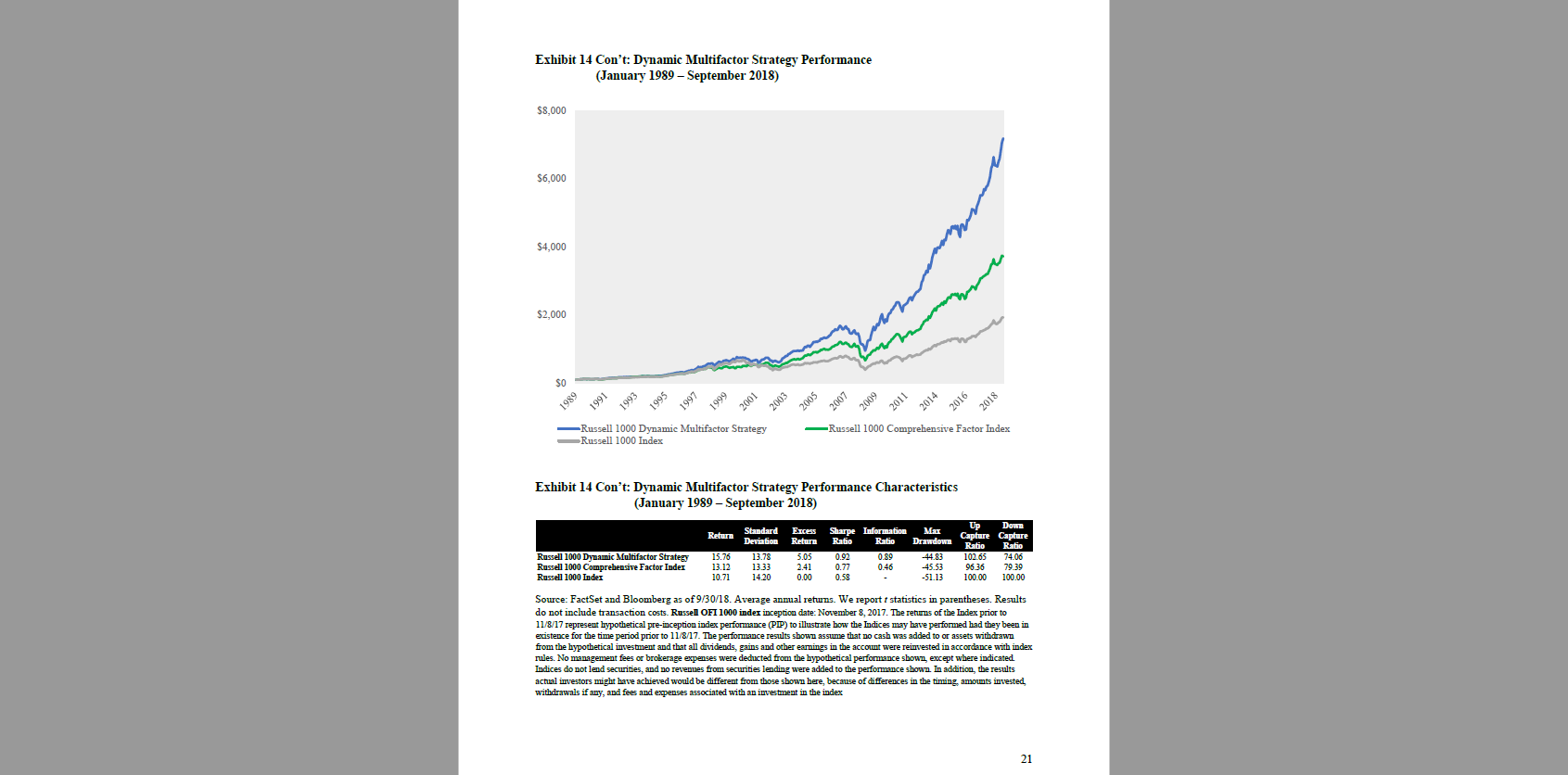

As an alternative to hedgeye, I suggest we can follow the rotation of factors in the OMFL (Russell 1000 Dynamic Multifactor ETF), its holdings rotate between Recovery (Size,Value), Expansion (Size, Value, Momentum), Slowdown (Low Volatility, Momentum) and Contraction (Momentum, Low Volatility, Quality) based on different economic conditions. The ETF holdings are available in the Invesco website. The ETF is currently in the Recovery Mode. I would personally add market timing to hold somthing like GLD/IEF in the Contraction stage instead of holding Momentum, Low Volatility, Quality stocks. This ETF has been extensively researched, I am attaching a research paper by London School of Economics/Oppenheimer Funds for reference.

ustonapc,

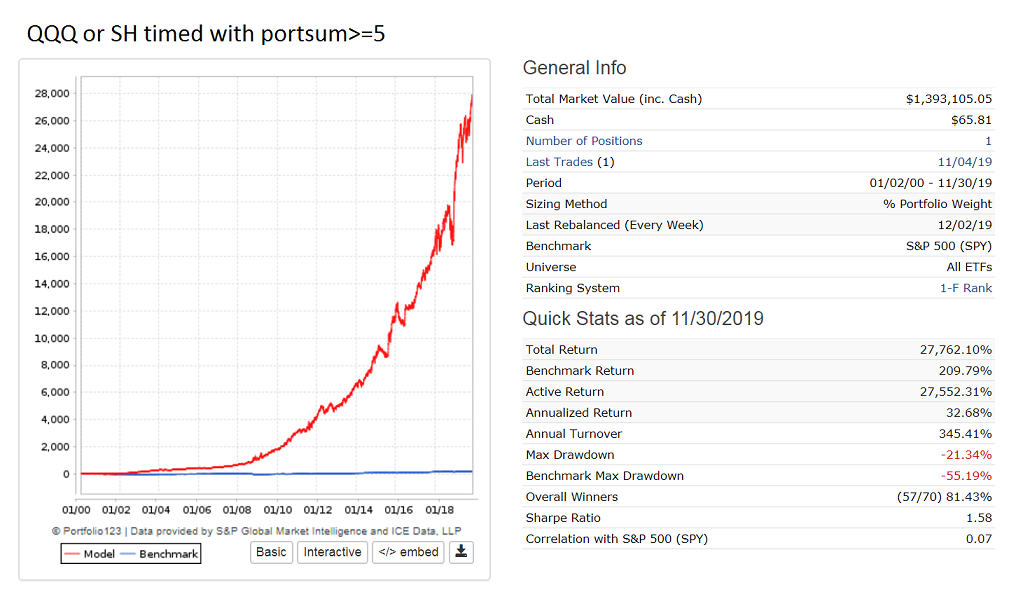

Use QQQ instead of OMFL which has only been around for 2 years.

A good market timer will return CAGR of 30%.

Here is one that switches between QQQ and SH.